Advertisement

- United States

- /

- Pharma

- /

- NasdaqGS:PCRX

Pacira BioSciences (PCRX): Valuation in Focus Following Moves to Defend EXPAREL Patents Against Generic Competition

Simply Wall St

Reviewed by Simply Wall St

Pacira BioSciences (PCRX) recently filed lawsuits against The WhiteOak Group and Qilu Pharmaceutical, seeking to block their generic versions of EXPAREL. This move triggers a 30-month delay for FDA approval of competing generics and highlights the company’s firm defense of its intellectual property portfolio.

See our latest analysis for Pacira BioSciences.

Pacira BioSciences’ robust defense of its core asset comes alongside a strong year-to-date share price return of 28.6%. While recent legal actions have drawn attention, overall momentum this year has been positive, and the stock’s 1-year total shareholder return stands at an impressive 39.4%. However, long-term holders remain underwater from past declines.

If you’re eyeing healthcare innovators making strategic moves, it is a perfect moment to discover new opportunities in the sector with our See the full list for free.

With shares still trading nearly 28% below analyst price targets and at a steep discount to some intrinsic measures, investors are left to wonder whether Pacira BioSciences is an undervalued pick or if the market has already accounted for its future growth potential.

Most Popular Narrative: 18.7% Undervalued

With the narrative fair value set at $29, Pacira BioSciences’ last close of $23.57 sits well below this estimate. The gap highlights optimism from the consensus view, based on both strategic progress and high earnings growth forecasts.

The new strategic partnership with Johnson & Johnson MedTech for ZILRETTA is expected to double sales coverage and significantly expand reach across new physician specialties and healthcare systems. This development is considered a potential catalyst for revenue growth in 2026 and beyond.

How do analysts land on such a bullish number? The secret is in their aggressive profit turnaround assumptions and a surprisingly disciplined profit multiple. Read the full narrative to catch the exact blueprint for this fair value.

Result: Fair Value of $29 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Pacira’s heavy reliance on EXPAREL and the risk of delays in broader market adoption could challenge the bullish growth outlook reflected in today’s valuation.

Find out about the key risks to this Pacira BioSciences narrative.

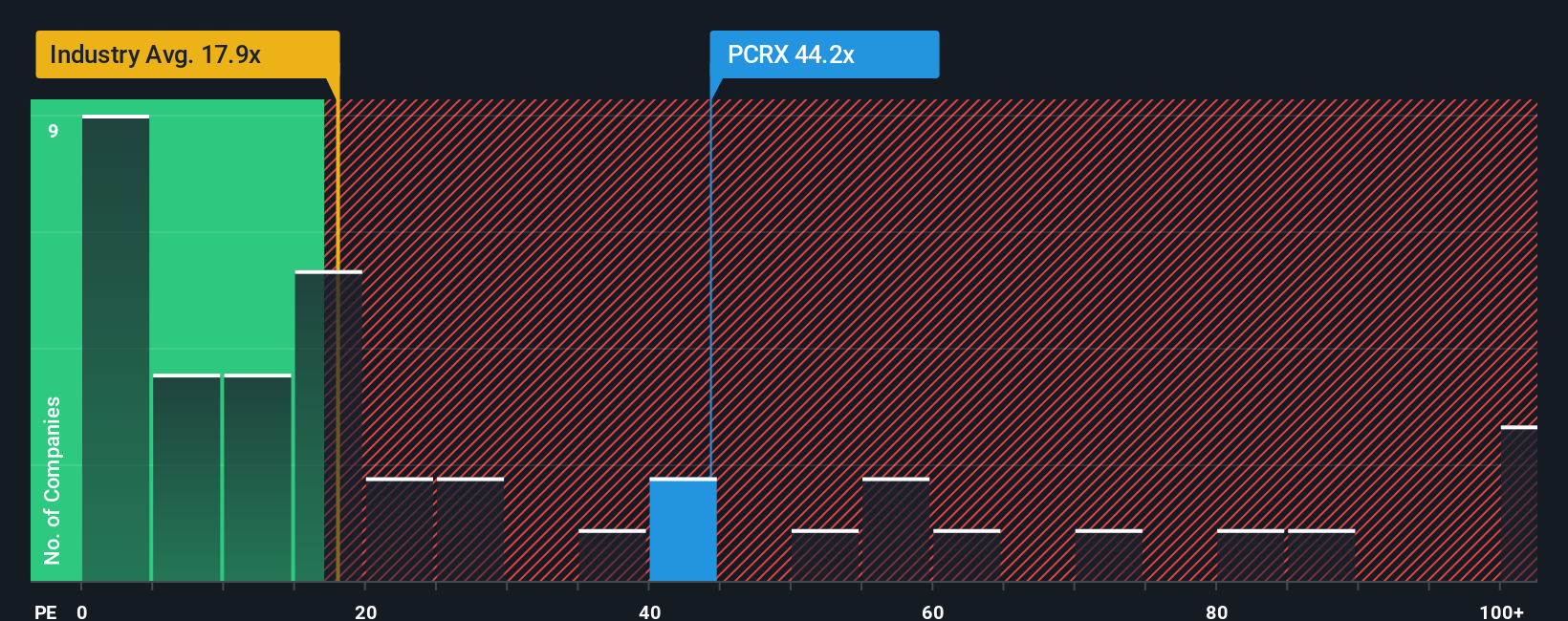

Another View: Are Multiples Hinting at Overvaluation?

While fair value and growth models suggest upside for Pacira, traditional price-to-earnings comparisons tell a different story. The company’s 47.3x ratio is more than double both the US Pharmaceuticals industry average (20.6x) and the peer average (15.8x). It also sits far above the fair ratio of 22.2x, a level the broader market could slowly move toward. This big gap points to real valuation risk if growth doesn’t accelerate. Are investors paying too much for possibility alone?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Pacira BioSciences Narrative

If you would rather shape your own story or crunch the numbers yourself, you can easily put together a personal analysis in just a few minutes with Do it your way.

A great starting point for your Pacira BioSciences research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Broaden your horizons and gain an edge in today’s markets. Don’t let compelling opportunities pass you by when powerful tools are right at your fingertips.

- Uncover hidden value by jumping straight into these 920 undervalued stocks based on cash flows with impressive fundamentals yet to be recognized by the wider market.

- Supercharge your portfolio’s growth potential when you spot tomorrow’s standouts with these 25 AI penny stocks leading the way in artificial intelligence innovation.

- Lock in attractive yields and strengthen your passive income by reviewing these 15 dividend stocks with yields > 3% boasting payout rates above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PCRX

Pacira BioSciences

Engages in the development, manufacture, marketing, distribution, and sale of non-opioid pain management and regenerative health solutions to healthcare practitioners in the United States.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative