Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGM:TMDX

Is Now the Right Time for TransMedics After a 120% Surge and FDA Approvals?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if TransMedics Group is still a bargain or if the huge price moves have put it out of reach? Let’s break down whether now is the right time to buy in or stay on the sidelines.

- TransMedics stock has soared 120.0% year-to-date and 68.7% over the past year, drawing fresh attention from growth investors and those tracking emerging medical technology trends.

- Much of this renewed interest follows industry headlines about innovations in organ transplant logistics and successful expansion into new markets, with TransMedics frequently in the spotlight. Recent FDA approvals for its organ care systems have also boosted optimism and shifted market perception.

- Right now, TransMedics scores a 2 out of 6 on our valuation check, suggesting the story goes deeper than just the share price. Let’s explore the standard ways analysts value stocks like this, before revealing why there might be an even smarter approach at the end of this article.

TransMedics Group scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: TransMedics Group Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the value of a company by projecting its future cash flows and then discounting them back to today's dollars. This approach helps investors gauge what the business is fundamentally worth, independent of current market sentiment.

For TransMedics Group, analysts estimate the company generated Free Cash Flow of $17.7 million in the last twelve months. Forecasts anticipate rapid growth, with Free Cash Flow expected to climb to $233.6 million by 2028. Since analysts only project out five years with concrete numbers, subsequent years are extrapolated based on historical and industry patterns. Looking out ten years from now, annual Free Cash Flow could reach over $559 million according to these models.

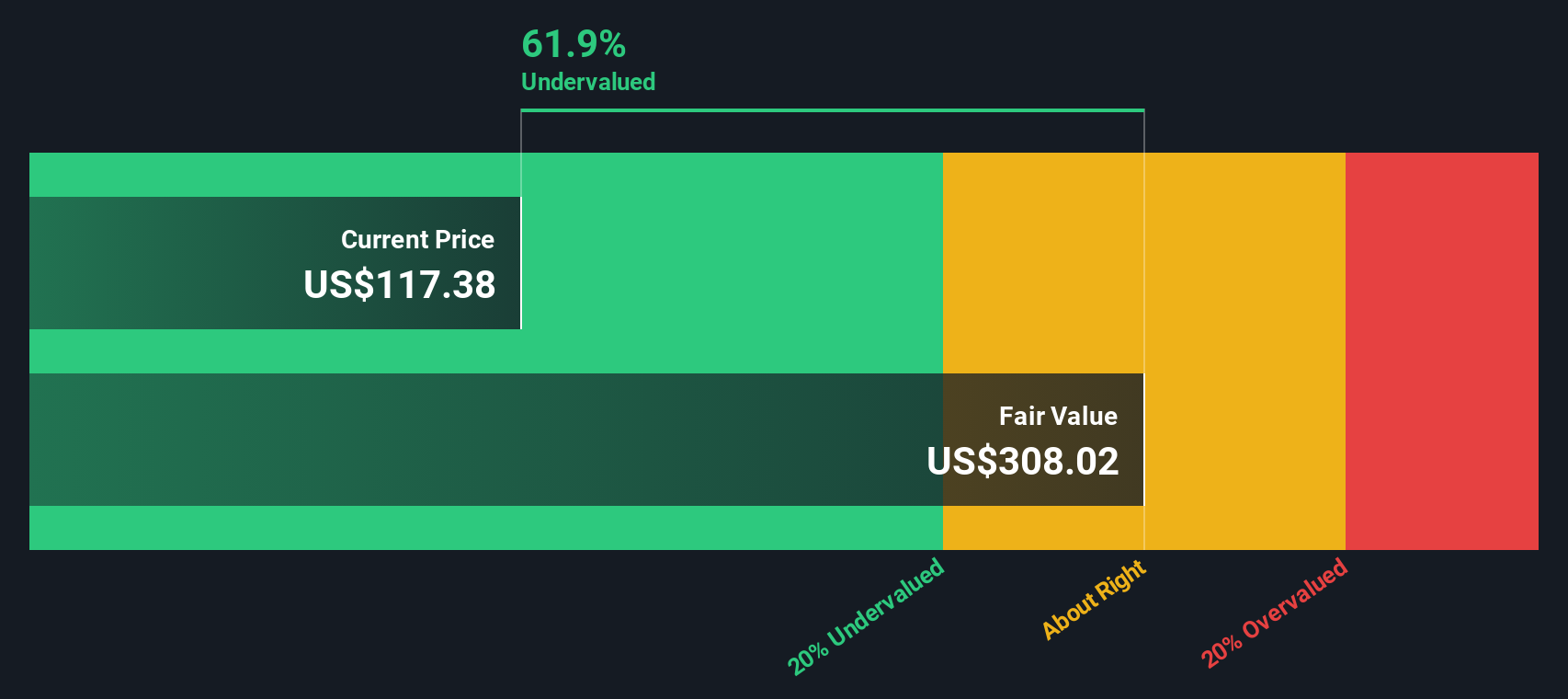

Using this two-stage DCF approach, the estimated intrinsic value per share is $231.89. Compared to the current share price, this implies the stock is 36.9% undervalued, indicating a meaningful potential upside for long-term investors.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests TransMedics Group is undervalued by 36.9%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: TransMedics Group Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a time-tested valuation metric, especially meaningful for profitable companies like TransMedics Group. It helps investors quickly assess how much they are paying for each dollar of earnings, providing a practical benchmark for comparing stocks across the same industry or growth profile.

However, a "fair" PE is not one-size-fits-all. Companies with stronger expected growth, higher profit margins, or lower risk typically deserve a higher PE multiple, while slower-growing or riskier companies deserve lower ones. As a result, the right PE ratio must reflect these underlying differences.

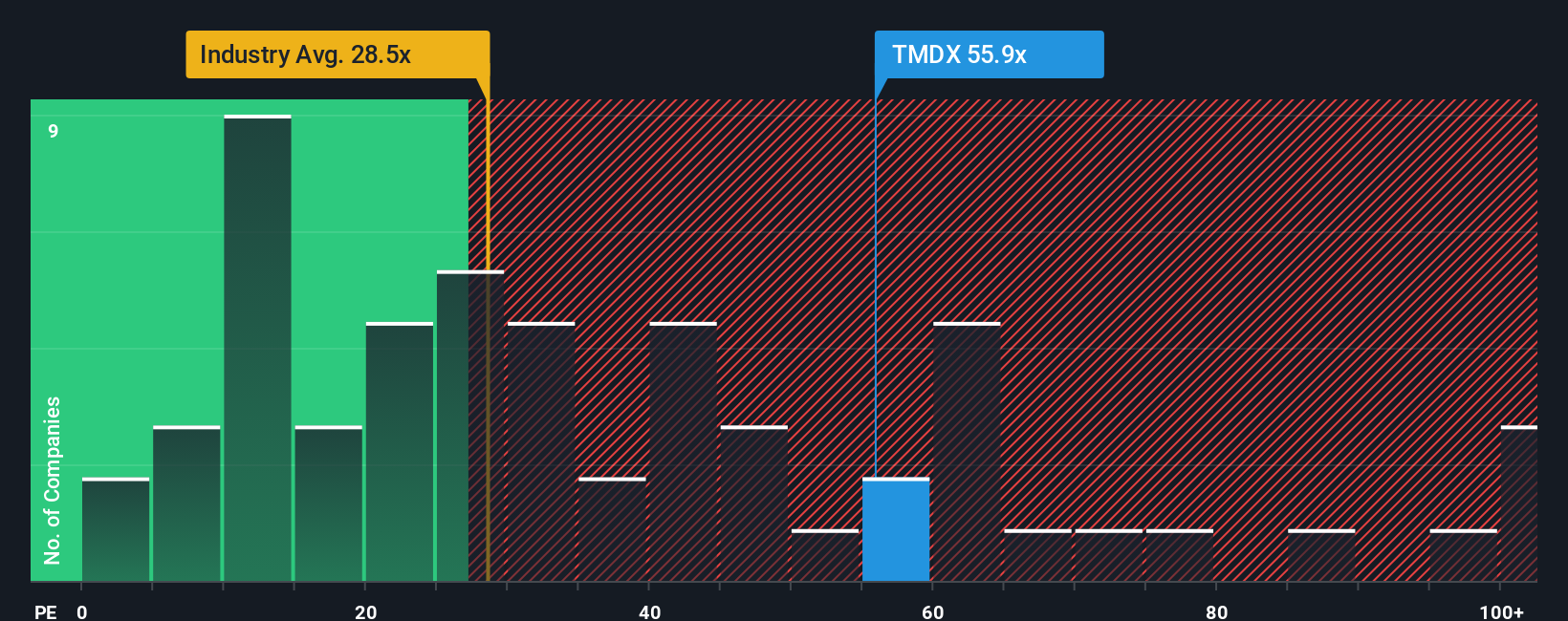

TransMedics Group currently trades at 54.5x earnings, which is well above the medical equipment industry average of 28.9x and also higher than the group of direct peers, who average 43.5x. At first glance, this premium might make the stock seem expensive.

This is where Simply Wall St’s “Fair Ratio” shines. Instead of simply averaging peers or industries, it factors in TransMedics’ unique growth expectations, profit margins, risk profile, industry dynamics, and company size. For TransMedics, the Fair Ratio is 28.1x, which is a clear, data-driven indication of what would be justified for a business with these characteristics.

Since TransMedics’ current PE is much higher than its Fair Ratio, this suggests the stock is currently trading above what would be considered fair based on its fundamentals and prospects.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your TransMedics Group Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives.

Narratives are a simple but powerful approach that lets you explain your perspective on a company by connecting its story, such as business strengths, risks, or industry changes, to your own expectations for future revenue, earnings, and margins.

With Narratives, you go beyond the numbers to build a logical bridge. Start with your understanding of TransMedics Group’s opportunities and challenges, turn those insights into a financial forecast, and instantly see your fair value estimate.

This tool is accessible for everyone on Simply Wall St’s Community page, used by millions of investors, making it easier than ever for you to test your investment thesis and share it with others.

Narratives make decisions clearer by dynamically comparing your Fair Value to the latest Price and automatically updating when new news or earnings are announced, so you stay ready to act when the story changes.

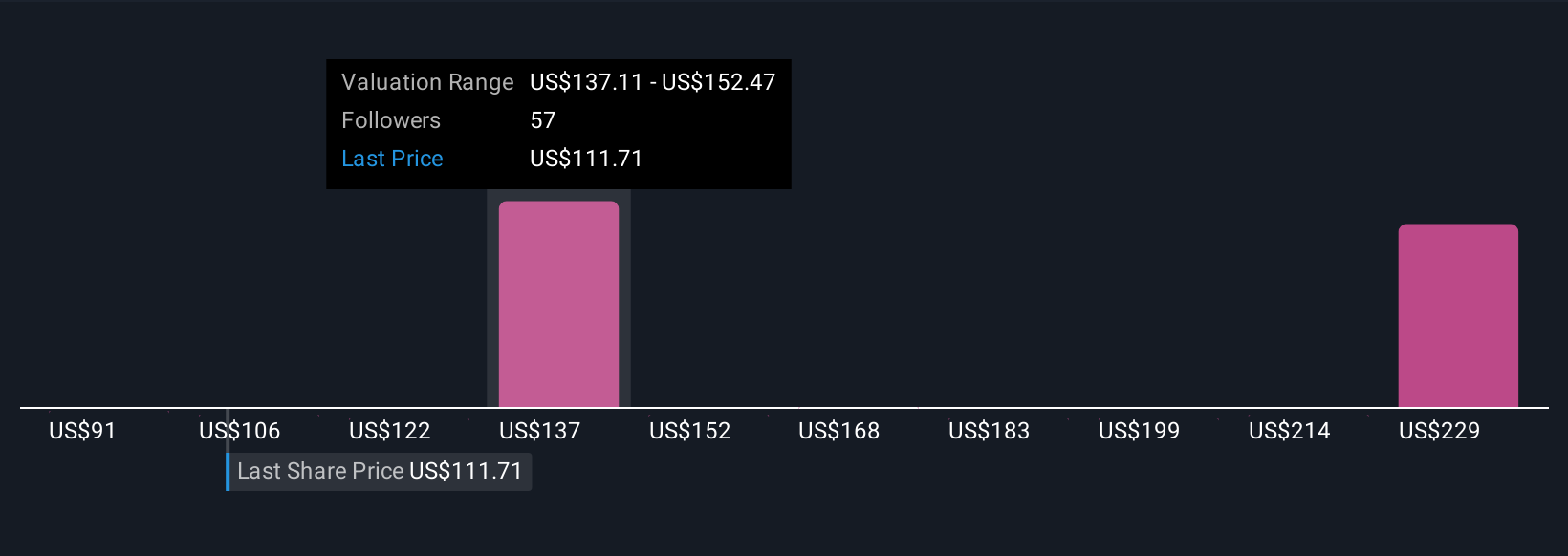

For example, some investors may have a bullish Narrative for TransMedics Group, projecting strong U.S. sales and international expansion that support a fair value of $170 per share. Others are more cautious and see near-term challenges justifying a fair value closer to $114.

Do you think there's more to the story for TransMedics Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TransMedics Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:TMDX

TransMedics Group

A commercial-stage medical technology company, engages in transforming organ transplant therapy for end-stage organ failure patients in the United States and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative