Advertisement

- United States

- /

- Entertainment

- /

- NasdaqGS:IQ

How Investors May Respond To iQIYI (IQ) Reversing to Q3 Net Loss Amid Falling Revenue

Simply Wall St

Reviewed by Sasha Jovanovic

- iQIYI, Inc. recently announced its third-quarter 2025 results, reporting revenue of CNY 6,682.39 million, down from CNY 7,245.68 million a year earlier, and a net loss of CNY 248.93 million compared to net income of CNY 229.41 million in the same period last year.

- This marks a reversal from profitability to loss, highlighting the company's increased vulnerability to weaker content cycles and ongoing economic pressures in China.

- We’ll now assess how iQIYI’s swing to net loss and lower revenue could reshape its investment narrative and future outlook.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

iQIYI Investment Narrative Recap

For anyone considering iQIYI, the core belief centers on the company's ability to consistently deliver hit original content and translate this into stable subscription and advertising revenue. The third-quarter swing from net income to loss, alongside continuing revenue declines, directly impacts the most important short-term catalyst, renewed subscriber and advertiser momentum through compelling programming, while also highlighting the heightened risk of revenue volatility in a challenging content cycle. This news is material, as it may further pressure near-term profitability and visibility.

Among recent developments, the October premiere of The Blooming Journey Season 2 stands out as most relevant, aiming to boost user engagement and offset weaker quarters with highly anticipated content launches. However, as these releases are tested against softer demand, the company’s ability to reignite top-line growth could hinge on whether such shows generate enough viewership and buzz to reverse membership or advertising declines.

On the flip side, investors should be particularly aware of the persistent risk that, if blockbuster content production slips or fails to connect with audiences, the company’s top-line recovery could stall…

Read the full narrative on iQIYI (it's free!)

iQIYI's narrative projects CN¥29.2 billion revenue and CN¥1.3 billion earnings by 2028. This requires 1.8% yearly revenue growth and a CN¥1.21 billion increase in earnings from CN¥88.5 million today.

Uncover how iQIYI's forecasts yield a $2.33 fair value, a 5% upside to its current price.

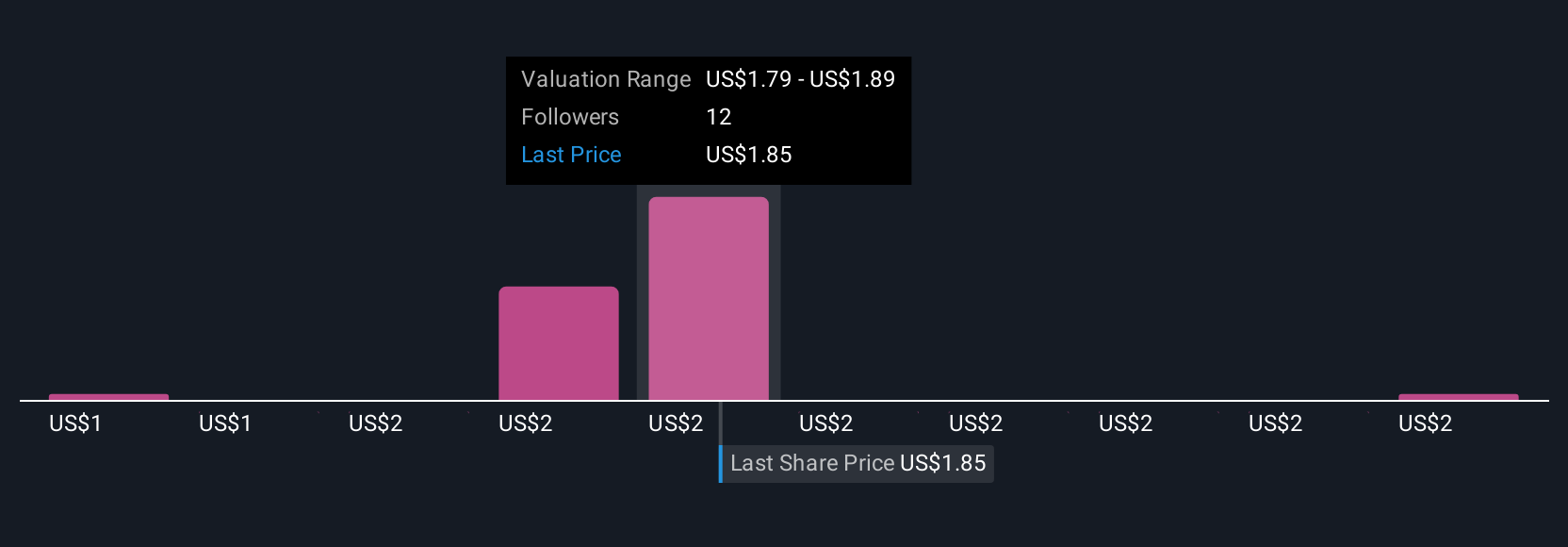

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community range widely, from CN¥1.38 to CN¥3.34 per share. In light of iQIYI's recent net loss and declining revenue, this range reflects how much your outlook may depend on confidence in a rebound fueled by successful content releases.

Explore 5 other fair value estimates on iQIYI - why the stock might be worth as much as 50% more than the current price!

Build Your Own iQIYI Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your iQIYI research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free iQIYI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate iQIYI's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if iQIYI might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IQ

iQIYI

Through its subsidiaries, provides online entertainment video services in the People’s Republic of China.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative