Advertisement

- United States

- /

- Pharma

- /

- NYSE:BMY

Is Bristol-Myers Squibb a Bargain After Recent 15.6% Jump in Share Price?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious whether Bristol-Myers Squibb is a hidden bargain or just another big pharma stock? Here is a breakdown of what the numbers and recent moves may indicate about its value.

- The stock has shown some life lately, jumping 6.5% over the past week and rising 15.6% in the past month, even though it is still down 13.3% year-to-date.

- Much of this renewed momentum comes as industry chatter and analyst upgrades have sparked new optimism. Recent developments in Bristol-Myers Squibb’s drug pipeline have begun shifting investor sentiment. Takeover speculation and regulatory updates have also played a role, making this a stock that is suddenly drawing fresh attention.

- On traditional valuation metrics, Bristol-Myers Squibb scores a solid 5 out of 6 for value. This suggests it screens as undervalued in nearly every area investors care about. Before exploring the standard valuation techniques, there is an even more nuanced way to decide if the price is truly right, which will be covered at the end of the article.

Find out why Bristol-Myers Squibb's -12.7% return over the last year is lagging behind its peers.

Approach 1: Bristol-Myers Squibb Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by extrapolating its future cash flows and discounting them back to today’s value. This approach helps investors gauge what the company should be worth based on its anticipated earnings, rather than just its current profits or market price.

For Bristol-Myers Squibb, the latest reported Free Cash Flow stands at $15.34 Billion. Analyst estimates project this figure decreasing to around $11.17 Billion by the end of 2029. These forecasts combine direct analyst projections for the next five years with longer-term trend extrapolations.

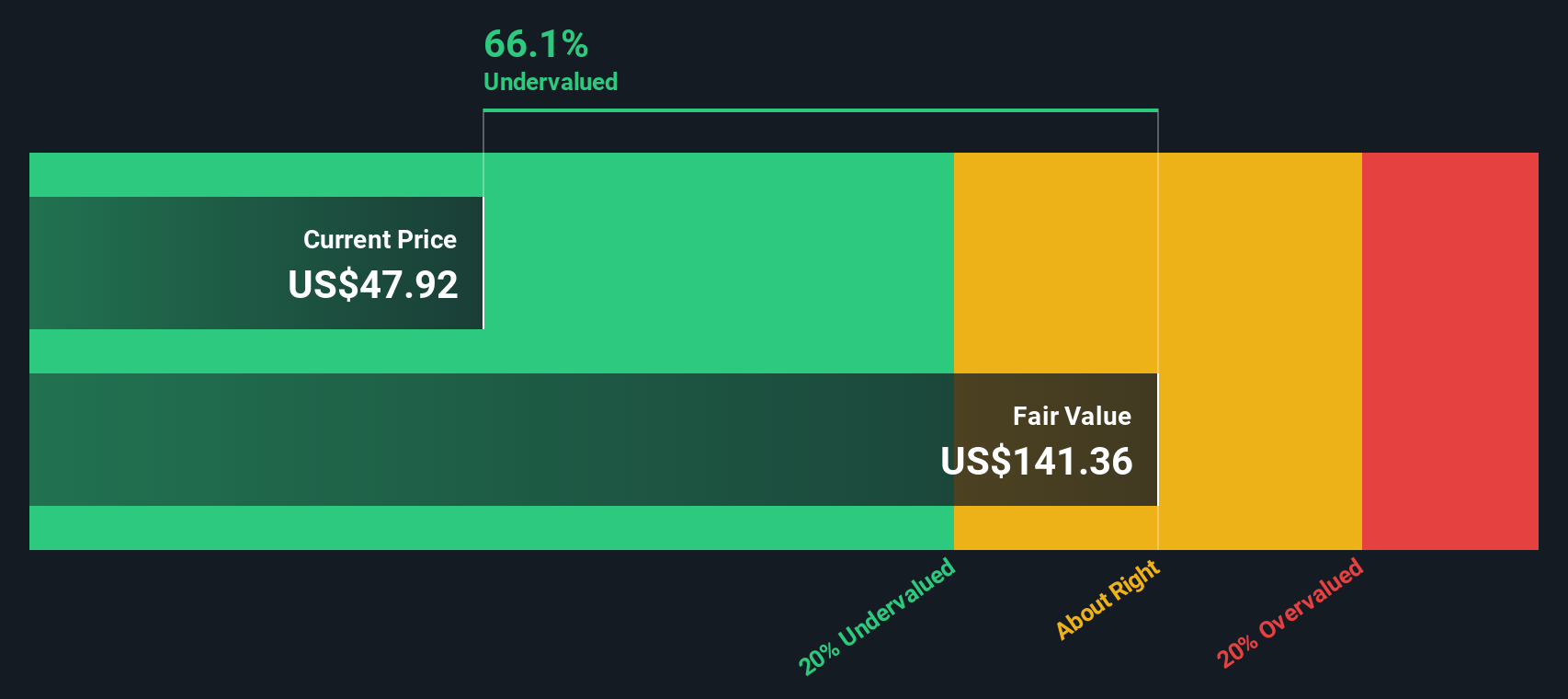

Using the 2 Stage Free Cash Flow to Equity model, the DCF analysis places Bristol-Myers Squibb’s fair value at $117.66 per share. Compared to the current market price, this implies the stock is trading at a 58.1% discount to its estimated intrinsic value, indicating it may be deeply undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Bristol-Myers Squibb is undervalued by 58.1%. Track this in your watchlist or portfolio, or discover 926 more undervalued stocks based on cash flows.

Approach 2: Bristol-Myers Squibb Price vs Earnings

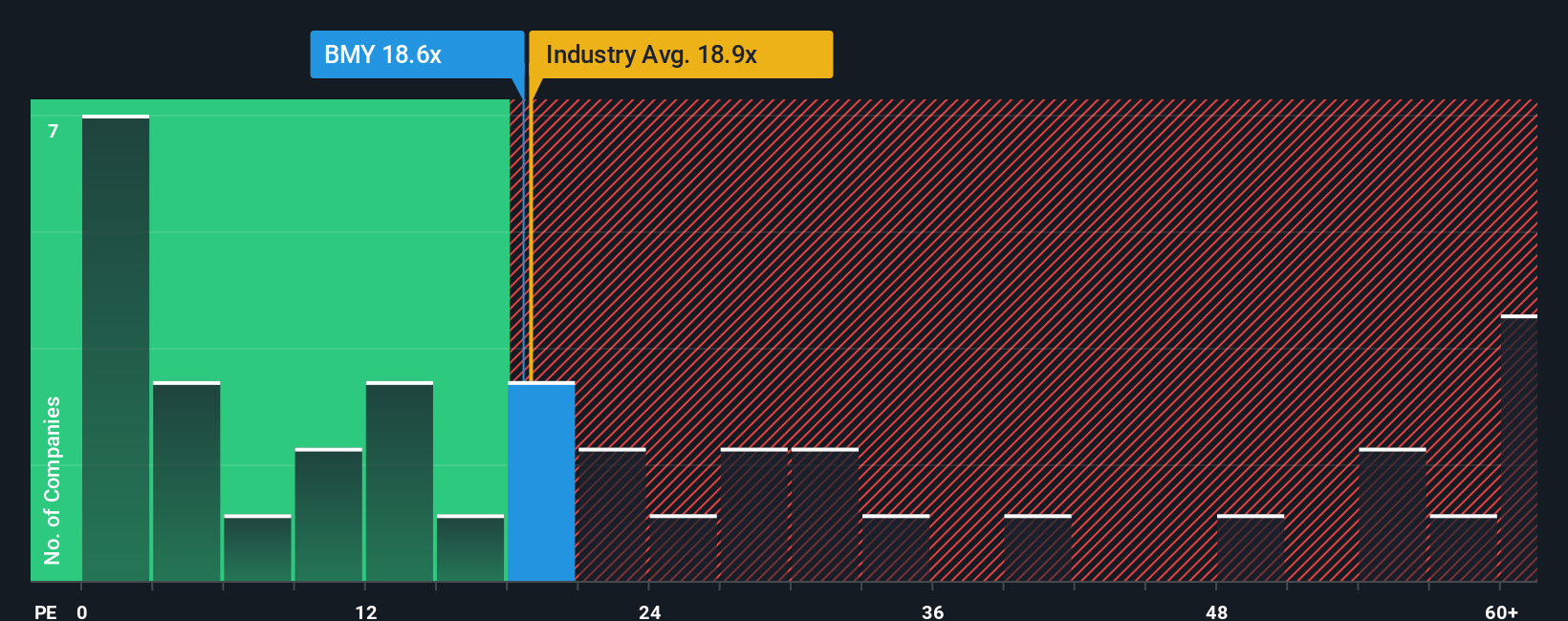

The Price-to-Earnings (PE) ratio is often regarded as a standard valuation metric for profitable companies like Bristol-Myers Squibb because it directly compares the company’s current share price to its earnings. This helps investors quickly determine how much is being paid for each dollar of profit, which is particularly meaningful when the company has a consistent record of generating income.

What is considered a “normal” or “fair” PE ratio can vary depending on growth expectations and the level of risk associated with the company. Companies experiencing rapid growth or viewed as less risky tend to carry higher PE ratios, while slower growth or higher risk usually results in lower ratios.

Bristol-Myers Squibb is currently trading at a PE ratio of 16.6x. For comparison, the average PE ratio among its pharmaceutical peers is 23x, while the broader industry average is approximately 20.6x. This indicates that the stock is priced more conservatively when compared to other major players in its sector.

Simply Wall St’s “Fair Ratio” for Bristol-Myers Squibb is calculated using a proprietary model that considers factors such as earnings growth, risk profile, profit margin, market capitalization, and the industry landscape. This model arrives at a Fair Ratio of 24.4x. This approach offers a more tailored assessment than simply comparing the company’s PE to peers or the industry, as it is based on Bristol-Myers Squibb’s specific fundamentals and outlook.

When comparing the current PE of 16.6x to the Fair Ratio of 24.4x, it suggests that Bristol-Myers Squibb is trading at a notable discount relative to what might be expected based on its own characteristics.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Bristol-Myers Squibb Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is the story and reasoning behind a user’s view on a company, connecting their assumptions about future revenue, profit margins, and fair value with a clear, explainable summary. Narratives make it simple for investors to see how a company’s underlying business outlook translates into a financial forecast and, ultimately, an estimated fair value.

With Narratives on Simply Wall St’s Community page, a tool used by millions of investors, anyone can articulate or explore different perspectives on Bristol-Myers Squibb. Narratives offer a straightforward way to decide when to buy or sell by laying out your assumptions, comparing the resulting Fair Value to the current share price, and updating automatically as new earnings, news, or regulatory developments emerge.

For example, one investor might construct a bullish Narrative for Bristol-Myers Squibb, projecting $67 per share using robust revenue growth and margin expansion. Another might set a far more cautious fair value around $34 based on lower growth expectations and competitive pressures. Narratives help everyone translate their vision into numbers and make smarter, more confident decisions, grounded in their own reasoning and open to revision as fresh data arrives.

Do you think there's more to the story for Bristol-Myers Squibb? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bristol-Myers Squibb might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BMY

Bristol-Myers Squibb

Bristol-Myers Squibb Company discovers, develops, licenses, manufactures, markets, distributes, and sells biopharmaceutical products worldwide.

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative