Advertisement

- United States

- /

- Media

- /

- NasdaqGS:NXST

Is Nexstar Media Group Still a Bargain After Strong 19.9% Rally in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Nexstar Media Group's stellar run means it's still a smart buy, or if the market is getting ahead of itself? You're not alone. Let’s dig in to see what’s really driving the value here.

- The stock has delivered a strong 19.9% gain year-to-date and is up 101.3% over five years, hinting at both growth potential and perhaps a shift in how investors are assessing its future.

- Recent headlines spotlight Nexstar’s continued expansion into digital content and strategic partnerships. These moves are fueling optimism among investors. The company’s sizable footprint in local media and aggressive push into streaming have caught the market’s attention, potentially contributing to its recent momentum.

- On our valuation scale, Nexstar Media Group scores a solid 5 out of 6, meaning it ticks almost every box for being undervalued. Next, we’ll break down exactly how we get to that number and, even more importantly, look at a smarter way to spot real value hiding in plain sight.

Approach 1: Nexstar Media Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model helps estimate what a company is truly worth today by projecting its future cash flows and then discounting those back to their present value. This method is often favored for its focus on the actual cash the business is expected to generate over time, rather than current earnings or market sentiment.

For Nexstar Media Group, the most recent data shows Free Cash Flow at $964.1 million, with analysts expecting gradual growth ahead. According to these projections, Nexstar’s Free Cash Flow could grow to just under $1.3 billion by 2028, with further extrapolations suggesting continued gains through 2035. While analyst forecasts typically cover five years, Simply Wall St extends these estimates out to give a more comprehensive long-term picture.

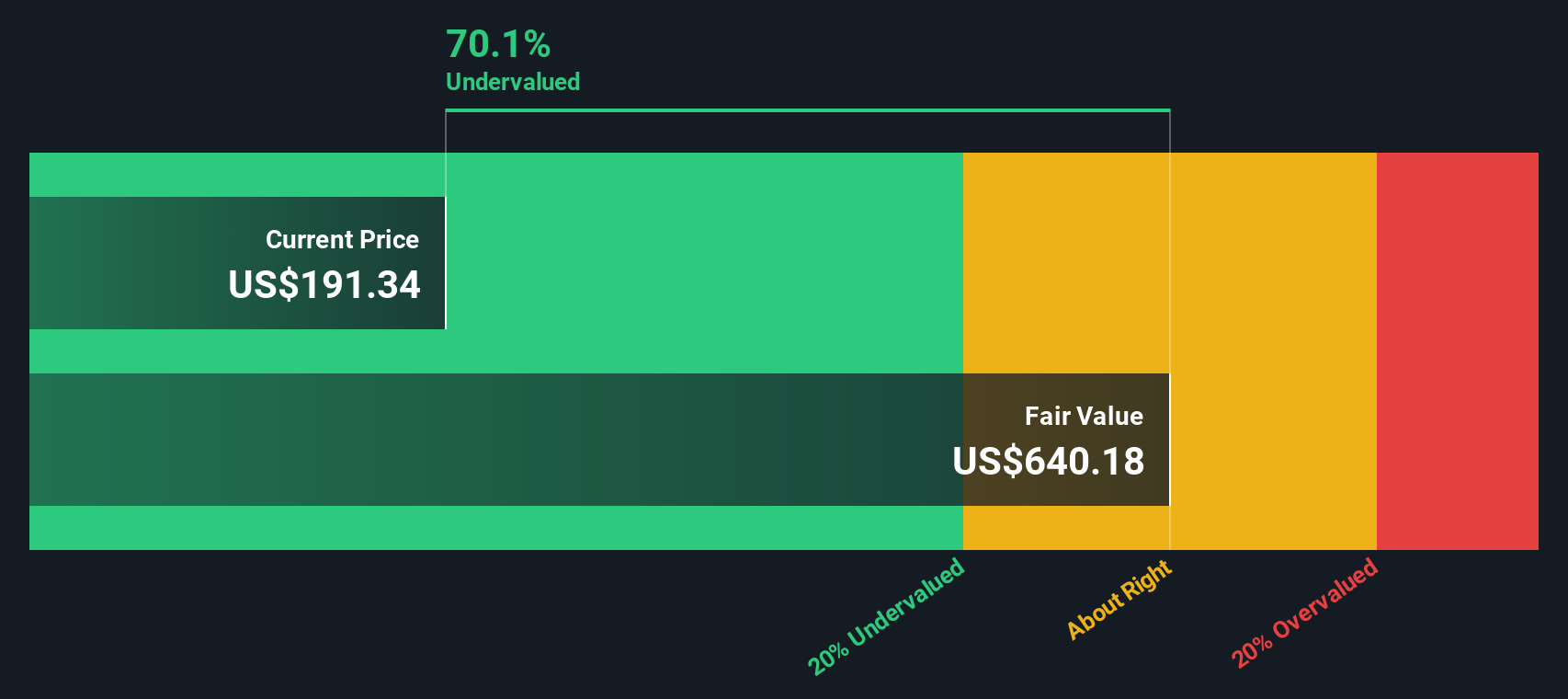

The result of this detailed cash flow modeling is an estimated intrinsic value of $795.42 per share. Compared to Nexstar’s current trading price, this suggests the stock is trading at a 76.0% discount to its calculated fair value. In other words, the market appears to be heavily undervaluing what Nexstar’s future cash flows could be worth today.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Nexstar Media Group is undervalued by 76.0%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

Approach 2: Nexstar Media Group Price vs Earnings

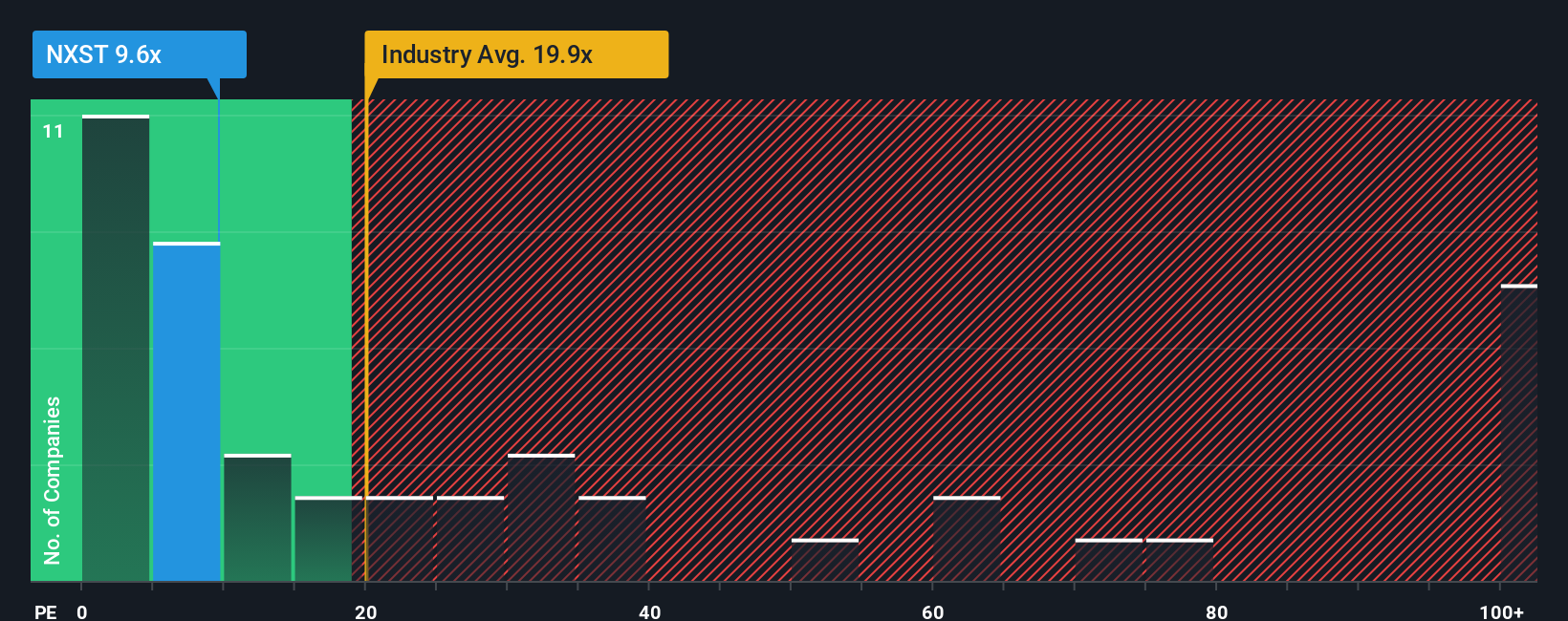

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies like Nexstar Media Group, as it compares a company’s share price to its earnings per share. For investors, the PE ratio offers a quick way to assess how much the market is willing to pay for each dollar of current earnings.

It is important to remember that higher expected growth or lower perceived risk typically justifies a higher "fair" PE ratio. Companies growing their earnings quickly or operating in stable industries generally attract premium valuations, while those with slower growth or more risk warrant lower PEs.

Nexstar Media Group is currently trading at an 11.56x PE multiple. This is above the average of its peers at 10.10x, but below the overall media industry average of 15.33x. According to Simply Wall St’s proprietary Fair Ratio model, which adjusts for factors like the company’s earnings growth outlook, profit margins, market capitalization, and broader risks, Nexstar’s fair PE ratio should be 18.82x. The Fair Ratio offers a more tailored benchmark than simply comparing with industry or peers because it reflects Nexstar’s individual fundamentals and risk profile instead of relying on general group averages.

Since Nexstar’s current PE ratio is well below its calculated fair value multiple, it suggests the stock is undervalued on this basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Nexstar Media Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are a way to combine your own view of a company's story, such as how you expect Nexstar's digital initiatives or political ad revenues to evolve, with your projections for future revenue, earnings, margins, and ultimately what you believe is a fair value for the stock.

With Narratives, you are not limited to just the numbers; you can anchor your investment decisions in the bigger picture by linking the company's strategic moves to tangible financial forecasts. This makes Narratives a practical and approachable tool, available directly on Simply Wall St’s Community page, where millions of investors are already sharing their perspectives.

Narratives help you decide exactly when to buy, hold, or sell by showing how your personal Fair Value compares with the current Price, and they are updated instantly as news events or earnings updates come in.

As an example, some investors might be optimistic about Nexstar’s broadcast consolidation and forecast a fair value of $250 per share, while others, more cautious about linear TV declines, may set a fair value as low as $190. This demonstrates how personal insights and expectations shape real-world investing decisions.

Do you think there's more to the story for Nexstar Media Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nexstar Media Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NXST

Nexstar Media Group

Operates as a diversified media company that produces and distributes local and national news, sports, and entertainment contents on the television and digital platforms in the United States.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative