Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:BDX

Becton Dickinson (BDX): Evaluating Valuation After European Launch of Surgiphor and Recent Strategic Moves

Simply Wall St

Reviewed by Simply Wall St

Becton Dickinson (BDX) unveiled its BD Surgiphor Surgical Wound Irrigation System across select European countries following CE approval for the product. This marks a notable addition to its infection control and surgical offerings.

See our latest analysis for Becton Dickinson.

The Surgiphor launch is not happening in isolation. BD has also been investing in growth drivers such as the recent acquisition of Edwards Lifesciences’ Critical Care group and a board refresh, signaling a focus on innovation and strategic execution. While the share price has climbed nearly 7% in the past month, Becton Dickinson’s one-year total shareholder return of -11% reflects lingering volatility and tempered market optimism, even as momentum has built recently.

If you’re interested in discovering what other healthcare innovators are up to right now, you can see the full list for free with our dedicated screener: See the full list for free.

With recent innovations and strategic acquisitions strengthening BD’s position, the key question for investors now is whether the current valuation reflects the company’s longer-term growth prospects or if an attractive entry point still exists.

Most Popular Narrative: 3.7% Undervalued

Compared to Becton Dickinson’s last close of $194.02, the most widely followed narrative sees fair value at $201.49. This narrow gap sets the scene for a debate on whether recent innovation and business changes can unlock more upside in the share price.

The pending separation of the Biosciences and Diagnostic Solutions business will transform BD into a pure-play medical technology leader with a consumables-heavy portfolio (more than 90% of revenue), enabling higher cash flow predictability and margin improvement. In addition, anticipated aggressive share buybacks directly support EPS growth.

Curious how breaking apart the business could change everything? The most popular narrative features surprisingly ambitious assumptions around margins and future buybacks that drive its fair value. Discover which bold numbers might change your outlook.

Result: Fair Value of $201.49 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing trade tensions and looming execution risks from the business separation could quickly upend analyst expectations. This may make forecasts less certain.

Find out about the key risks to this Becton Dickinson narrative.

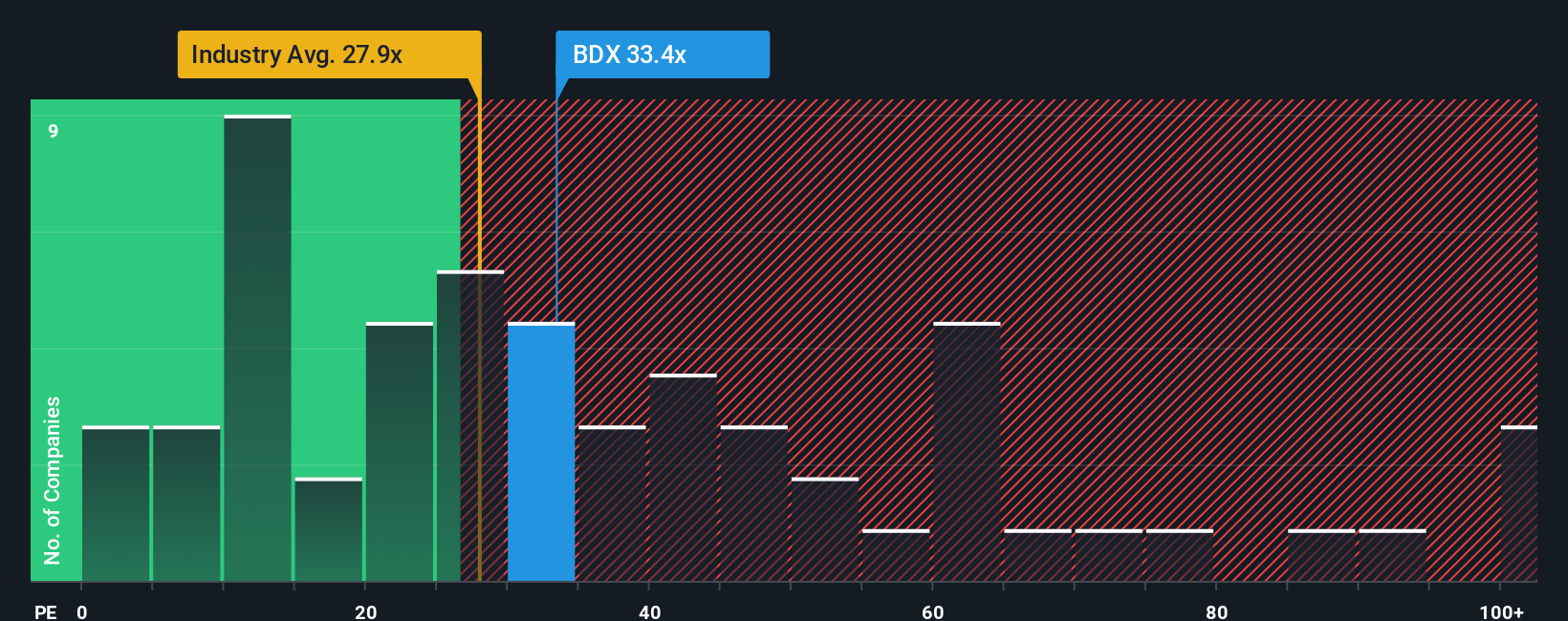

Another View: Market Comparisons Suggest a Premium

While some models suggest Becton Dickinson may be undervalued, its current price-to-earnings ratio of 33x is above the US Medical Equipment sector average of 28.9x, and just over the fair ratio of 32.4x. This premium indicates that investors see extra value or are taking on more risk. So, does the market know something others do not?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Becton Dickinson Narrative

If you see things differently or want to take a deeper dive into the numbers yourself, you can easily craft your own story in just a few minutes with our platform. Do it your way.

A great starting point for your Becton Dickinson research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Opportunities?

Don’t limit yourself to just one company when so many promising trends are shaping tomorrow’s market. Uncover unique investing angles, shake up your strategy, and stay ahead by tracking what’s making a difference today.

- Capture cash-flow potential by checking out these 920 undervalued stocks based on cash flows which contains stocks trading for less than their intrinsic value.

- Tap into the future by exploring these 28 quantum computing stocks as it highlights rapid breakthroughs in quantum tech and computing power.

- Secure steady income with these 15 dividend stocks with yields > 3% that consistently deliver yields above 3% to strengthen your portfolio’s foundation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Becton Dickinson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BDX

Becton Dickinson

Develops, manufactures, and sells medical supplies, devices, laboratory equipment, and diagnostic products for healthcare institutions, physicians, life science researchers, clinical laboratories, pharmaceutical industry, and the general public worldwide.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative