Advertisement

- United States

- /

- Healthtech

- /

- NYSE:VEEV

Veeva Systems (VEEV): Evaluating Valuation After Strong Q3 Growth and Expanded Roche Partnership

Simply Wall St

Reviewed by Simply Wall St

Veeva Systems (VEEV) just posted its third quarter results, recording healthy jumps in revenue and net income compared to last year. In addition, the company expanded its relationship with Roche Pharmaceuticals, which selected Veeva Vault CRM for its commercial activities.

See our latest analysis for Veeva Systems.

The recent boost from strong earnings and the expanded partnership with Roche initially sparked optimism for Veeva Systems, but the company’s share price return has faced pressure, dropping 18.6% over the last month and 11.6% across the past 90 days. Still, the longer-term story is more resilient, with a total shareholder return of 6.1% for the year and 26.4% for investors holding over three years, reflecting both the growth potential and shifts in investor sentiment.

If the momentum around pharma technology has you curious about similar opportunities, now is the perfect time to discover See the full list for free.

With shares recently under pressure despite Veeva’s strong fundamentals and expanding customer relationships, the key question is whether investors are being offered a compelling entry point or if the market has already accounted for future growth.

Most Popular Narrative: 24.9% Undervalued

The narrative consensus fair value for Veeva Systems is well above its last close price, signaling a potential disconnect between analyst expectations and market sentiment. This provides key insight into the narrative’s main drivers.

The resolution of the long-standing dispute with IQVIA removes critical data interoperability barriers. This enables Veeva to fully integrate industry-leading datasets into its Commercial Cloud, which should materially expand its addressable market, improve product adoption across multiple commercial applications, and accelerate top-line revenue growth over the next several years.

Want to know why analysts see so much upside here? The explanation involves ambitious growth assumptions, significant profit margin projections, and a future multiple typically reserved for industry leaders. The full narrative explores the numeric story that could alter the market’s perspective overnight.

Result: Fair Value of $320.62 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing customer resistance to new platforms and heightened competition from established tech giants could quickly challenge Veeva's projected growth trajectory.

Find out about the key risks to this Veeva Systems narrative.

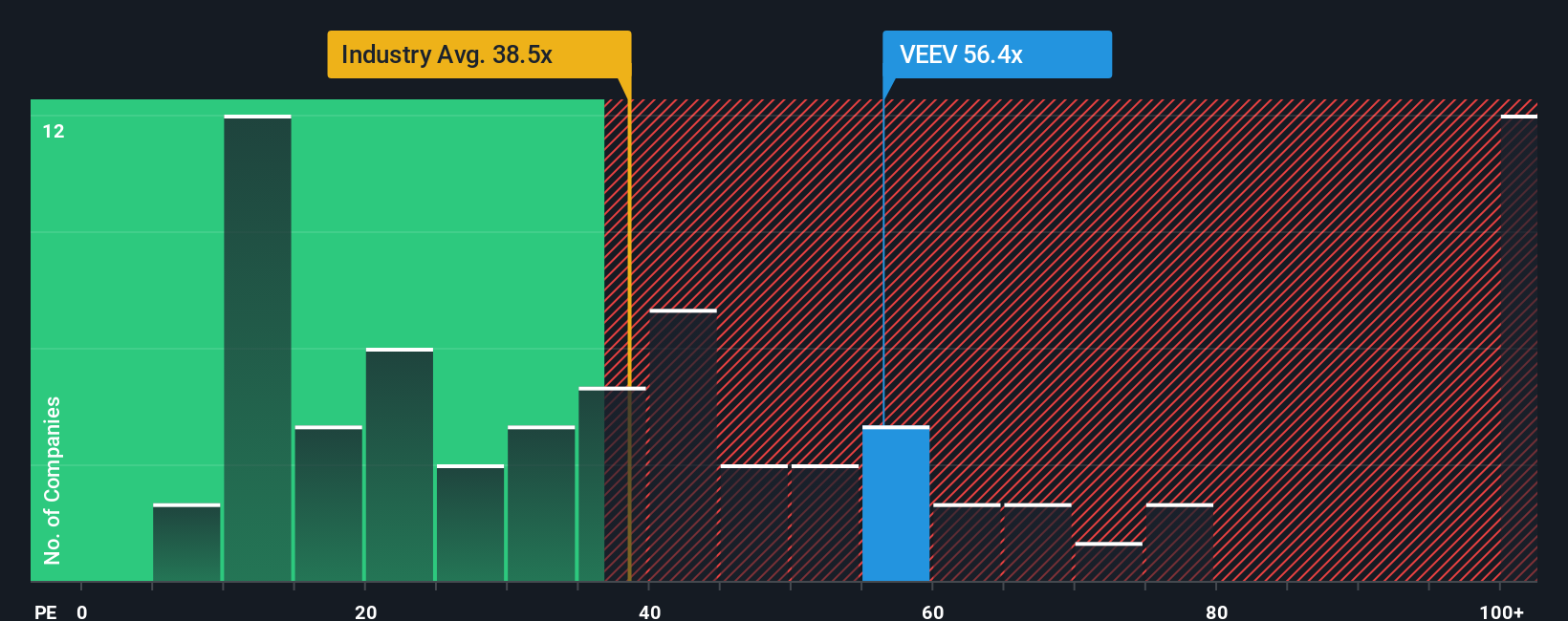

Another View: Multiples Raise Valuation Questions

While analysts see upside based on earnings and growth projections, the current price-to-earnings ratio of 46x puts Veeva well above the industry average of 35.9x and the fair ratio of 32.3x. Compared to peer companies, Veeva actually looks cheaper. However, when measured against the wider market, this gap could signal a risk that valuations may revert lower.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Veeva Systems Narrative

If you have your own perspective or want to dive deeper into the numbers yourself, you can easily craft your narrative and gain new insights in just a few minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Veeva Systems.

Looking for more investment ideas?

Smart investors don’t stand still. Broaden your portfolio and seize fresh opportunities with our top screeners on Simply Wall Street. These strategies could mean the difference between a good year and a great one.

- Uncover high-yield potential by tapping into these 15 dividend stocks with yields > 3% with proven track records of delivering strong income, even in uncertain markets.

- Target undervalued gems and strengthen your returns by seeking out these 927 undervalued stocks based on cash flows poised for a rebound based on solid fundamentals.

- Be part of the AI surge and maximize your exposure by focusing on these 25 AI penny stocks making moves in artificial intelligence and automation right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VEEV

Veeva Systems

Provides cloud-based software for the life sciences industry in North America, Europe, the Asia Pacific, the Middle East, Africa, and Latin America.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative