Advertisement

- United States

- /

- Household Products

- /

- NasdaqGS:CENT

Central Garden & Pet (CENT): Net Margin Jumps to 5.2%, Reinforcing Profitability Narrative

Simply Wall St

Reviewed by Simply Wall St

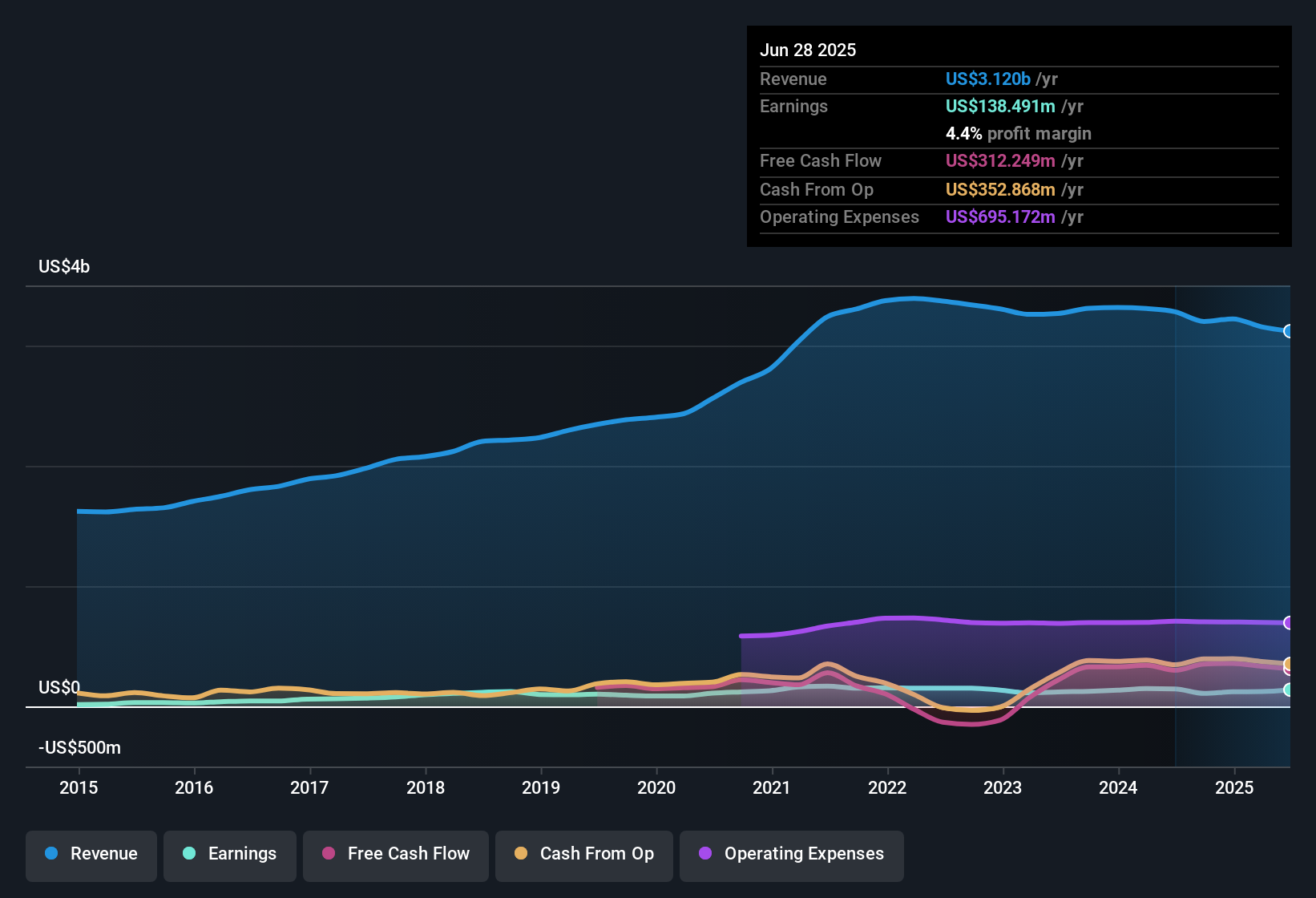

Central Garden & Pet (CENT) just released its FY 2025 Q4 results, reporting revenue of $678 million and a basic EPS of -$0.16. Over the last year, the company has seen revenue change from $3.2 billion to $3.1 billion, while basic EPS moved up from $1.64 to $2.58. Margins have ticked higher, setting the tone for how investors interpret the latest release.

See our full analysis for Central Garden & Pet.Now, let's see how these results stack up against the narratives driving Central Garden & Pet’s story in the market. Some views are likely to be reinforced, while others may face a reality check.

See what the community is saying about Central Garden & Pet

Net Margin Gains Outpace Past Years

- Net profit margin climbed to 5.2% over the last twelve months, compared to 3.4% a year earlier. This reflects a substantial improvement in bottom-line performance alongside $3.1 billion in annual revenue.

- Consensus narrative emphasizes that operational streamlining and a focus on premium, sustainable pet and garden products are driving these margin gains and more resilient earnings.

- Margin improvement supports analysts' view that strategic cost actions and direct-to-consumer investments are working as intended.

- However, the slower forecasted annual revenue growth of 2.9%, well below the US market’s projected 10.5%, presents a notable tension with the positive margin trend.

Valuation Discount Remains Unchanged

- The current share price of $34.16 is 19% below the consensus analyst price target of $42.33, while the company's Price-to-Earnings ratio is 13.1x compared to the global household products industry average of 17.5x.

- Consensus narrative notes that this discounted valuation, paired with improved profit margins, makes the stock appear attractively valued on a relative basis despite restrained growth prospects.

- Analysts point to the 23.9% upside from the current price as an opportunity, provided growth levels meet projections.

- Tension arises as the future PE ratio implied by 2028 earnings estimates (13.7x) is projected to be lower than the sector PE, prompting investors to balance value against growth risks.

Sustainable Growth or Plateau?

- Earnings rose by 50.2% in the last year, sharply outpacing the company’s own five-year trend. However, both revenue and earnings are projected to grow more slowly than the overall US market at 2.9% and 7.91% annually, respectively.

- The consensus narrative highlights how initiatives such as new DTC facilities, product innovation in premium and eco-friendly categories, and strategic SKU rationalization are expected to support durable growth and margin stability.

- Investors are encouraged by these catalysts, but analysts caution that execution risks, along with heavy reliance on core US categories and weather patterns, could limit upside if incremental growth does not offset industry-wide challenges.

- Revenue guidance and declining share count will need to deliver as forecasted to justify analyst expectations for higher earnings by 2028.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Central Garden & Pet on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Does your take on the results differ from the consensus? Put your viewpoint into action by crafting your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Central Garden & Pet.

See What Else Is Out There

Despite stronger margins, Central Garden & Pet faces slower revenue and earnings growth projections than the broader US market, which suggests limited expansion ahead.

If steady, market-beating growth is your priority, use our stable growth stocks screener (2075 results) to quickly find companies that consistently deliver reliable revenue and earnings gains year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CENT

Central Garden & Pet

Produces and distributes various products for the lawn and garden, and pet supplies markets in the United States.

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative