Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:WS

Worthington Steel (WS): Assessing Valuation After a Recent Turn in Share Price Momentum

Simply Wall St

Reviewed by Simply Wall St

Worthington Steel (WS) has quietly put together a steady run, with the stock up about 12% over the past month and 14% in the past 3 months, despite a weaker 1 year return.

See our latest analysis for Worthington Steel.

That recent 30 day share price return of just over 12 percent and the 90 day gain of about 14 percent suggest momentum is improving, even though the 1 year total shareholder return remains firmly negative. This indicates that sentiment has only recently started to turn.

If you are weighing up where else to put fresh capital in this market, it is worth scanning fast growing stocks with high insider ownership for other ideas with strong momentum behind them.

With the shares trading only slightly below analyst targets and showing modest fundamentals rather than explosive growth, the key question now is whether Worthington Steel is quietly undervalued or if the market already anticipates its next leg higher.

Most Popular Narrative: 2% Undervalued

The current share price of $35.30 sits just below the most followed fair value estimate of $36.00, setting up a modest valuation gap.

Analysts expect earnings to reach $169.8 million (and earnings per share of $3.36) by about September 2028, up from $110.7 million today. In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.8x on those 2028 earnings, down from 14.2x today.

Want to see how steady revenue growth, rising margins and a lower future earnings multiple still add up to a higher fair value estimate? The narrative spells out the full math and the assumptions driving it, but keeps one key growth lever surprisingly bold. Curious which one it is and how it shapes that $36 target?

Result: Fair Value of $36 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer volumes, weaker pricing, and lingering macro uncertainty in automotive and construction could easily derail those upbeat growth and valuation assumptions.

Find out about the key risks to this Worthington Steel narrative.

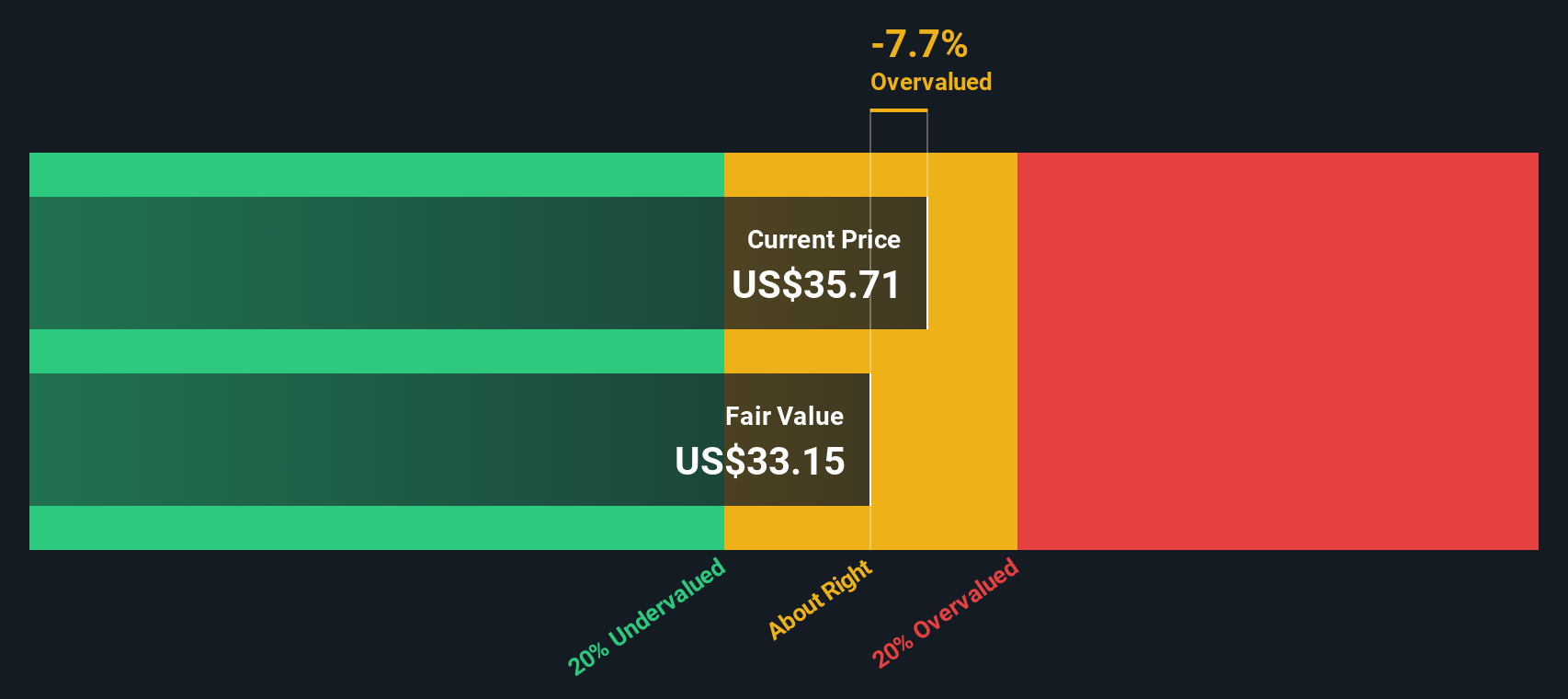

Another View: When Fair Value Flips

While the analyst narrative points to a small upside, our DCF model paints a cooler picture, with Worthington Steel trading above its estimated fair value of $33.09. If cash flows do not ramp as expected, today’s price could already be baking in too much optimism.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Worthington Steel for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 903 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Worthington Steel Narrative

If you see the story differently or want to dive into the numbers yourself, you can build a personalized narrative in under three minutes: Do it your way.

A great starting point for your Worthington Steel research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by using the Simply Wall St Screener to spot strong, focused themes you might otherwise overlook.

- Capture potential high-upside moves early by scanning these 3581 penny stocks with strong financials that pair smaller market caps with surprisingly solid financial underpinnings.

- Capitalize on structural growth trends by targeting these 30 healthcare AI stocks that blend medical innovation with cutting edge data driven technology.

- Strengthen your income stream by filtering for these 15 dividend stocks with yields > 3% that aim to deliver reliable cash payouts above typical market yields.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Worthington Steel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WS

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RA

RacerBVN on iShares Trust - iShares Preferred and Income Securities ETF ·

This one is all about the tax benefits

Fair Value:US$54.5543.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FatPie on SoFi Technologies ·

Estimated Share Price is $79.54 using the Buffett Value Calculation

Fair Value:US$79.5465.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

961 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative