Advertisement

- United States

- /

- Biotech

- /

- NasdaqCM:CELC

Does Celcuity’s 670% Surge Reflect Its True Value After Breakthrough Cancer Trial Updates?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if Celcuity is living up to all the buzz? Let’s take a closer look at whether its current share price really makes sense or if there is more here than first meets the eye.

- Celcuity’s stock has been on a remarkable run, climbing 3.7% in the past week and 36.7% in the last month. Additionally, it is up over 670% year-to-date and 690% over the past year.

- These moves have occurred alongside a series of notable developments, including the company’s recent advances in clinical studies and updates around its innovative cancer therapies. The industry has shown increased interest as Celcuity announced data that could influence how targeted treatments are approached, fueling both investor optimism and heightened risk appetite.

- Right now, Celcuity holds a valuation score of 2 out of 6. While this is not an exceptionally high rating, numbers only tell part of the story. Let’s examine how these valuation checks compare, and explore another way to look at this company’s value further ahead.

Celcuity scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Celcuity Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to today's value. This helps investors assess what a company is truly worth based on its potential to generate cash in the years ahead.

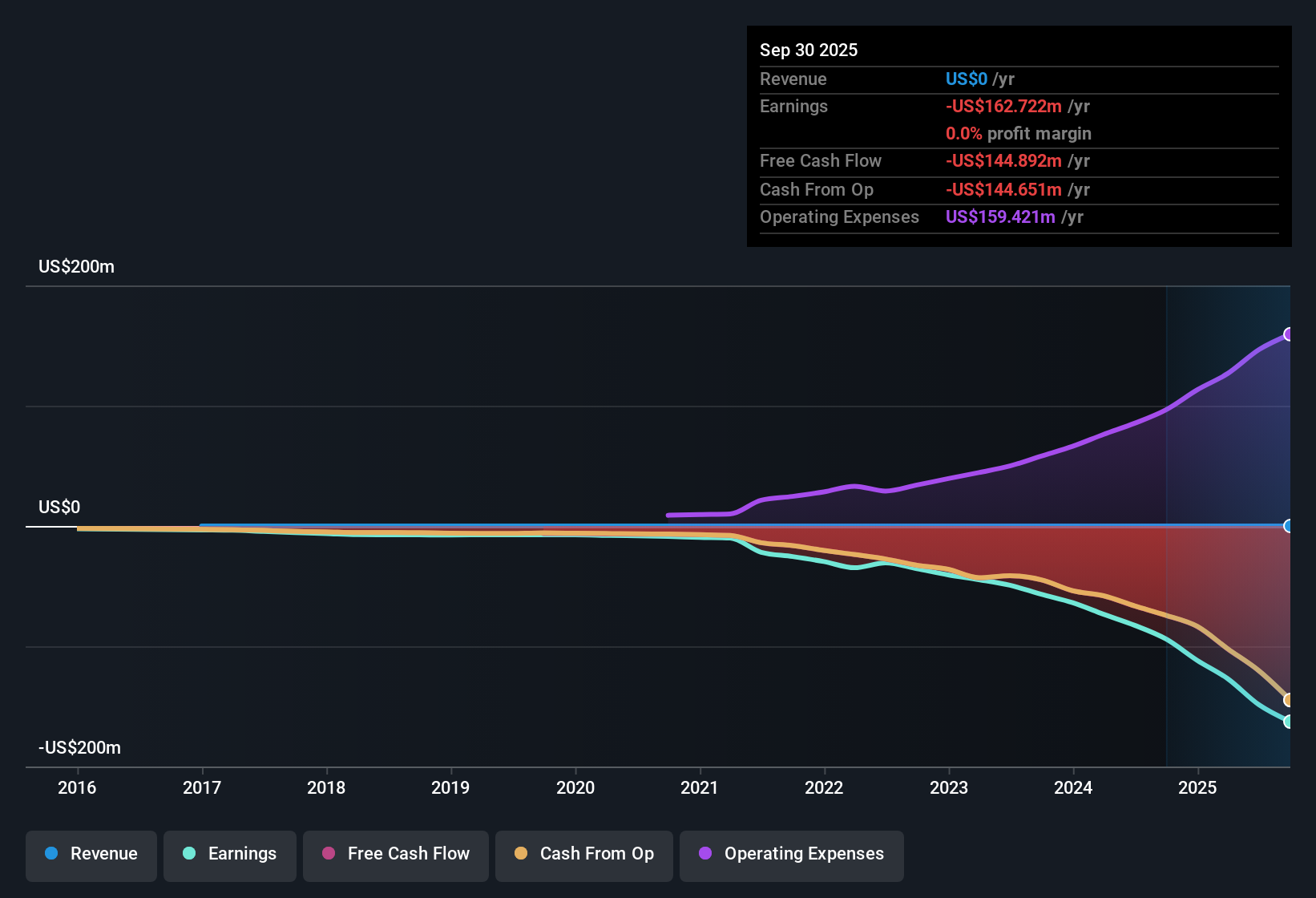

For Celcuity, the latest twelve months’ Free Cash Flow (FCF) is -$144.89 Million. Analyst forecasts suggest the company’s FCF could rise significantly, turning positive as growth initiatives take effect. By 2029, projections indicate FCF could reach $536.1 Million. Over a longer horizon, these cash flows are expected to rise further, with Simply Wall St estimating values over $1.3 Billion by 2035.

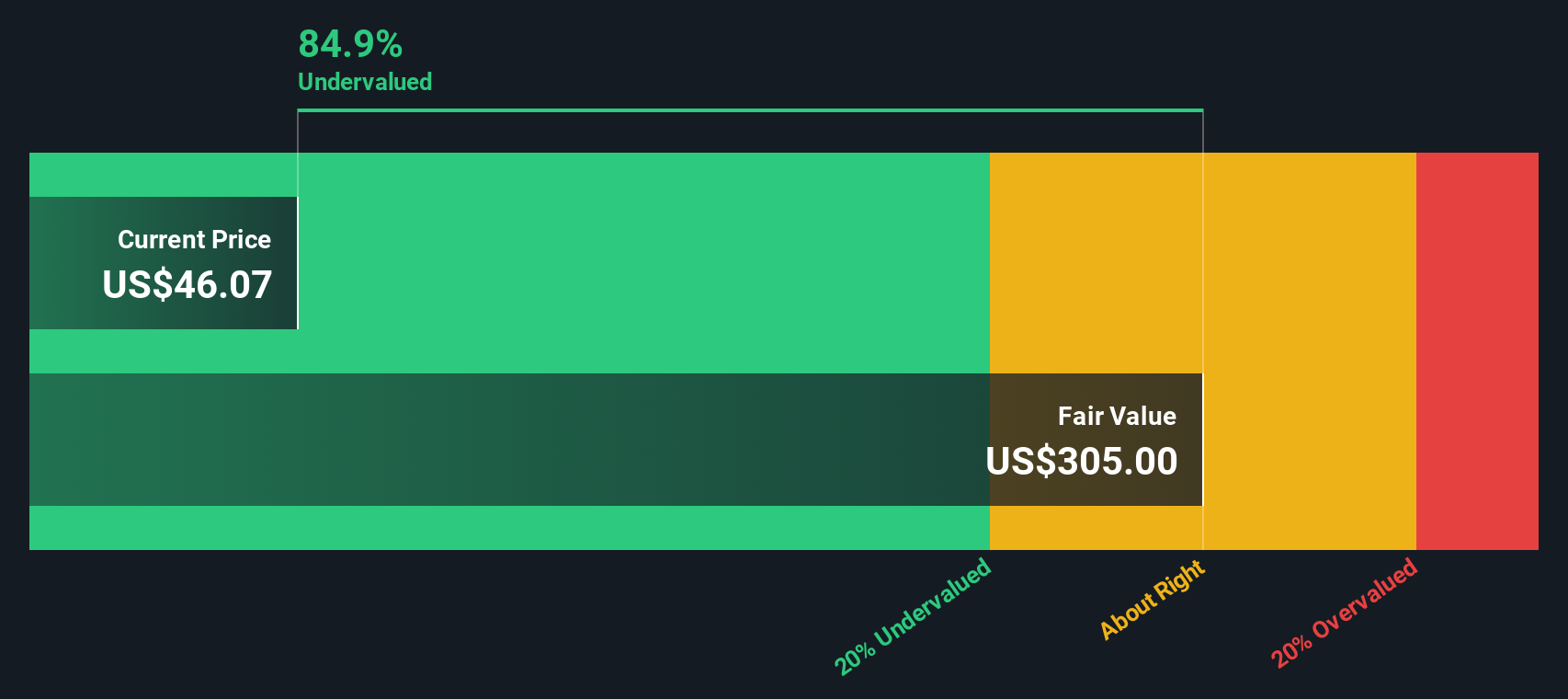

Using the DCF model, which relies on a 2 Stage Free Cash Flow to Equity approach, the estimated intrinsic value per share is $488.98. This calculation indicates that the current share price is trading at a 79.3% discount to its underlying cash flow value, which suggests the market may be undervaluing Celcuity’s long-term prospects.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Celcuity is undervalued by 79.3%. Track this in your watchlist or portfolio, or discover 922 more undervalued stocks based on cash flows.

Approach 2: Celcuity Price vs Book

The Price-to-Book (PB) ratio is often used to value biotech companies, especially those that are early-stage or not yet consistently profitable. This metric compares a company’s market value to its net assets and offers insight when earnings are volatile or negative, as is often the case in fast-growing biotech firms such as Celcuity.

A company’s PB ratio reflects how much investors are willing to pay for each dollar of net assets. Expectations for future growth or risk drive this number higher or lower. Faster-growing, more innovative companies tend to trade at a higher PB ratio relative to industry peers, while higher risk or less certain prospects can push it lower. The “normal” or “fair” PB ratio for any company is usually contextual and closely linked to the industry average and the company’s unique prospects.

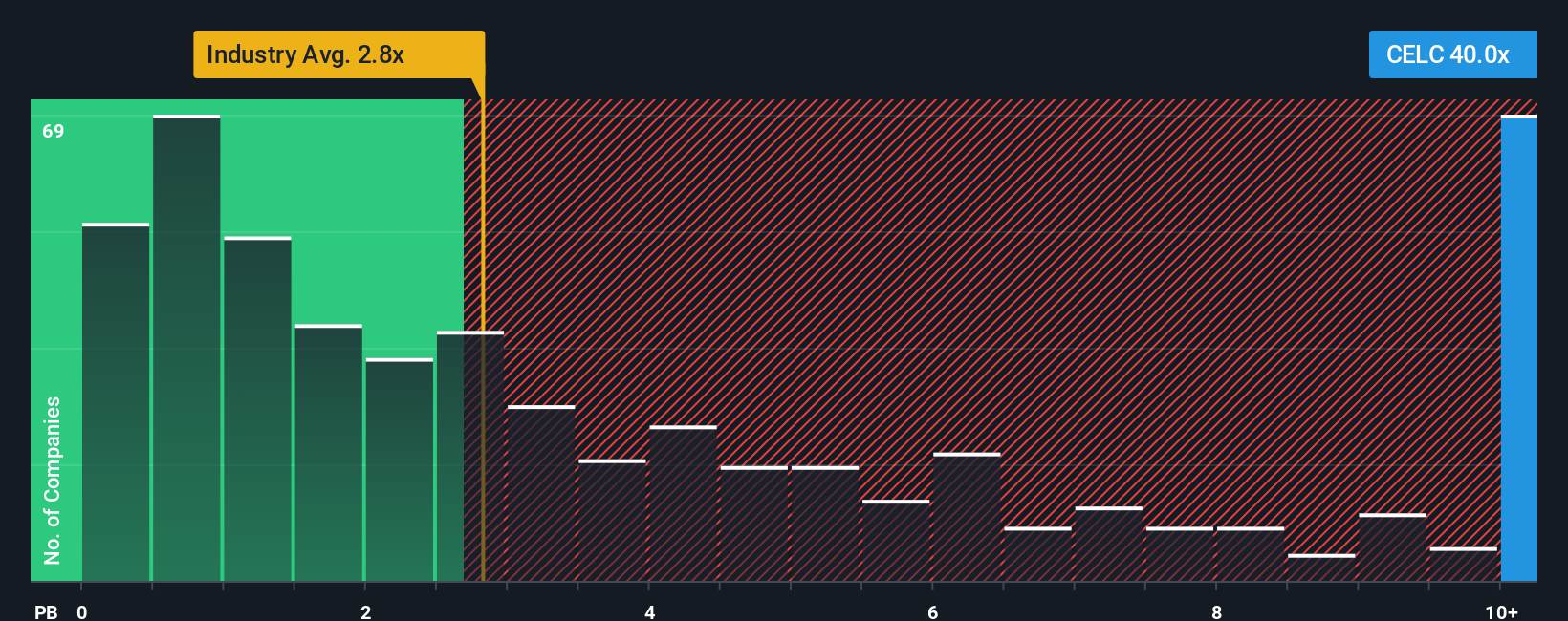

Currently, Celcuity trades at a PB ratio of 40.01x. This is significantly above the biotech industry average of 2.78x and the peer group’s average of 6.85x. While headline comparisons suggest a steep premium, it is important to consider whether this is justified by the company’s projected growth and risk profile.

This is where Simply Wall St's proprietary “Fair Ratio” comes in. Rather than just comparing to industry or peer averages, the Fair Ratio incorporates factors like expected earnings growth, profit margins, risk profile, and market cap. This provides a more tailored view of what’s reasonable for Celcuity specifically. Benchmarking only against peers or industry averages could miss the bigger picture, especially for companies with unique potential or challenges.

Comparing Celcuity’s current PB ratio to its Fair Ratio helps cut through the noise. If the current multiple closely matches the Fair Ratio, the stock can be seen as fairly valued given its unique circumstances. In Celcuity’s case, the difference between its actual PB ratio and the Fair Ratio suggests the stock is OVERVALUED at current levels.

Result: OVERVALUED

PB ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Celcuity Narrative

Earlier we mentioned that there's an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is a simple but powerful tool that lets you attach a personal story or perspective to a company’s numbers, such as your estimates for Celcuity’s fair value, future revenue, and margins. Narratives connect what you believe about the company’s potential directly to a financial forecast and ultimately to a fair value, making your investment thesis concrete and testable.

Millions of investors already use Narratives on Simply Wall St's Community page, where you can build, share, and update your outlook as new news or earnings arrive. By comparing your Narrative’s Fair Value to today’s market price, deciding when to buy or sell becomes more transparent and grounded in your own analysis. Narratives are updated dynamically whenever the underlying data changes, so your perspective always stays relevant.

For example, some Celcuity Narratives forecast robust success and see a fair value well above the current share price. Others take a more cautious view and expect a lower fair value based on different assumptions. With Narratives, you can make better decisions that reflect your unique view and adapt as new information unfolds.

Do you think there's more to the story for Celcuity? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:CELC

Celcuity

A clinical-stage biotechnology company, focuses on the development of targeted therapies for the treatment of various solid tumors in the United States.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative