Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:DGX

How a Narrowed 2024 Outlook and Margin Pressures Will Impact Quest Diagnostics (DGX) Investors

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Quest Diagnostics reported solid third-quarter earnings but narrowed its full-year revenue outlook, reflecting shifting expectations for near-term performance.

- Despite revising 2025 revenue forecasts upward, ongoing concerns over profit margin contraction and increasing debt levels highlight financial headwinds for the company.

- With a tighter revenue outlook tempering optimism, we’ll explore how these recent developments could influence Quest Diagnostics' overall investment case.

Find companies with promising cash flow potential yet trading below their fair value.

Quest Diagnostics Investment Narrative Recap

Holding Quest Diagnostics stock means believing in the long-term durability of diagnostic testing demand and the company's ability to navigate changes in healthcare policy and payer dynamics. The latest quarterly results and narrowed revenue outlook do not materially shift the near-term catalyst, which remains ongoing expansion in advanced testing services, though the biggest risk of prolonged profit margin pressure from rising costs and increased debt is now in sharper focus.

Among Quest's recent announcements, its October 2025 guidance update, raising expected full-year revenues while lowering earnings per share, best encapsulates the current tension between higher top-line potential and the headwinds impacting profitability. This revision underscores why margin trends and operational efficiency remain central to investors watching for sustainable earnings growth.

By contrast, even with these topline gains, investors need to be aware of ongoing concerns about Quest’s rising debt load and margin contraction, especially if...

Read the full narrative on Quest Diagnostics (it's free!)

Quest Diagnostics' narrative projects $11.9 billion revenue and $1.3 billion earnings by 2028. This requires 4.1% yearly revenue growth and a $355 million earnings increase from $945 million today.

Uncover how Quest Diagnostics' forecasts yield a $197.31 fair value, a 4% upside to its current price.

Exploring Other Perspectives

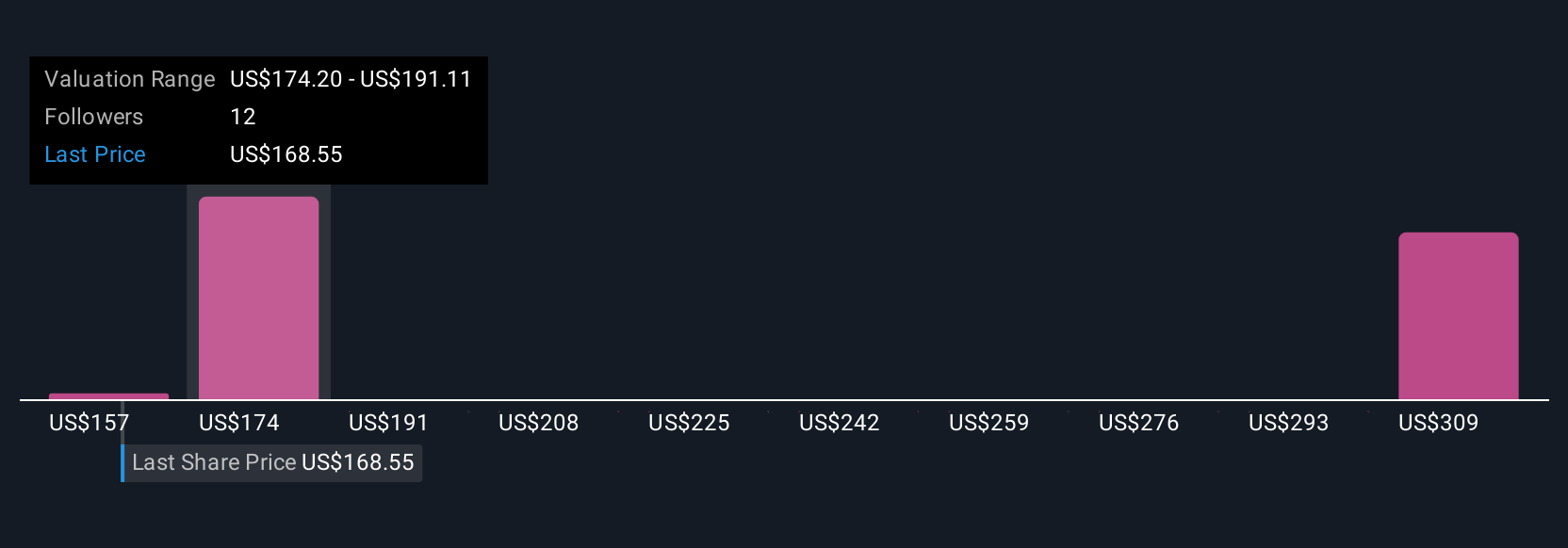

Three members of the Simply Wall St Community estimated Quest Diagnostics' fair value between US$157.30 and US$224.73. While optimism about expanding advanced testing supports the high end, margin headwinds could prove challenging for long-term returns, so exploring more viewpoints is critical.

Explore 3 other fair value estimates on Quest Diagnostics - why the stock might be worth as much as 19% more than the current price!

Build Your Own Quest Diagnostics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Quest Diagnostics research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Quest Diagnostics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Quest Diagnostics' overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Quest Diagnostics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DGX

Quest Diagnostics

Provides diagnostic testing and services in the United States and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative