Advertisement

- United States

- /

- Media

- /

- NasdaqGM:TTD

Is Trade Desk (TTD) Undervalued After a 67% Slide? A Fresh Look at Its Current Valuation

Simply Wall St

Reviewed by Simply Wall St

Trade Desk (TTD) has been under the spotlight lately as the stock continues to face pressure. With investor attention focused on its recent performance, questions are swirling about what comes next for the digital advertising platform.

See our latest analysis for Trade Desk.

It has been a tough year for Trade Desk shareholders, with the stock’s share price sliding nearly 67% since January and a one-year total shareholder return of -69%. While a weak 30-day share price return hints at fading momentum, these moves reflect ongoing volatility and shifting investor sentiment around digital advertising’s growth outlook.

If Trade Desk’s recent ups and downs have you rethinking your approach, now is a perfect moment to broaden your search and discover fast growing stocks with high insider ownership

After such a steep decline and a price well below analyst targets, is Trade Desk currently undervalued and poised for a rebound, or is the market already accounting for the company’s future growth potential?

Most Popular Narrative: 37.3% Undervalued

With Trade Desk’s last close at $39.11 and a narrative fair value of $62.33, the narrative consensus points to a large gap between today’s share price and what analysts expect as fair value. Investors are left wondering if recent pessimism has truly gone too far, or if there is more pain to come for this digital ad innovator.

The continued rapid shift of ad spend from linear TV to connected TV (CTV) is driving significantly faster growth for Trade Desk's highest-margin channel. Deepened relationships with leading CTV and streaming content partners (Disney, Netflix, Roku, LG, etc.) position Trade Desk to capture an outsized share of the expanding premium digital video ad market, which should accelerate revenue and earnings growth as CTV penetration increases globally.

Want to know what’s fueling the optimism behind that hefty fair value? It’s not just about ad spend trends. There is a key financial lever and a future profit multiple that buck the sector’s norms. The full narrative reveals which earnings assumptions could set Trade Desk apart. Will they hold up? Find out what drives the math behind that valuation.

Result: Fair Value of $62.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, potential challenges such as intensified competition from industry giants and Trade Desk’s reliance on large clients could threaten its current growth path.

Find out about the key risks to this Trade Desk narrative.

Another View: Multiples Tell a Cautionary Story

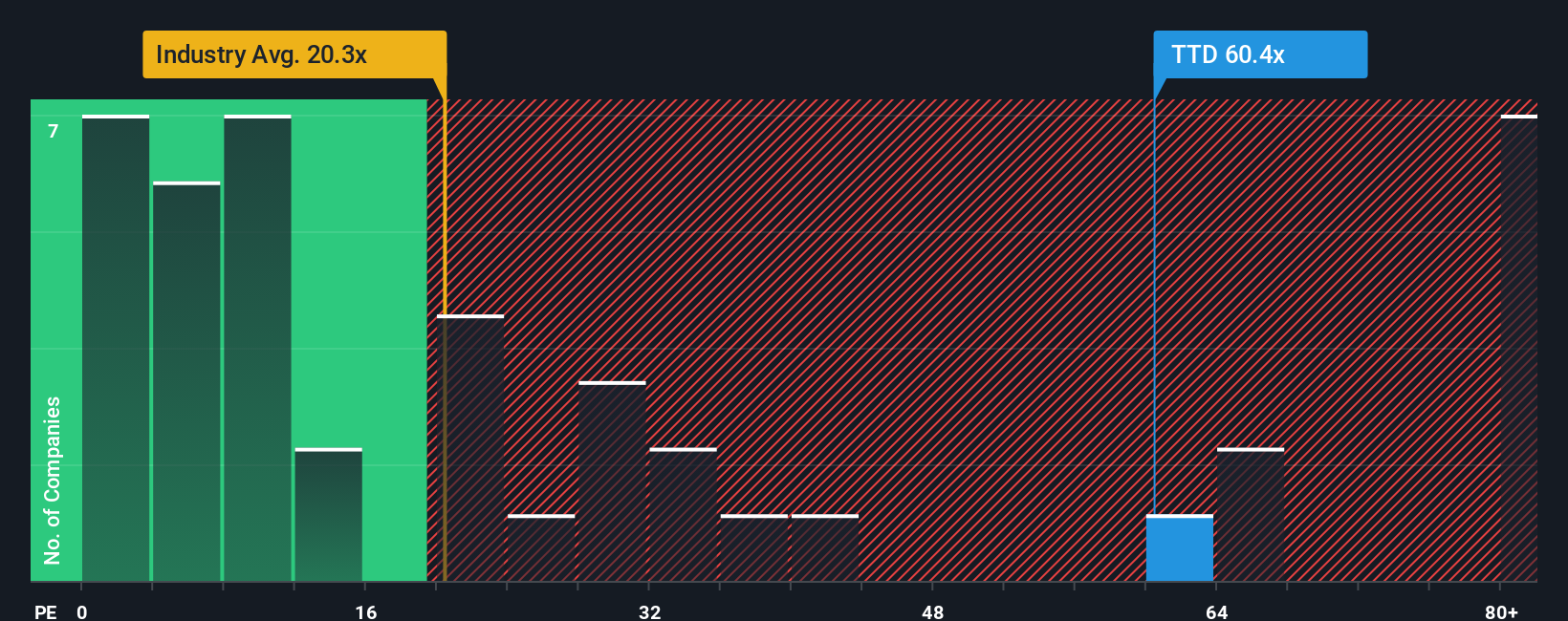

While the consensus fair value suggests Trade Desk is undervalued, a look at its price-to-earnings ratio offers a more cautious take. The company’s 43.1x ratio is much higher than both the peer average of 25.3x and the US Media industry’s 16.4x. It is also well above the fair ratio of 27.8x. This sizable gap highlights real valuation risk. Could the share price have further to fall if the market tunes its optimism?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Trade Desk Narrative

If you see things differently or want to crunch the numbers on your own, you can easily shape your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Trade Desk.

Looking for More Investment Ideas?

Don't let fresh opportunities slip away. If you're keen to expand your horizons or stay ahead of market trends, explore these smart ways to strengthen your portfolio:

- Spot long-term potential by reviewing these 927 undervalued stocks based on cash flows for companies trading below their intrinsic values and positioned to outperform as the market catches up.

- Maximize income streams by uncovering these 15 dividend stocks with yields > 3% with reliable yields above 3% and steady cash flow to support your returns even in uncertain times.

- Catch the next wave in tech as you navigate these 25 AI penny stocks shaping artificial intelligence breakthroughs and offering exposure to tomorrow’s innovation leaders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Trade Desk might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:TTD

Trade Desk

Operates as a technology company in the United States and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative