Advertisement

- United States

- /

- Insurance

- /

- NYSE:MMC

Marsh McLennan (MMC): Assessing Valuation After $6 Billion Share Buyback Announcement

Simply Wall St

Reviewed by Simply Wall St

Marsh & McLennan Companies has authorized a new share repurchase program, with plans to buy back up to $6 billion of its own stock. This move often signals management's confidence in the business and can impact shareholder value.

See our latest analysis for Marsh & McLennan Companies.

While Marsh & McLennan Companies' $6 billion buyback is making headlines, it follows a period of heightened activity including leadership changes and a strategic tech focus. Despite the vote of confidence from management, the stock’s share price return is down 13.6% so far this year and total shareholder return for the past twelve months sits at -20.4%, in contrast to strong gains over longer timeframes. Momentum has faded recently but the company’s long-term total return of nearly 68% over five years tells a more resilient story.

If you’re looking for the next compelling opportunity beyond insurance, now may be the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With a sizeable buyback in play and recent underperformance raising eyebrows, the key question is whether Marsh & McLennan Companies is now trading at a bargain or if the market has already priced in all the growth ahead.

Most Popular Narrative: 14.7% Undervalued

Compared to Marsh & McLennan Companies' recent closing price of $182.70, the most widely followed narrative assigns a fair value of $214.26. This suggests the market may be overlooking some crucial drivers of future upside. Unpacking the rationale, analysts have weighed growth prospects, earnings power, and sector headwinds to arrive at this higher valuation.

Strategic investments in digital transformation, advanced analytics, and AI (for example, proprietary data tools for risk modeling and agentic interfaces) are expected to enhance operational efficiency and improve product and service offerings. This could enable margin expansion and net earnings growth through improved client retention and lower cost to serve.

Wondering what bold assumptions are behind this valuation surge? The narrative’s calculations rest on a future profit leap, ambitious growth bets, and margin upgrades not yet reflected in the share price. Are you ready to uncover how those projections stack up to market expectations?

Result: Fair Value of $214.26 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent declines in pricing and ongoing consulting demand uncertainty could challenge the optimistic narrative around Marsh & McLennan’s future prospects.

Find out about the key risks to this Marsh & McLennan Companies narrative.

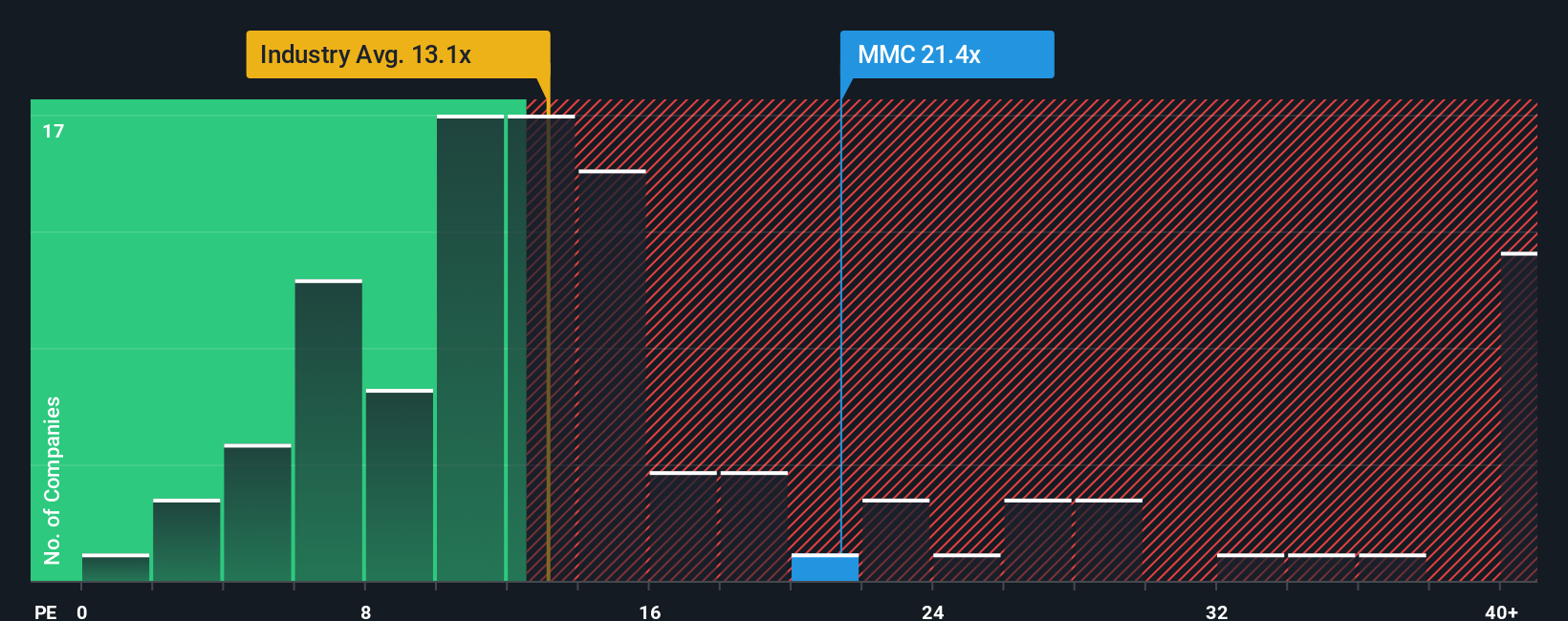

Another View: A Look at Valuation Multiples

While the narrative leans toward undervaluation, looking at Marsh & McLennan Companies' price-to-earnings ratio tells a different story. The company is trading at 21.7x earnings, higher than the US insurance sector average of 13.2x and the estimated fair ratio of 15.3x. This pricing gap could signal caution if the market adjusts toward those lower benchmarks. So, is the margin of safety real, or could valuation risk still loom large?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Marsh & McLennan Companies Narrative

If you want to dig deeper into the numbers or challenge the prevailing story, you can quickly create your own Marsh & McLennan Companies narrative in just a few minutes. Do it your way

A great starting point for your Marsh & McLennan Companies research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Ways to Strengthen Your Portfolio?

Smart investors always scan for tomorrow’s standouts. Take five minutes now and tap into these tailored investment themes before the next big market move passes you by.

- Accelerate your passive income goals and spot top yield opportunities with these 15 dividend stocks with yields > 3%. These consistent options often compare favorably to low-interest bank accounts.

- Explore breakthrough innovations with these 30 healthcare AI stocks, which continues to transform how we detect, treat, and manage health on a global scale.

- Find unique opportunities with these 3579 penny stocks with strong financials that combine strong financials and the potential for outsized returns, ahead of the crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MMC

Marsh & McLennan Companies

A professional services company, provides advisory services and insurance solutions to clients in the areas of risk, strategy, and people worldwide.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative