Advertisement

- United States

- /

- Insurance

- /

- NYSE:ALL

Is It Too Late to Consider Allstate After a 12% Surge and Digital Upgrades?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Allstate is still a good deal or if the stock has run ahead of itself? Let’s break down what’s going on so you can cut through the noise and make a clear, informed decision.

- After a solid 12.1% jump over the last month and an 11.0% gain so far this year, Allstate’s price momentum has caught the eye of both new investors and longstanding shareholders.

- Recent headlines have highlighted a mix of analyst upgrades and news about Allstate strengthening its digital insurance offerings. These developments have sparked lively debates about the potential for future growth and the company’s ability to adapt in a rapidly evolving insurance market.

- Allstate currently clocks a valuation score of 4 out of 6, which suggests it is undervalued in several key areas. There is more to the story than just numbers. Let’s dive deeper into the major valuation methods, then explore an even better way to figure out if Allstate really is a bargain.

Approach 1: Allstate Excess Returns Analysis

The Excess Returns valuation model helps investors evaluate a company's profitability by comparing how much profit is made in excess of its cost of equity. This is based on the capital invested by shareholders and provides insight into whether Allstate is generating strong returns on its equity and how sustainable those returns appear over time.

For Allstate, the numbers stand out. The book value is $97.34 per share, and the model estimates a stable earnings per share of $29.14, based on the weighted consensus of 12 analysts. With the cost of equity calculated at $8.51 per share, the resulting excess return is an impressive $20.63 per share. The company’s average return on equity sits at a robust 23.82%, indicating efficient profit generation from every dollar of shareholder investment. Projections for the stable book value rise to $122.33 per share, according to estimates from 11 analysts.

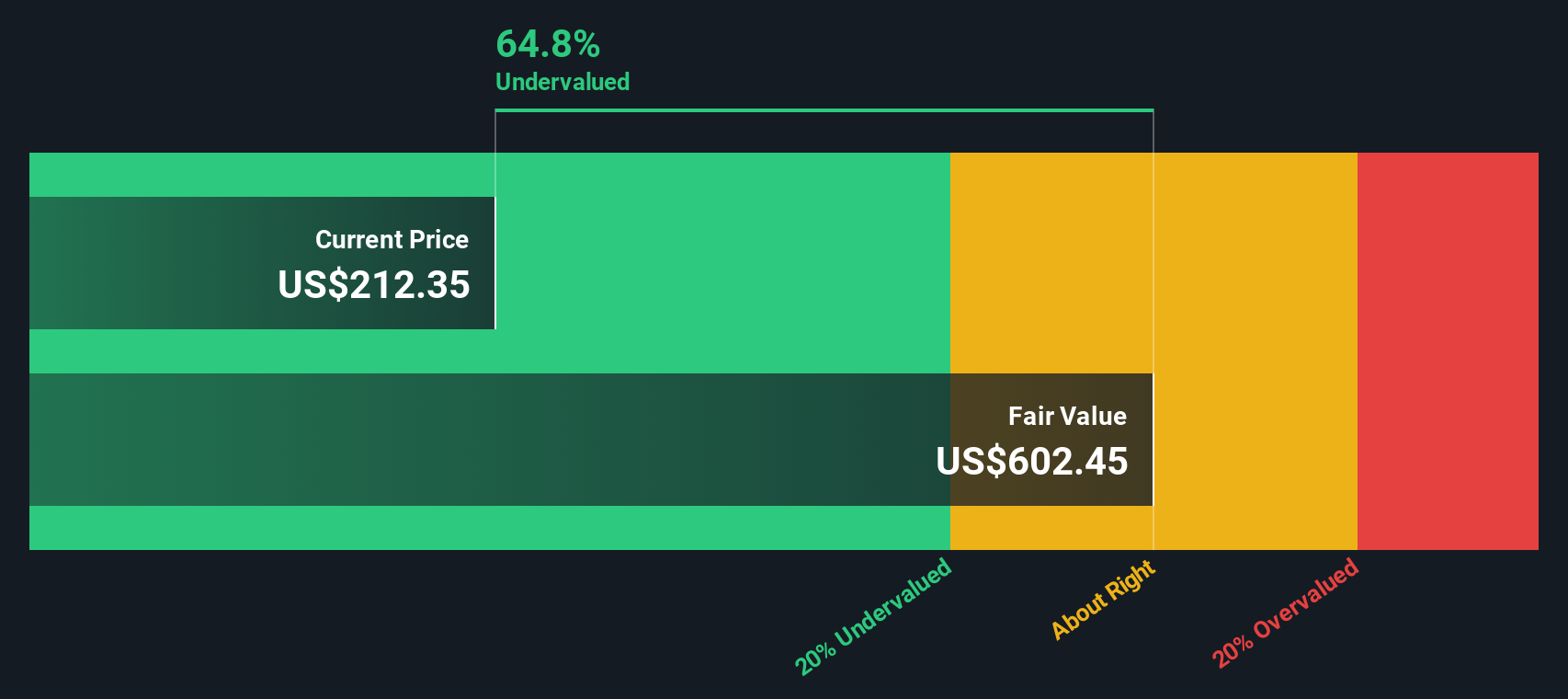

Based on these excess returns, the model estimates Allstate is trading at a 68.7% discount to its true intrinsic value. This suggests the stock is significantly undervalued at its current market price.

Result: UNDERVALUED

Our Excess Returns analysis suggests Allstate is undervalued by 68.7%. Track this in your watchlist or portfolio, or discover 919 more undervalued stocks based on cash flows.

Approach 2: Allstate Price vs Earnings

The price-to-earnings (PE) ratio is a popular and practical valuation metric for profitable companies like Allstate. This multiple relates a stock’s price to its earnings per share, making it especially useful for investors trying to gauge market expectations for future growth and profitability. Generally, a lower PE can signal an undervalued stock, while a higher one might indicate high growth expectations or elevated risks.

Determining what counts as a “fair” PE ratio involves a blend of factors including anticipated earnings growth, the stability of earnings, and the overall risk profile of the business. Companies with faster forthcoming growth or less risk tend to justify higher PE ratios, while slower-growing or riskier firms deserve lower ones.

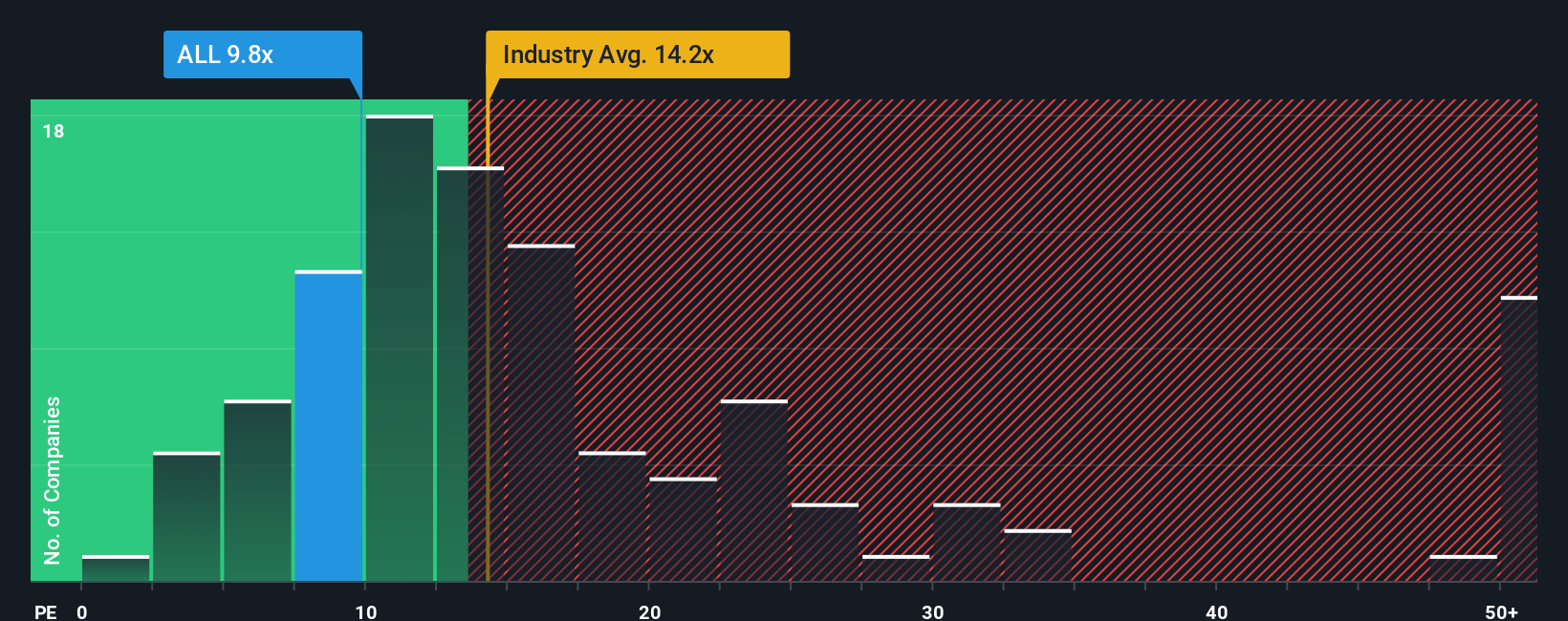

Allstate’s current PE stands at 6.75x, which is notably lower than both the insurance industry average of 13.18x and its peer group average of 13.01x. This on its own might suggest the stock is trading at a discount. However, Simply Wall St’s proprietary Fair Ratio tool offers a deeper look. Its fair PE ratio for Allstate comes in at 6.73x. Unlike basic peer or industry comparisons, the Fair Ratio specifically accounts for critical details like Allstate’s growth prospects, profit margins, factored-in risks, and market cap, giving investors a much more tailored and insightful valuation.

With Allstate’s actual PE almost identical to the Fair Ratio, the stock appears appropriately valued when all fundamentals are considered.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Allstate Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives, a tool that goes beyond statistics by letting you shape your own story or perspective about Allstate's future and see how it impacts the company's upside.

A Narrative is more than just a set of numbers; it is a clear, intuitive way to connect your outlook, from forecasts of revenue growth and margins to expected fair value, with the company's actual story and business realities. Narratives simplify investment decisions by guiding you to compare fair value, based on your assumptions, to the current market price. This can help you decide when to buy or sell with greater confidence.

Narratives are available on Simply Wall St's Community page, used by millions of investors, and they update automatically as new information, such as earnings or company news, emerges. This means your view stays relevant even as the market changes.

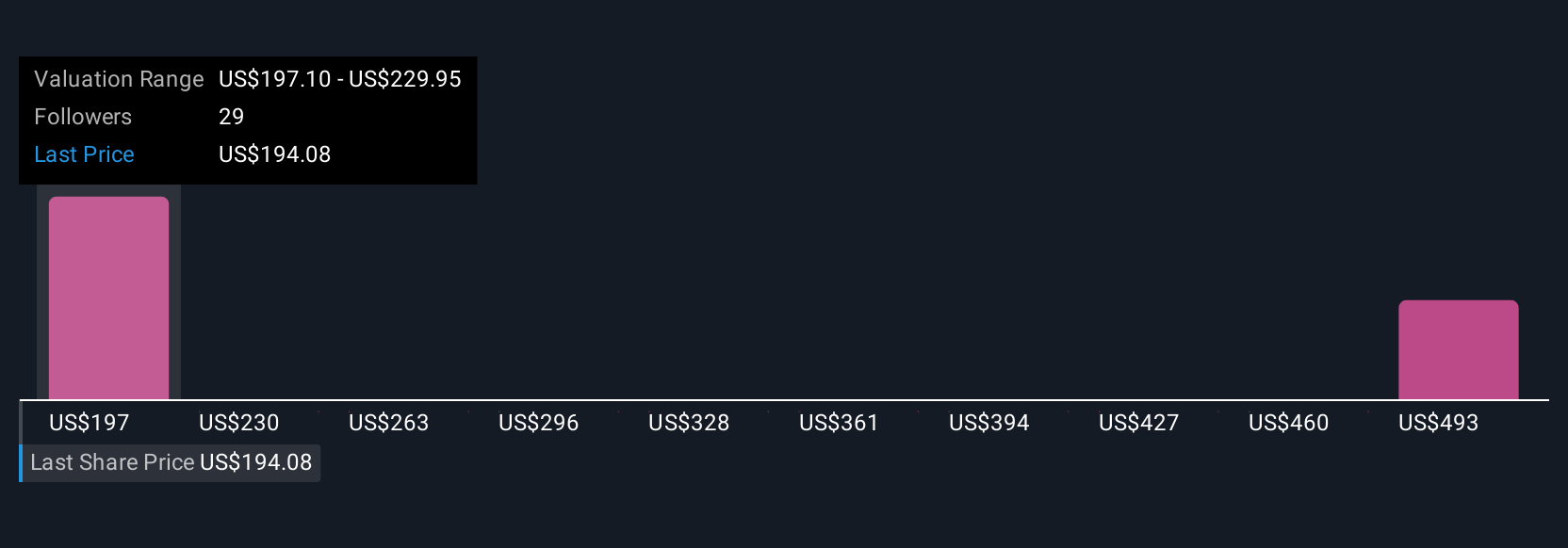

For example, with Allstate, some investors see strong gains ahead, estimating fair value at $275 per share based on tech-driven growth and share buybacks. Others, more cautious about industry risks, believe $157 per share is more realistic. Narratives make it easy to explore these different viewpoints, so you can invest with clarity and conviction.

Do you think there's more to the story for Allstate? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ALL

Allstate

Provides property and casualty, and other insurance products in the United States and Canada.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative