Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:HCC

A Look at Warrior Met Coal’s (HCC) Valuation Following Strong Q3 Results and Blue Creek Progress

Simply Wall St

Reviewed by Simply Wall St

Warrior Met Coal (HCC) topped expectations in its third-quarter 2025 earnings report, posting stronger than anticipated revenue and earnings per share. UBS responded by maintaining its Neutral stance and raising its outlook after the company’s continued operational momentum.

See our latest analysis for Warrior Met Coal.

Shares of Warrior Met Coal have gained momentum recently, with a 20.3% share price return over the past month and a 31.2% gain over the last 90 days, as investors respond positively to the company’s strong operational updates and project de-risking. Over the longer term, the stock boasts a robust track record, delivering a 12.99% total shareholder return in the past year and an impressive 126% total return over three years. This is clear evidence that confidence is building behind the company’s growth story.

If this surge in momentum has you curious about other standouts, it could be the perfect time to broaden your strategy and discover fast growing stocks with high insider ownership

Still, with the stock’s strong rally and a price now approaching analysts’ targets, investors must ask whether there is real value left on the table or if the market has already factored in the company’s next phase of growth.

Most Popular Narrative: 3.3% Undervalued

With the latest consensus narrative projecting a fair value of $80 for Warrior Met Coal, the last close price of $77.38 is just below this target. This suggests analysts see a small but meaningful upside. Here’s a catalyst the narrative identifies as central to the company’s thesis.

"The ahead-of-schedule and on-budget launch of the Blue Creek longwall in early Q1 2026 accelerates Warrior Met Coal's transition from capital investment to higher-volume revenue generation. This unlocks increased production capacity along with lower-cost, higher-quality tons, positioning the company to grow both revenues and net margins as volumes ramp and cost efficiencies are realized."

Curious what’s fueling this valuation? The narrative's bold case leans on a transformative project, bets on margin expansion, and assumptions that could surprise even seasoned market watchers. Which crucial financial projection tips the scales? Only the full narrative has the details.

Result: Fair Value of $80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weakness in global steel demand or increased exposure to price competition in key Asian markets could quickly erode the company’s margin outlook.

Find out about the key risks to this Warrior Met Coal narrative.

Another View: What Multiples Say

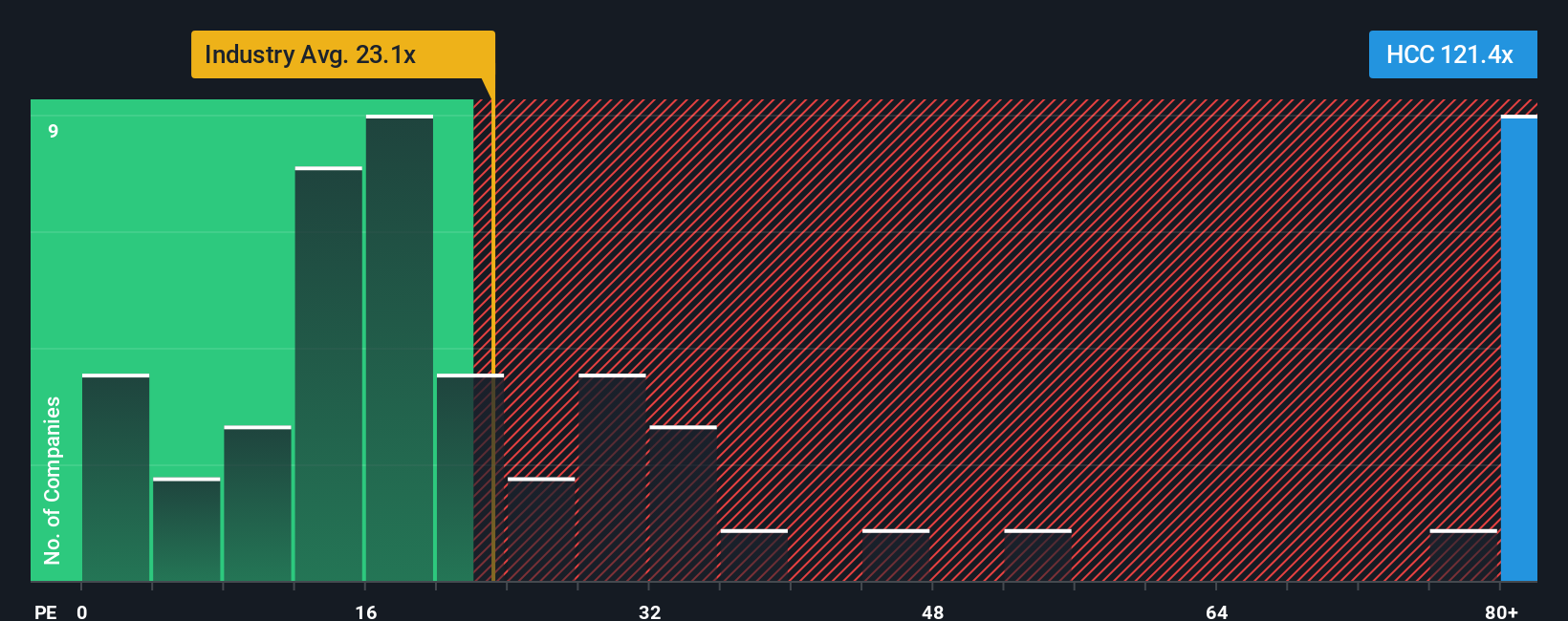

Taking a closer look at Warrior Met Coal’s valuation through the lens of the price-to-earnings ratio reveals a different story. Warrior Met’s P/E stands at 115.7x, which is much higher than the industry average of 21.4x, its peer average of 35x, and notably above the fair ratio of 73.9x. Such a large gap may point to expectations that are already baked in and could raise the risk of a pullback if future growth falls short. Could this signal that the stock’s current price reflects more optimism than value?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Warrior Met Coal Narrative

If this perspective doesn't quite align with your own research style, consider diving into the numbers and shaping your own view in just a few minutes. Do it your way

A great starting point for your Warrior Met Coal research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t wait for the next opportunity to pass by. Gain an edge and spot hidden gems by evaluating fresh ideas tailored to your strategy with these hand-picked themes:

- Boost your passive income by scanning these 14 dividend stocks with yields > 3%, which offers yields above 3% and resilient payout records.

- Uncover the next wave in medicine by exploring these 30 healthcare AI stocks, where artificial intelligence is transforming healthcare for tomorrow’s breakthroughs.

- Capture untapped potential among innovators by seeking out these 3582 penny stocks with strong financials with strong financial foundations and breakout momentum.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Warrior Met Coal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HCC

Warrior Met Coal

Engages in the production and export of non-thermal steelmaking coal for the steel production by metal manufacturers in Europe, South America, and Asia.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative