Advertisement

- United States

- /

- Pharma

- /

- NasdaqGM:OCS

Is Oculis Holding’s New Equity Shelf Shaping a More Flexible Capital Strategy for OCS Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

- Oculis Holding AG has closed its previously filed shelf registration dated 10 November 2025, covering US$9.39 million of ordinary shares totaling 494,259 securities.

- This completed shelf registration, alongside the vesting of restricted stock units for a company director, highlights both Oculis’s evolving capital structure and its approach to equity-based compensation.

- We’ll now explore how the completion of this US$9.39 million shelf registration shapes Oculis’s investment narrative and capital-raising flexibility.

Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

What Is Oculis Holding's Investment Narrative?

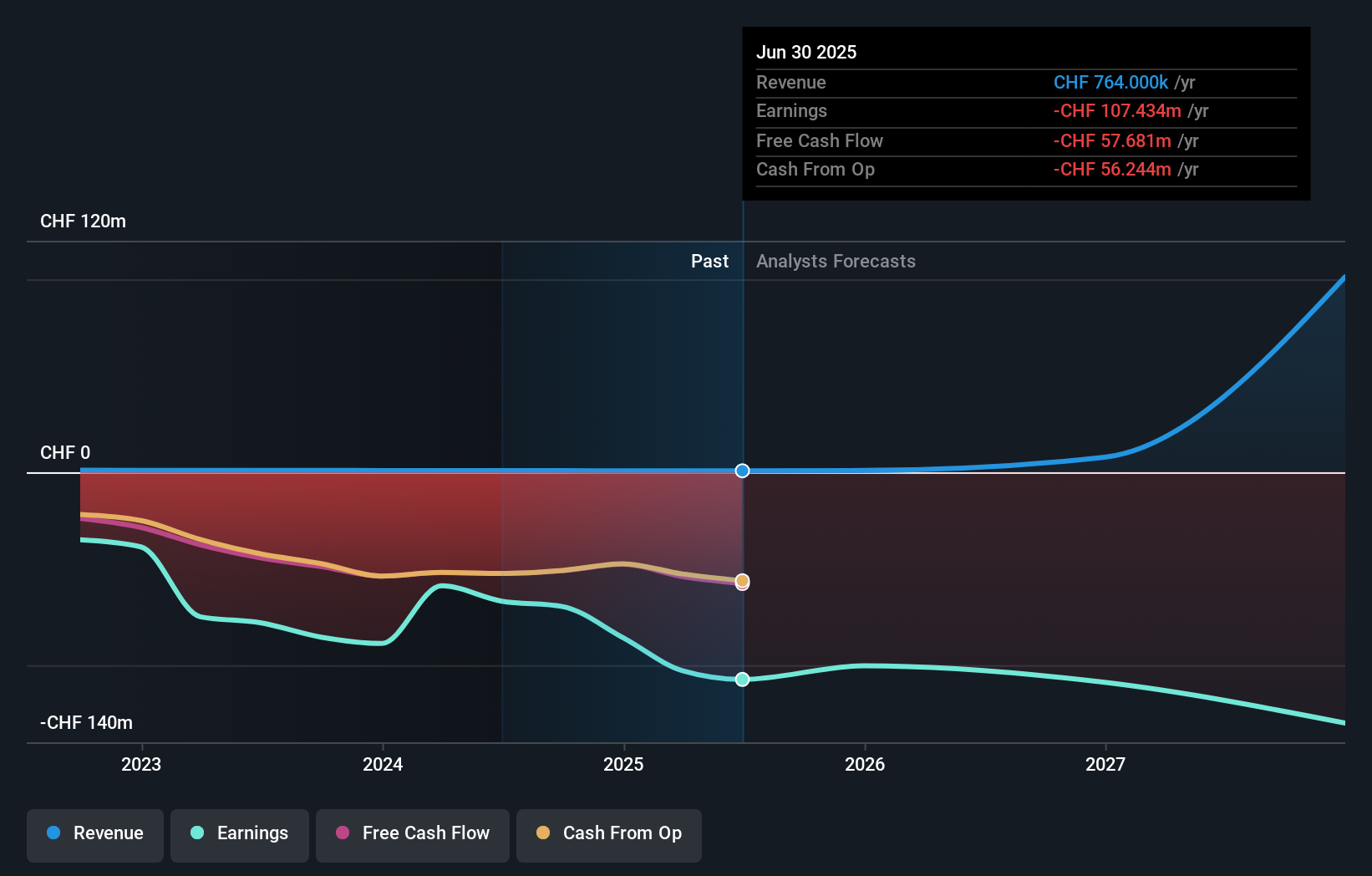

For Oculis, the core belief is that its ophthalmology pipeline, especially Privosegtor and OCS-01, can eventually justify heavy current losses and limited revenue, even at a rich price-to-book multiple. The recent closure of the US$9.39 million shelf registration, following the withdrawn US$100 million ATM and recent loan facilities, reinforces that the near-term story is still about securing flexible funding rather than changing the clinical or commercial timetable. This latest equity capacity looks small next to existing financing options, so it is unlikely to move the dial on key short term catalysts such as upcoming Privosegtor and OCS-01 milestones. It does, however, underline dilution and execution risk in a business that remains unprofitable and reliant on capital markets for runway extension. Yet there is one funding-related risk here that investors should not overlook.

In light of our recent valuation report, it seems possible that Oculis Holding is trading beyond its estimated value.Exploring Other Perspectives

The single fair value estimate from the Simply Wall St Community sits at US$44.69, suggesting a concentrated, optimistic view. Set this against Oculis’s ongoing losses and reliance on external funding, and it becomes clear why you may want to compare multiple viewpoints before deciding how its clinical and financing progress might influence future performance.

Explore another fair value estimate on Oculis Holding - why the stock might be worth just $44.69!

Build Your Own Oculis Holding Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Oculis Holding research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Oculis Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Oculis Holding's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:OCS

Oculis Holding

A clinical-stage biopharmaceutical company, develops drug candidates to treat ophthalmic diseases in Switzerland, Iceland, and internationally.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

45 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative