Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:TBLA

Taboola (TBLA): Assessing Valuation After Strong Earnings, Profit Return, and Upgraded Revenue Outlook

Simply Wall St

Reviewed by Simply Wall St

Taboola.com (TBLA) just reported higher quarterly sales and swung to a profit, while also raising its full-year revenue outlook. These updates are drawing new attention to the company’s stock this month.

See our latest analysis for Taboola.com.

Taboola.com’s strong earnings and upgraded revenue guidance have caught the market’s attention. This has helped fuel a 29.2% surge in its 1-month share price return and contributed to a notable 25.1% total shareholder return over the last year. Momentum has picked up recently, suggesting that investors may be seeing renewed growth potential after a few challenging years. However, the five-year total return remains deep in the red.

If you’re curious about which other stocks are capturing momentum right now, this could be the perfect moment to broaden your search and explore fast growing stocks with high insider ownership

With Taboola.com’s shares surging after upbeat results and guidance, the key question is whether the company is still trading below its true value or if expectations for future growth are already reflected in today’s price.

Most Popular Narrative: 9.9% Undervalued

Taboola.com's most widely followed narrative values the stock at $4.38 per share, above its last closing price of $3.94. This signals optimism about future earnings power, even as the market remains cautious about long-term growth.

The launch of Realize, Taboola's new performance advertising platform, is enabling entry into a much larger pool of display and social ad budgets. This positions the company to capture incremental revenue growth outside of traditional native ad formats. This is expected to materially expand the addressable market and drive a return to double-digit revenue growth in the coming years.

Want to know what’s fueling this optimistic valuation? The secret sauce is a bold new growth engine and some daring financial targets that set this stock apart from competitors. Discover which future numbers analysts are banking on—these projections might surprise you and could reshape your view of Taboola’s potential.

Result: Fair Value of $4.38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slower core growth and dependence on unproven new platforms could limit Taboola.com's ability to sustain the expected earnings acceleration that analysts anticipate.

Find out about the key risks to this Taboola.com narrative.

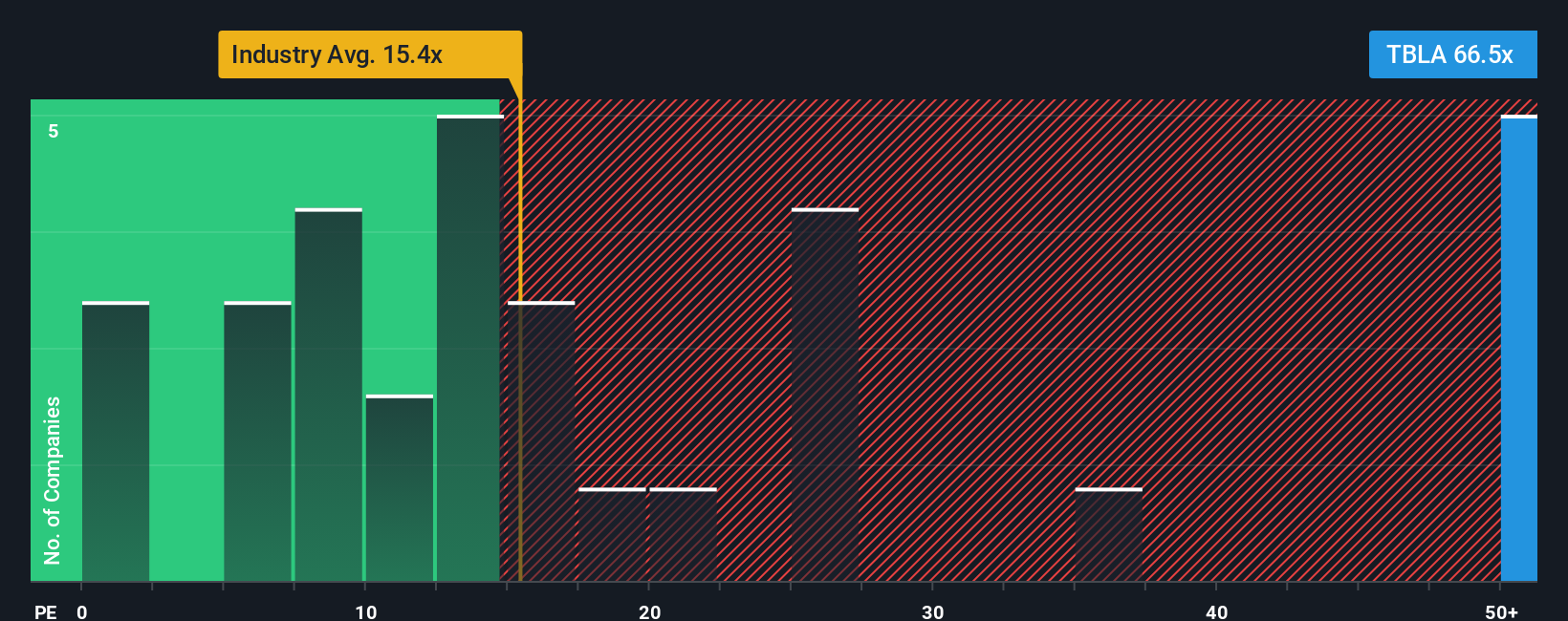

Another View: High Earnings Multiple Raises Concerns

While the fair value estimate suggests Taboola.com is undervalued, a glance at its price-to-earnings ratio tells a different story. The company trades at 44.9 times earnings, which is over three times higher than the US Interactive Media and Services industry average of 16.6x, and considerably above its own fair ratio of 19.6x. This large premium could expose shareholders to downside if market sentiment shifts or earnings disappoint. Is the current optimism already fully priced in?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Taboola.com Narrative

If you want to test your own perspective or look deeper than the consensus, you can shape your own story from the same data in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Taboola.com.

Looking for more investment ideas?

Smart investors never stand still. Now’s your chance to get ahead by uncovering breakthrough opportunities that could reshape your portfolio and set you up for future wins.

- Tap into the world of tomorrow by selecting these 27 AI penny stocks riding the biggest advances in artificial intelligence and transformative automation.

- Grow your income streams, and lock in stability and attractive yields when you select these 18 dividend stocks with yields > 3% built on a foundation of strong dividends.

- Seize the edge with these 905 undervalued stocks based on cash flows, those the market may be overlooking, and capture compelling value before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Taboola.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TBLA

Taboola.com

Operates an artificial intelligence-based algorithmic engine platform in Israel, the United States, the United Kingdom, Germany, and internationally.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative