Advertisement

- United States

- /

- Insurance

- /

- NYSE:FIHL

Quarterly Profit Rebound Might Change The Case For Investing In Fidelis Insurance Holdings (FIHL)

Simply Wall St

Reviewed by Sasha Jovanovic

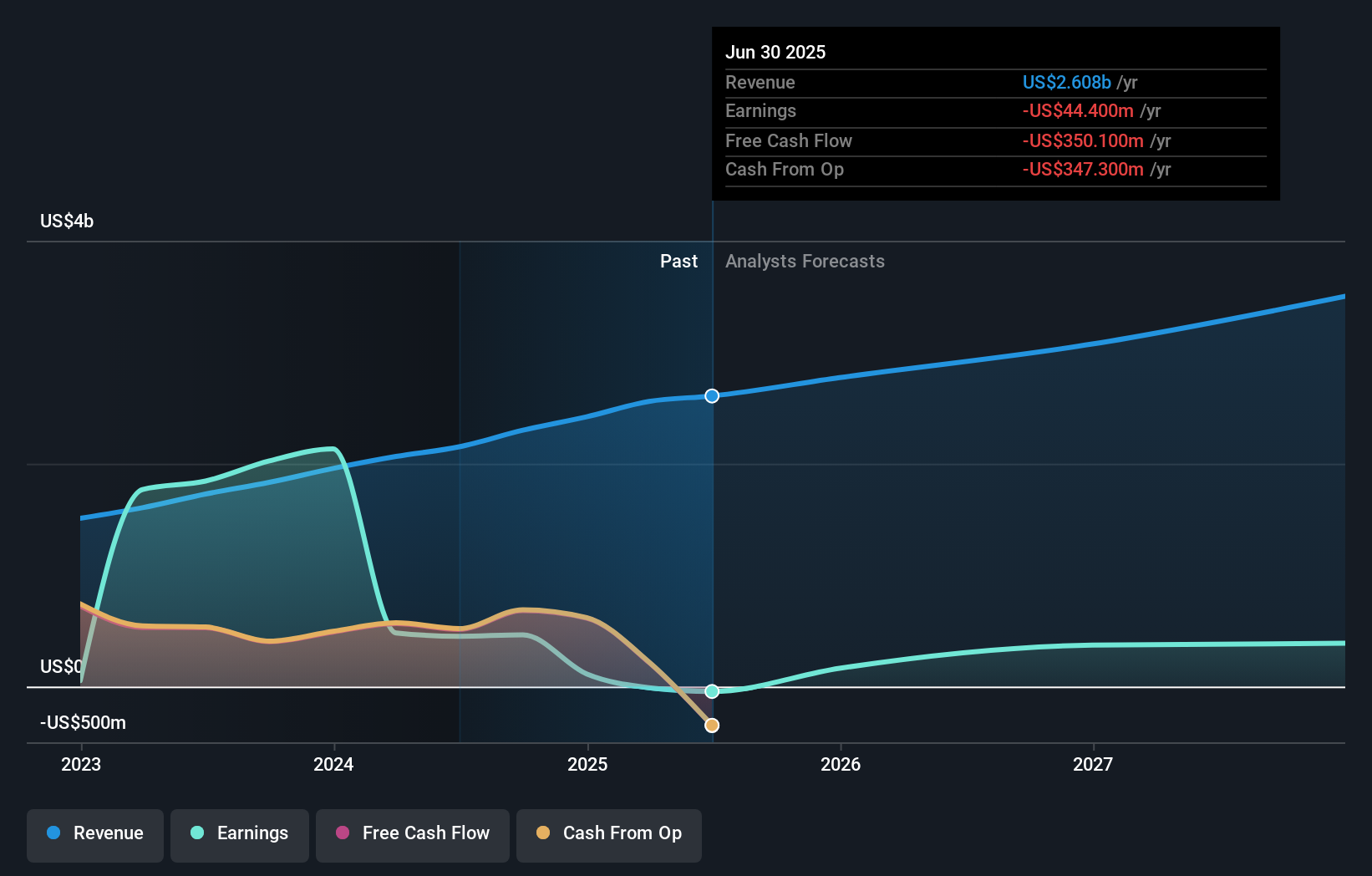

- Fidelis Insurance Holdings Limited recently announced financial results for the third quarter and nine-month period ended September 30, 2025, reporting quarterly revenue of US$651.9 million and net income of US$130.5 million.

- Despite lower nine-month net income versus the prior year, the company recorded higher quarterly earnings per share, indicating improved short-term profitability amid shifting revenue trends.

- We'll explore how the rebound in quarterly net income shapes Fidelis Insurance Holdings' investment narrative and future outlook.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Fidelis Insurance Holdings Investment Narrative Recap

Fidelis Insurance Holdings appeals to investors who are confident in specialty insurers’ ability to sustainably grow premium and earnings, particularly in property and catastrophe-exposed lines, by leveraging data-driven underwriting and capital-light models. The company’s latest results show a rebound in quarterly profitability, but the overall impact on short-term performance drivers appears limited, with the biggest immediate risk remaining exposure to large catastrophe losses and ongoing claims volatility, rather than one-off quarterly swings in net income.

Among recent announcements, Fidelis’s ongoing share repurchase program, totaling over US$166 million to date, stands out. This initiative reflects management’s focus on enhancing shareholder value and may help offset short-term earnings volatility, though it does not materially alter the primary catalysts or risks discussed here.

However, investors should also be aware that, despite improved quarterly net income, the company’s susceptibility to large-scale catastrophe events remains a key issue to watch...

Read the full narrative on Fidelis Insurance Holdings (it's free!)

Fidelis Insurance Holdings is projected to reach $3.6 billion in revenue and $660.8 million in earnings by 2028. This outlook assumes an annual revenue growth rate of 11.1% and an earnings increase of $705.2 million from the current earnings of -$44.4 million.

Uncover how Fidelis Insurance Holdings' forecasts yield a $20.61 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community estimate Fidelis Insurance Holdings’ fair value anywhere from US$20.61 to US$63.54 per share. While these views vary greatly, many still point to the importance of sustained premium growth amid competitive pricing and sector risks, reminding you to explore a range of perspectives before making your own judgment.

Explore 3 other fair value estimates on Fidelis Insurance Holdings - why the stock might be worth over 3x more than the current price!

Build Your Own Fidelis Insurance Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Fidelis Insurance Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Fidelis Insurance Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fidelis Insurance Holdings' overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FIHL

Fidelis Insurance Holdings

Provides insurance and reinsurance solutions in Bermuda, the Republic of Ireland, and the United Kingdom.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative