Advertisement

- United States

- /

- Life Sciences

- /

- NYSE:DHR

Danaher (DHR): Exploring Valuation After Q3 Earnings Beat and Bioprocessing Growth

Simply Wall St

Reviewed by Simply Wall St

Danaher (DHR) shares edged higher after the company reported third quarter earnings that beat expectations on both adjusted EPS and revenue, with ongoing growth in its bioprocessing segment catching investors' attention.

See our latest analysis for Danaher.

Danaher’s encouraging Q3 results have helped offset some earlier caution, but its 1-year total shareholder return of -3.8% still reflects a period of underperformance compared to sector peers. While its 90-day share price return of 11.3% hints at renewed momentum, investors remain attuned to the company’s steady bioprocessing growth and improving fundamentals.

If Danaher’s biotech momentum has you looking for the next discovery, you’ll want to see which other healthcare leaders are making waves. See the full list for free.

With Danaher’s solid earnings upside and shares still below their year-ago levels, investors are left to wonder whether the current price is an attractive entry point or if the market has already accounted for future growth.

Most Popular Narrative: 10.1% Undervalued

Danaher's fair value, as estimated by the most widely followed narrative, sits well above its last close. The narrative features ambitious projections that set the stage for a substantial premium if targets are met.

The sustained advancement of precision medicine and personalized therapies, including new AI-assisted diagnostic solutions and groundbreaking launches in genomics (like support for in vivo CRISPR therapies), positions Danaher's technology portfolio to capture higher-margin growth and drive long-term EBITDA expansion.

Want to know why this price target stands out? The real story lies behind bold profit margin expansion and a future earnings multiple that rivals fast-growth disruptors. Which unknowns and game-changing projections push this valuation so high? Click through to see which assumptions analysts are betting on for Danaher's next chapter.

Result: Fair Value of $254.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent global trade tensions and ongoing policy risk in China could disrupt Danaher’s growth story. These factors may put pressure on both revenue and margins in the future.

Find out about the key risks to this Danaher narrative.

Another View: Market Ratios Signal Caution

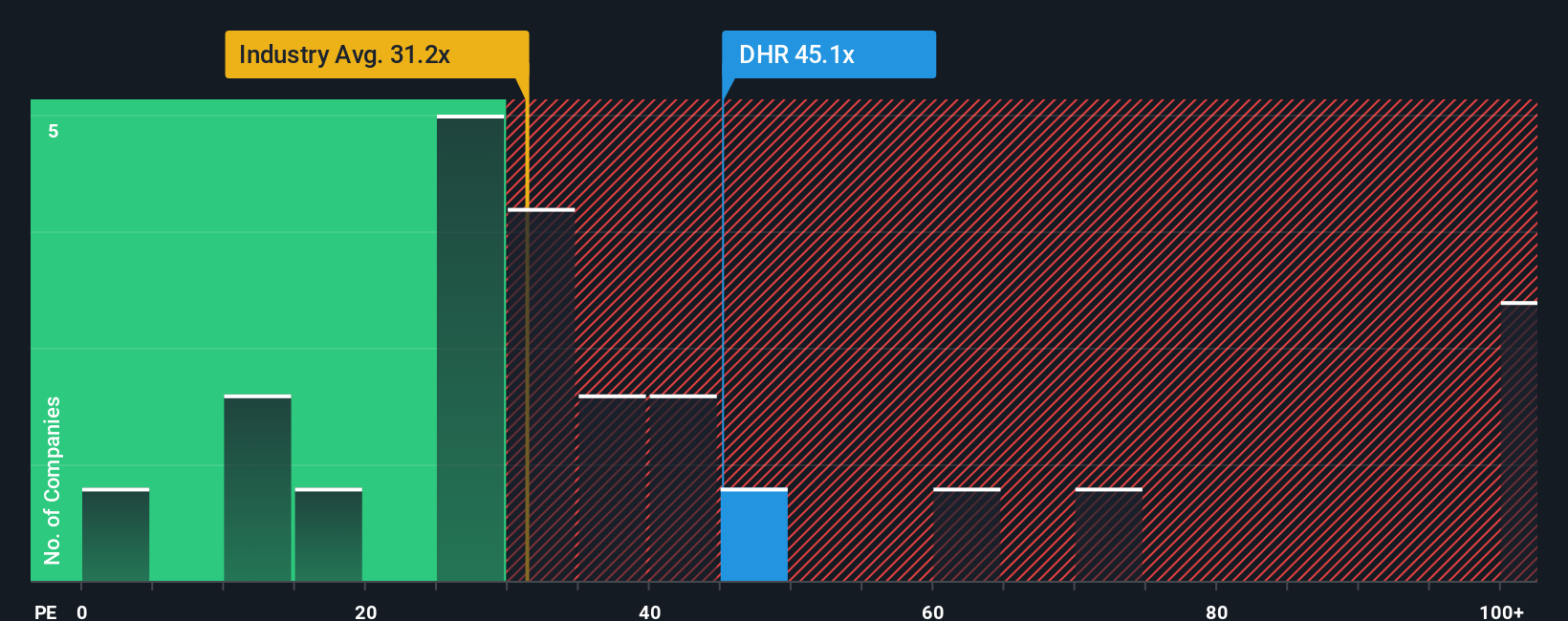

Take a look at Danaher’s current market ratios and you’ll see a different side of the story. Its price-to-earnings ratio stands at 46.1x, well above the industry average of 38.6x and the fair ratio of 31.5x. This suggests the stock is richly valued, which could limit further upside unless performance materially improves. Is the premium price truly justified, or could a shift in sentiment bring shares closer to the fair ratio?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Danaher Narrative

If you have a different take or want to dive into your own analysis, crafting a personal view from the data takes just a few minutes. Do it your way

A great starting point for your Danaher research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t settle for one opportunity when there’s a world of smarter investments waiting. Make your next move count with targeted stock picks from Simply Wall Street’s powerful Screener:

- Unlock tomorrow’s potential by targeting high-yield returns in these 15 dividend stocks with yields > 3%, which is built for those who prioritize consistent income streams.

- Get ahead of disruptive trends and position yourself for growth with these 25 AI penny stocks as it leads the artificial intelligence revolution.

- Capitalize on undervalued market gems. Seize your chance with these 927 undervalued stocks based on cash flows and stay one step ahead of hesitant investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DHR

Danaher

Designs, manufactures, and markets professional, medical, research, and industrial products and services in the United States, China, and internationally.

Excellent balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative