Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:BAX

Does Baxter International’s Restructuring Make Its Recent Share Slump a Long Term Opportunity?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Baxter International at around $18.54 is a bargain or a value trap, you are not alone. That is exactly what this breakdown is going to unpack.

- The stock has slipped 1.1% over the last week but is up 3.0% over the past month, while still sitting on steep losses of 36.6% year to date and 40.6% over the last year. This has many investors questioning whether the risk profile has finally shifted.

- Recent headlines have focused on Baxter reshaping its portfolio and balance sheet, including ongoing steps to streamline its business mix and sharpen its focus on core medical technologies. At the same time, the market has been reassessing large medtech names in light of changing healthcare demand and capital allocation priorities, which helps explain some of the volatility in the share price.

- On our valuation framework, Baxter scores a solid 5 out of 6 on undervaluation checks, suggesting that the market may be overly pessimistic, at least on the numbers. Next we will walk through the main valuation approaches behind that score, and finish with a more holistic way of thinking about what Baxter might really be worth.

Find out why Baxter International's -40.6% return over the last year is lagging behind its peers.

Approach 1: Baxter International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and then discounting them back to a single value today. For Baxter International, this means taking expected Free Cash Flow and translating it into a present day intrinsic value per share.

Baxter generated trailing twelve month Free Cash Flow of about $261 million, and analysts expect this to rise steadily, reaching around $943 million by 2027. Beyond the explicit analyst horizon, Simply Wall St extrapolates those estimates, with projected Free Cash Flow climbing to roughly $1.46 billion by 2035 as growth gradually moderates.

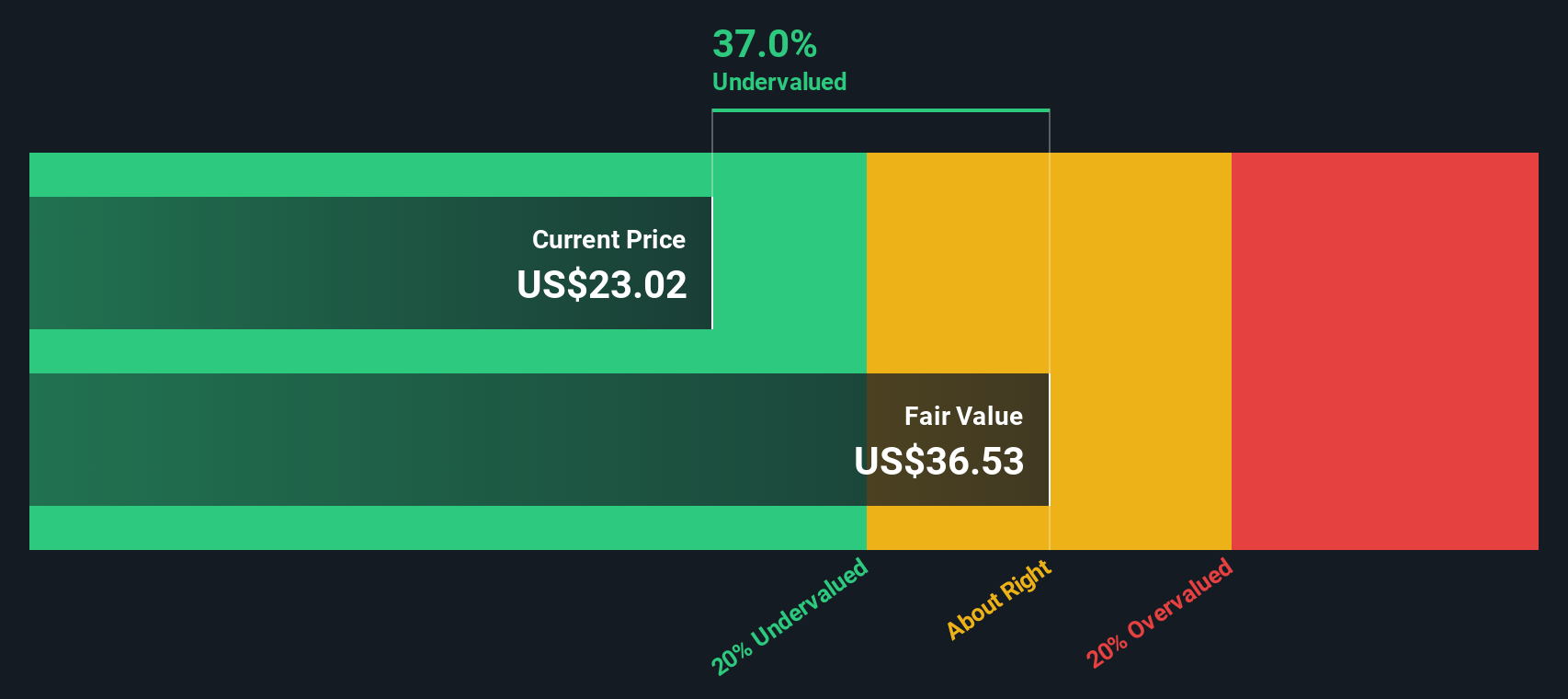

When all those future cash flows are discounted back using a 2 Stage Free Cash Flow to Equity model, the implied intrinsic value comes out at approximately $30.21 per share. Compared with the recent share price around $18.54, the DCF suggests the stock is about 38.6% undervalued, which indicates the market may be heavily discounting Baxter’s ability to convert its medtech portfolio into growing cash flow.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Baxter International is undervalued by 38.6%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

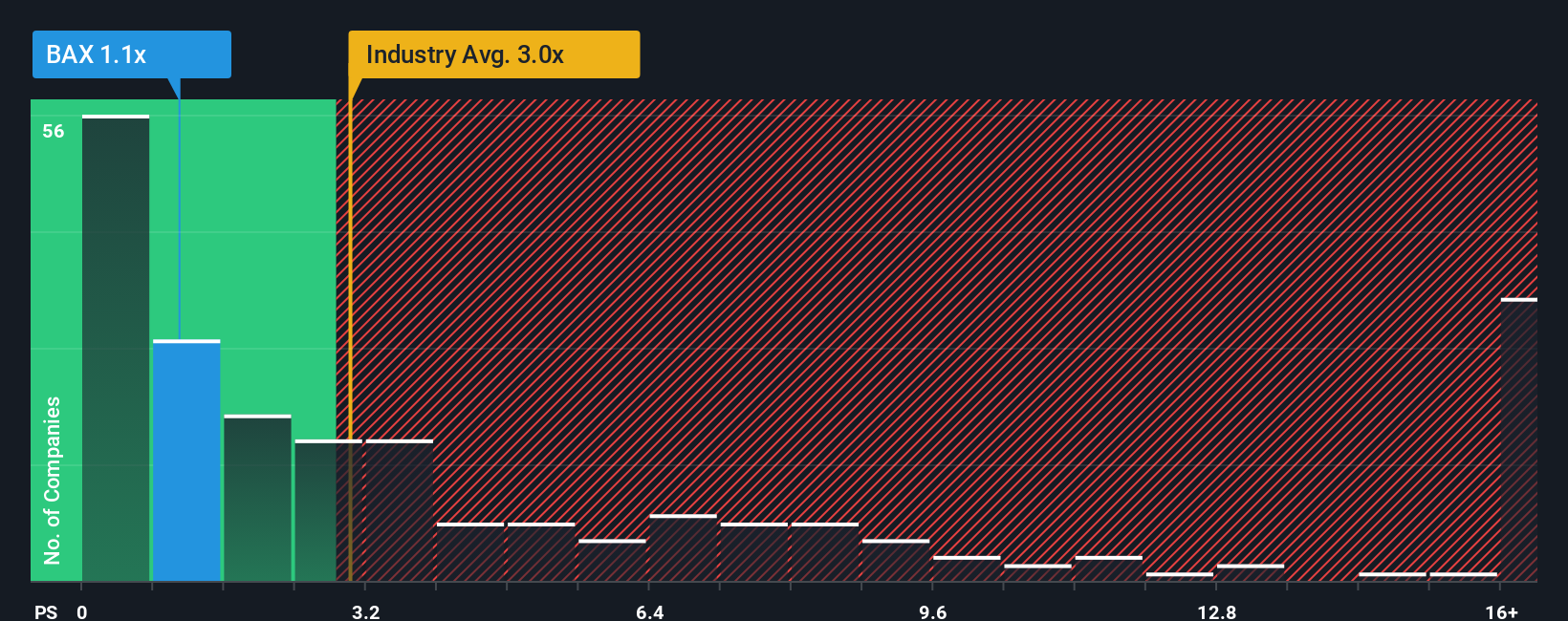

Approach 2: Baxter International Price vs Sales

Price to Sales is a useful yardstick for companies where revenue is a more stable indicator than earnings, which can swing around because of restructuring charges, interest costs, or other one off items. For medtech names like Baxter, investors often look at how much they are paying for each dollar of sales as a quick sense check on valuation.

In general, faster growth and lower risk justify a higher multiple. Slower or more uncertain growth tends to pull a “normal” Price to Sales ratio down. Baxter currently trades on about 0.86x sales, well below the Medical Equipment industry average of roughly 3.37x and also far under the peer group average of about 4.52x. On simple comparison, that gap makes the stock look very cheap.

Simply Wall St’s proprietary Fair Ratio, at 1.33x, adjusts for Baxter’s specific growth outlook, margins, size, industry, and risk profile, making it more tailored than blunt peer or sector comparisons. Because this Fair Ratio builds those fundamentals in, it is presented as a more reliable anchor for what investors might reasonably pay for the stock. With the actual Price to Sales at 0.86x versus a Fair Ratio of 1.33x, Baxter screens as undervalued on this metric.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1452 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Baxter International Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simple, story driven explanations of why you think a company like Baxter International is worth a certain amount, tying your view of its future revenue, earnings and margins to a financial forecast and ultimately to a fair value. On Simply Wall St’s Community page, millions of investors can build and compare these Narratives, using them as an easy, accessible tool to decide whether a fair value estimate sits above or below the current share price, and to track that estimate as it updates automatically when new news, earnings, or guidance comes in. For Baxter, for example, one investor might build a bullish Narrative that assumes strong margin recovery under the new CEO and a fair value closer to the upper analyst target of $47. Another might focus on persistent operational headwinds and quality risks and anchor their Narrative around a more cautious fair value near the low end of $19. Both perspectives are transparently linked back to explicit forecasts and assumptions.

Do you think there's more to the story for Baxter International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baxter International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BAX

Baxter International

Through its subsidiaries, provides a portfolio of healthcare products in the United States.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative