Advertisement

- United States

- /

- Pharma

- /

- NYSE:NUVB

Top Growth Companies With Strong Insider Ownership November 2025

Simply Wall St

Reviewed by Simply Wall St

As the U.S. stock market experiences a robust week, buoyed by gains across major indices like the Dow Jones and Nasdaq despite recent technical disruptions, investors are keenly observing growth trends and insider activities. In such an environment, companies with high insider ownership often attract attention for their potential alignment of interests between management and shareholders, making them intriguing candidates for those looking to understand growth dynamics in today's market.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Super Micro Computer (SMCI) | 14.0% | 50.7% |

| StubHub Holdings (STUB) | 23.3% | 73.5% |

| SES AI (SES) | 12% | 68.9% |

| Niu Technologies (NIU) | 37.2% | 93.7% |

| FTC Solar (FTCI) | 22.6% | 78.8% |

| Credo Technology Group Holding (CRDO) | 10.9% | 30.4% |

| Bitdeer Technologies Group (BTDR) | 33.4% | 131.7% |

| Atour Lifestyle Holdings (ATAT) | 18% | 24.5% |

| Astera Labs (ALAB) | 11.9% | 29.1% |

| AppLovin (APP) | 27.5% | 26.5% |

Below we spotlight a couple of our favorites from our exclusive screener.

Super Micro Computer (SMCI)

Simply Wall St Growth Rating: ★★★★★★

Overview: Super Micro Computer, Inc. develops and sells server and storage solutions based on modular and open-standard architecture globally, with a market cap of approximately $19.60 billion.

Operations: The company generates approximately $21.05 billion from its high-performance server solutions segment.

Insider Ownership: 14.0%

Super Micro Computer is experiencing significant growth, with earnings expected to rise substantially over the next three years. The company is trading below its estimated fair value and has raised its revenue guidance for fiscal year 2026 to at least US$36 billion. Despite a recent decline in profit margins, Supermicro's revenue growth outpaces the U.S. market, supported by strategic expansions into federal markets and collaborations like its partnership with NVIDIA for advanced AI solutions.

- Delve into the full analysis future growth report here for a deeper understanding of Super Micro Computer.

- The analysis detailed in our Super Micro Computer valuation report hints at an deflated share price compared to its estimated value.

Daqo New Energy (DQ)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Daqo New Energy Corp. manufactures and sells polysilicon to photovoltaic product manufacturers in China, with a market cap of approximately $2.11 billion.

Operations: The company's revenue primarily comes from its polysilicon segment, which generated $639.06 million.

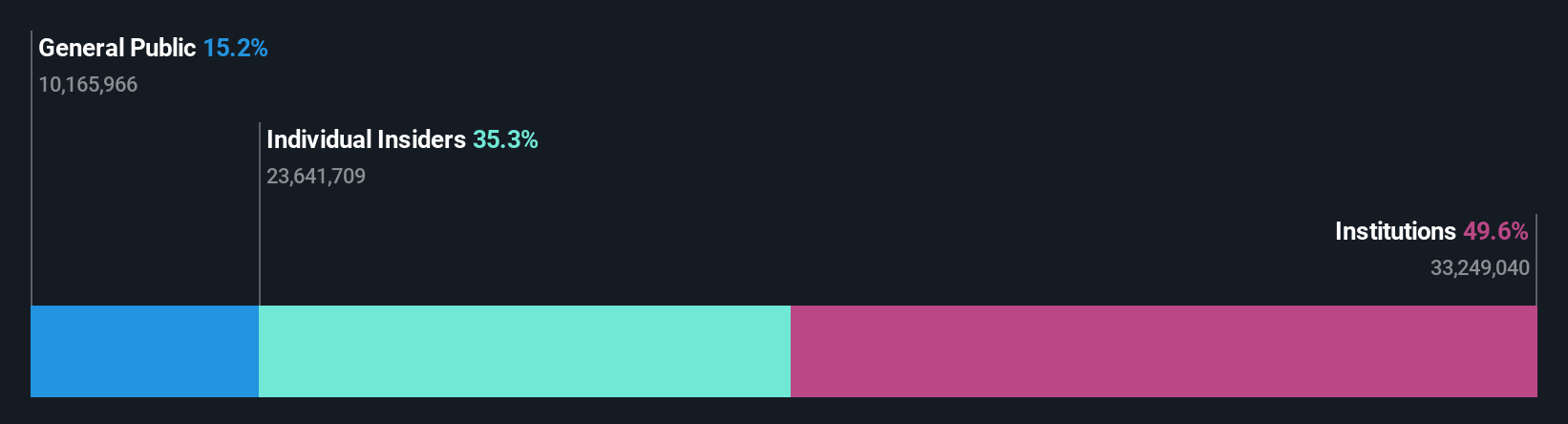

Insider Ownership: 35.3%

Daqo New Energy's revenue is forecast to grow significantly at 36.9% per year, outpacing the U.S. market average of 10.5%. Despite a volatile share price and low return on equity forecast of 1.8%, the company trades at a substantial discount to its estimated fair value, enhancing its appeal for growth-focused investors. Recent earnings results show improved financial performance with reduced net losses and increased polysilicon production, aligning with their optimistic production guidance for 2025.

- Click to explore a detailed breakdown of our findings in Daqo New Energy's earnings growth report.

- In light of our recent valuation report, it seems possible that Daqo New Energy is trading behind its estimated value.

Nuvation Bio (NUVB)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Nuvation Bio Inc. is a clinical-stage biopharmaceutical company dedicated to developing therapeutic candidates for oncology, with a market cap of approximately $2.75 billion.

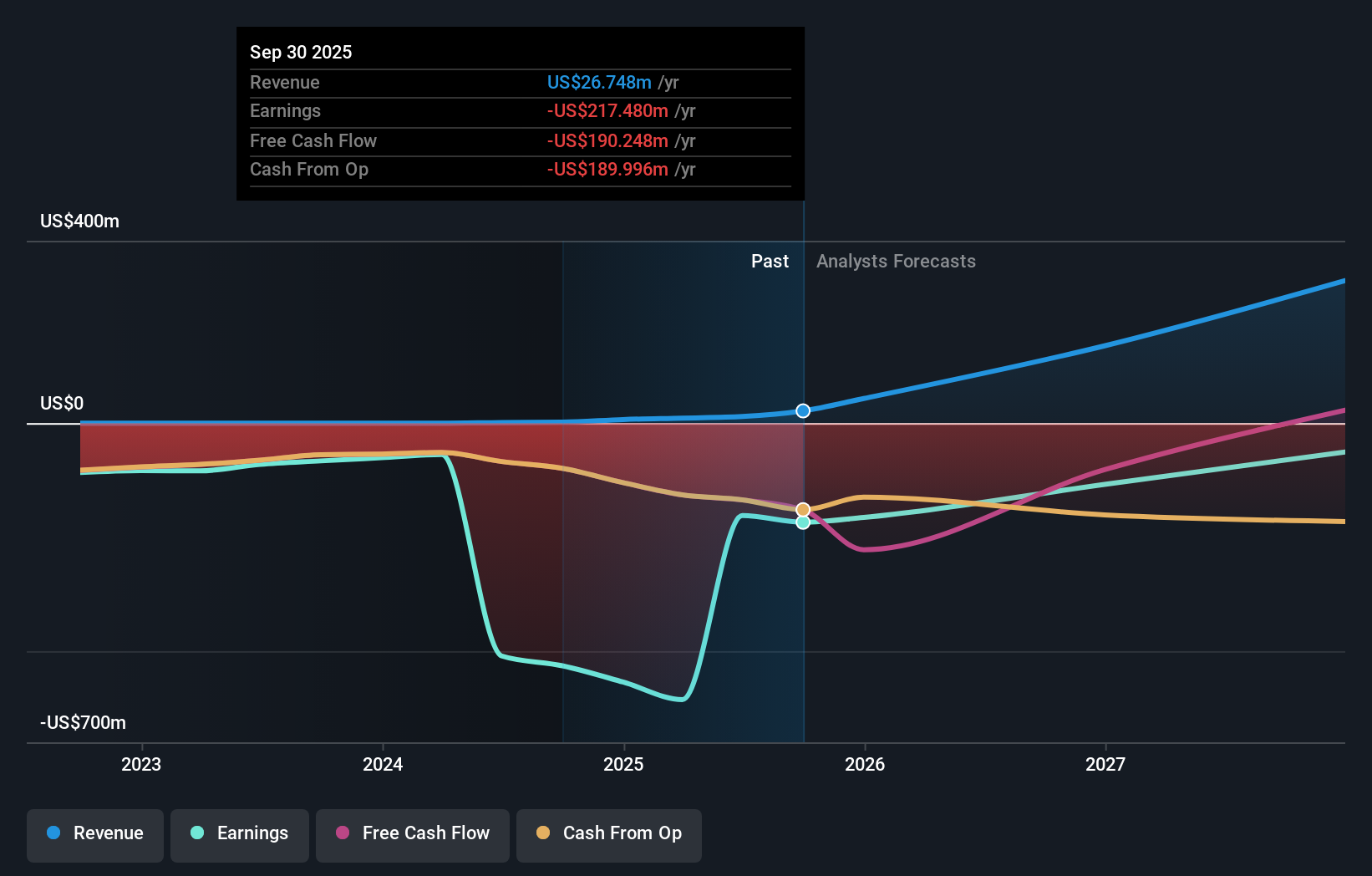

Operations: The company generates revenue from its oncology development activities, amounting to $26.75 million.

Insider Ownership: 24.9%

Nuvation Bio exhibits strong growth potential, with revenue expected to increase by 48.9% annually, surpassing the US market average of 10.5%. Recent positive Phase 2 study results for safusidenib highlight its innovative pipeline. Despite a net loss of US$55.79 million in Q3 2025, the company shows promise with substantial insider ownership and trading below estimated fair value. The stock's volatility may concern some investors, but analysts anticipate a price rise of 28%.

- Unlock comprehensive insights into our analysis of Nuvation Bio stock in this growth report.

- Upon reviewing our latest valuation report, Nuvation Bio's share price might be too pessimistic.

Taking Advantage

- Reveal the 197 hidden gems among our Fast Growing US Companies With High Insider Ownership screener with a single click here.

- Contemplating Other Strategies? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Nuvation Bio might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NUVB

Nuvation Bio

A clinical-stage biopharmaceutical company, focuses on developing therapeutic candidates for oncology.

High growth potential and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

98 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative