If you have been watching Collegium Pharmaceutical (COLL) lately, you have probably noticed the stock attract more attention after a prominent analyst upgrade. Zacks raised its rating to Strong Buy, citing a convincing upward trend in earnings estimates. Such analyst upgrades tend to spur investor enthusiasm, often amplifying hopes for solid performance ahead and sometimes shifting the risk appetite for the stock entirely.

This move comes as Collegium Pharmaceutical posts a mixed recent track record. The company delivered record revenue from Jornay PM and focused on deploying capital to benefit shareholders, although it missed earnings estimates last quarter. While shares are down around 10% over the past year, the stock has bounced back over the past three months, posting gains of nearly 15%, and its three- and five-year returns remain impressive. Even so, ongoing concerns over revenue declines and diminishing returns on capital have some investors questioning the sustainability of its long-term growth.

After riding this wave of renewed bullishness, the big question is whether the stock still represents a bargain or if the market is now fully pricing in future growth. Is this the right time to buy, or is the run-up set to stall?

Advertisement

Most Popular Narrative: 22.8% Undervalued

The most widely followed narrative suggests that Collegium Pharmaceutical is trading at a meaningful discount to its fair value, with upside potential based on future earnings strength and expanding profit margins.

Collegium's differentiated pain portfolio, notably with products featuring proprietary abuse-deterrent and extended-release technologies (for example, Xtampza ER's DETERx platform), is supported by industry and regulatory trends that increasingly favor safer opioid options. This is likely to enhance market share, pricing power, and sustain net margins as regulatory emphasis on abuse deterrence grows.

Think the market's already priced in the upside? This bold valuation actually rests on clear assumptions about shrinking risk, improved profitability, and a radical shift in earnings power over the next few years. Curious which key financial forecasts analysts are baking into their fair value, and if they stack up to scrutiny? The mystery lies in future profit margins and a valuation multiple that dares to defy industry norms.

However, the exclusivity loss from upcoming patent expirations and unpredictable regulatory shifts could challenge Collegium's bullish outlook and slow growth momentum.

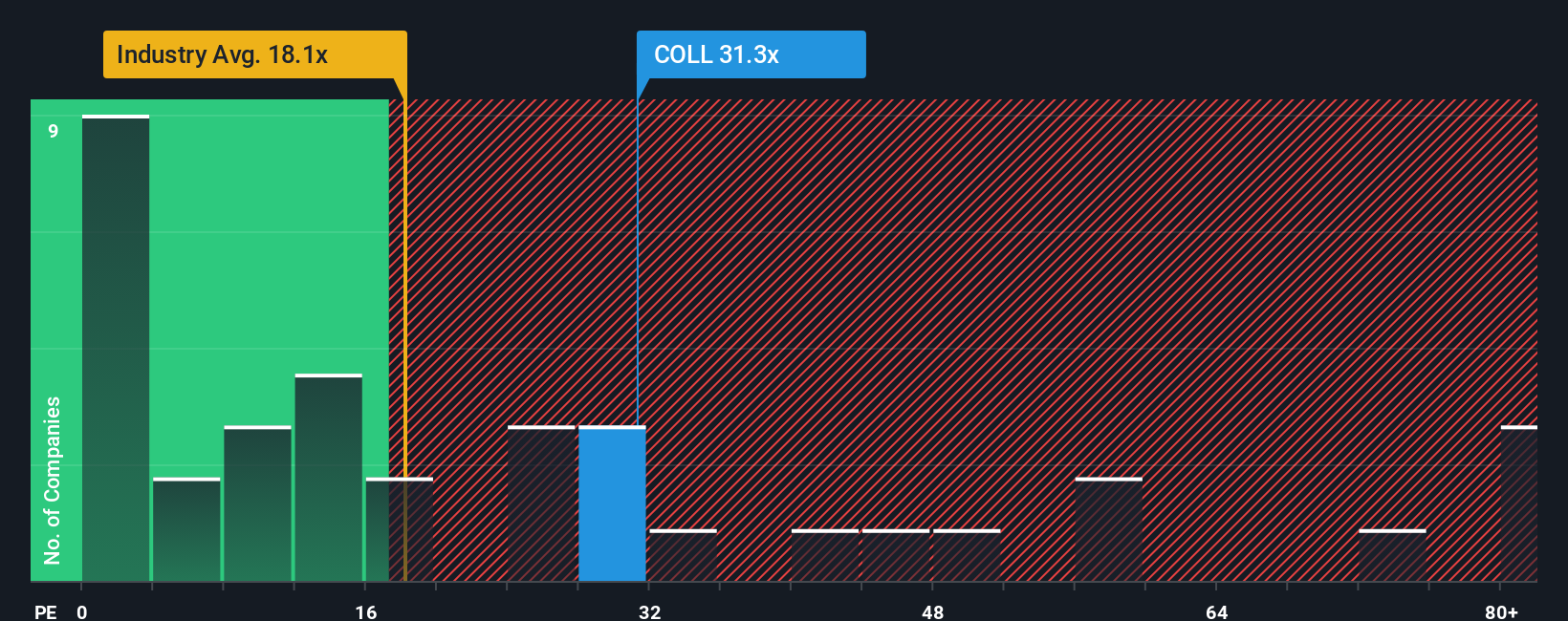

While many investors are drawn to analyst targets or discounted cash flow models, a look at how the company’s earnings multiple compares to the industry tells a different story and hints at potential overvaluation. Which story will prove right?

If you see things differently or want to investigate the numbers on your own terms, you can build your own analysis in just a few minutes. Do it your way

A great starting point for your Collegium Pharmaceutical research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors know that the winners of tomorrow might be found before everyone else catches on. See what else is catching momentum and don't let standout opportunities slip away.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies