Progressive (PGR) shares have dropped sharply after the company posted disappointing third-quarter earnings, as important measures like combined ratio and net premiums earned missed expectations. The pullback deepened because several analysts issued downgrades in response to the report.

Progressive’s sharp pullback comes on the heels of both a subdued third quarter and a flurry of analyst downgrades, but it’s worth noting that the recent selling may overstate near-term challenges. Despite a roughly 5% year-to-date share price decline and a 13% drop in total shareholder return over the past year, the company’s strong multi-year run remains intact. Total shareholder returns have climbed a striking 77% and 182% over the last three and five years, respectively. Recent news, such as the expanded agency relationship with Coterie and robust October policy growth, shows the underlying business is still evolving and capable of weathering short-term volatility.

With the stock down sharply from its highs and analyst sentiment split, the question becomes whether Progressive is trading at a meaningful discount or if the market has already factored in future growth. Could this be a compelling entry point for investors?

Advertisement

Most Popular Narrative: 11.1% Undervalued

The most widely followed narrative places Progressive’s fair value well above its last close, suggesting analyst consensus still sees significant upside from current levels. Recent price moves have not shifted the margin of undervaluation built into this fair value estimate, despite mixed earnings and divided analyst sentiment.

Progressive's scale, superior data analytics, and rapid pricing response mechanisms position the company to win disproportionate market share as technology-driven direct-to-consumer distribution continues to outpace traditional agents. This directly supports outperformance in net premiums written and long-term earnings growth.

Curious what numbers justify such optimism? The narrative price target is anchored by a blend of rising sales, profit margin adjustments, and an eye-catching future profit multiple. Which financial lever is the main reason for this bullish fair value? Explore the details and see what assumptions could shift the story in either direction.

However, rising claim costs and intensifying competition could undermine Progressive’s margin improvement. This may potentially reduce future earnings growth and challenge the bullish valuation case.

Another View: Multiple-Based Valuation Signals Caution

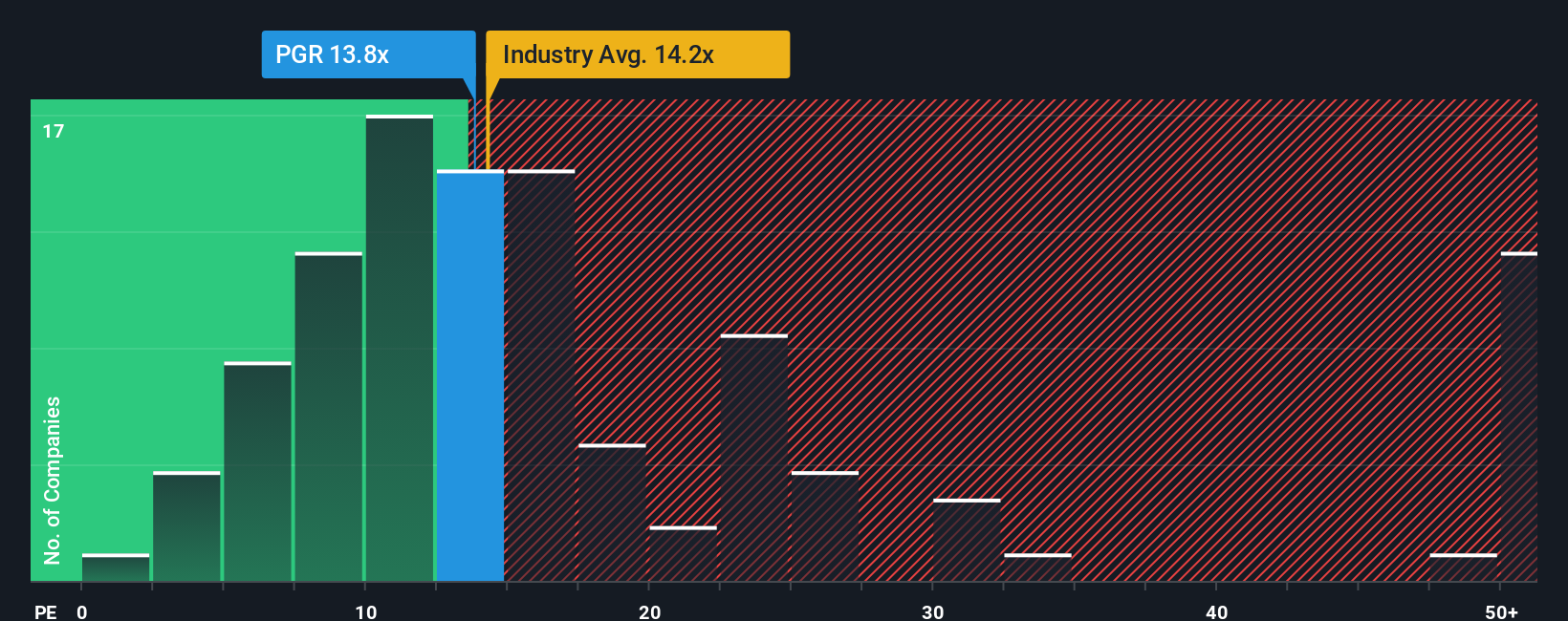

While the narrative-based fair value appears positive, comparing Progressive’s price-to-earnings ratio with its peers and industry provides a more skeptical perspective. At 12.5x, the ratio is higher than the peer average of 9.6x and its fair ratio of 10.7x, but lower than the broader industry’s 13.2x.

This disconnect introduces valuation risk. If the market adjusts, Progressive’s price could move closer to the fair ratio. This raises the question of whether the optimism in the price is justified or if there is potential for a decrease.

If the consensus doesn’t align with your view, or if you’d like to dig into the numbers and trends yourself, you can easily craft your own perspective in just a few minutes with Do it your way.

Don’t limit your search to a single stock when there is a world of opportunity waiting for you. Use these powerful tools to find under-the-radar gems that could deliver your next big win.

Maximize your income with high-yield picks by tapping into these 15 dividend stocks with yields > 3%, which includes stocks offering strong, reliable dividends above 3%.

Gain early access to breakthroughs by targeting these 25 AI penny stocks, designed to benefit from advances in artificial intelligence and next-generation solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks