Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGM:LMAT

Is LeMaitre Vascular’s Slide in 2025 a Chance Amid New Product Launches?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if LeMaitre Vascular is actually worth the price you see on your screen? You're not alone as many investors are wondering if now is the time to buy or step back.

- After an impressive rise in recent years, the stock is down 5.7% over the last week and has slipped 21.7% over the past year, though it is still boasting a 131.8% five-year return.

- LeMaitre Vascular has appeared in several headlines recently for major product launches and strategic acquisitions, sparking fresh conversations about its long-term potential. This flurry of activity helps explain both the volatility in its share price and the renewed interest from both growth and value investors.

- On our valuation checks, the company currently scores just 2 out of 6, pointing toward some possible concerns. In the next section, we'll break down what this means using a few popular valuation approaches and wrap up with one insightful shortcut savvy investors should not miss.

LeMaitre Vascular scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: LeMaitre Vascular Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the value of a company by projecting its future cash flows and then discounting those back to today's value. This approach provides an intrinsic value based on what the business is expected to earn moving forward.

For LeMaitre Vascular, the latest reported Free Cash Flow (FCF) is $65.6 million. Analysts have provided FCF estimates for the next several years, with projections reaching $71.3 million by 2029. After the first five years, further cash flow growth is extrapolated using standard industry assumptions, which is typical for long-term forecasts.

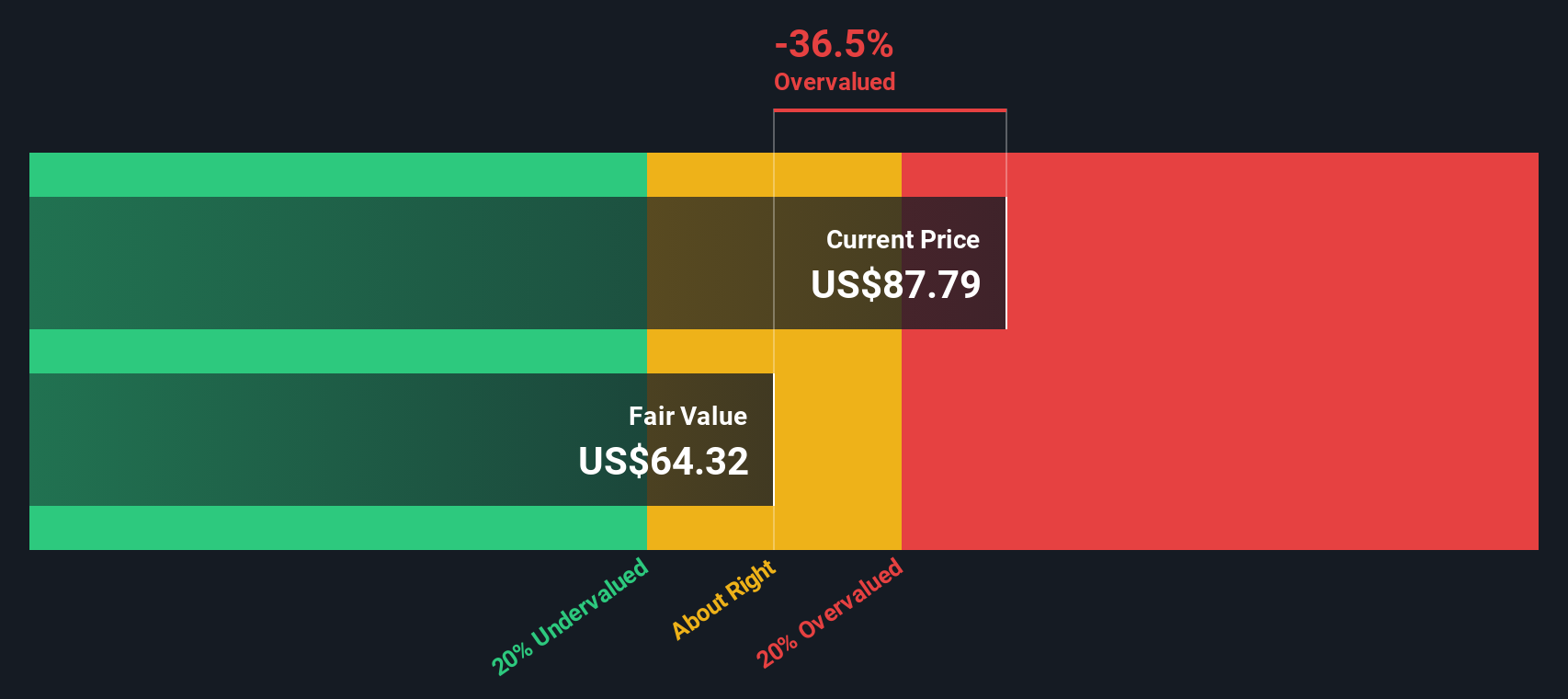

Based on the 2 Stage Free Cash Flow to Equity model, LeMaitre Vascular's intrinsic value per share is calculated at $59.89. However, the current market price indicates the stock is trading at a 38.5% premium compared to this DCF-derived estimate. In other words, the market is pricing in stronger growth or profitability than current cash flow projections suggest.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests LeMaitre Vascular may be overvalued by 38.5%. Discover 921 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: LeMaitre Vascular Price vs Earnings

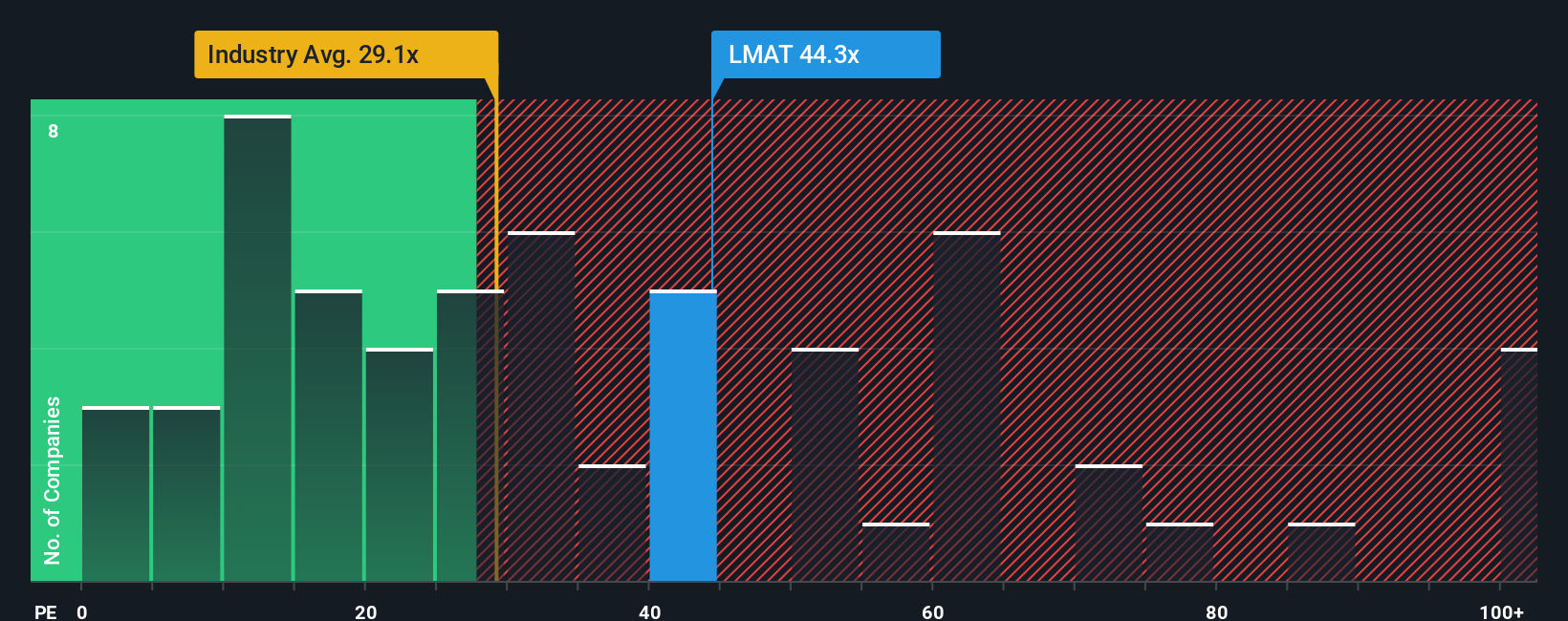

The Price-to-Earnings (PE) ratio is a classic valuation tool, especially for profitable companies like LeMaitre Vascular. Since it reflects how much investors are willing to pay per dollar of earnings, it offers a straightforward way to gauge market expectations. Generally, a higher PE ratio indicates investor optimism about future growth, while a lower ratio may point to either lower growth prospects or higher perceived risks.

Currently, LeMaitre Vascular trades at a PE ratio of 35.3x. To put this in perspective, the Medical Equipment industry average sits at 28.9x, and its peer group averages 46.8x. On its face, LeMaitre’s valuation is higher than the broader industry but not as stretched relative to peers operating in similar niches.

To get a more accurate picture, Simply Wall St calculates a proprietary "Fair Ratio" based on a range of factors like earnings growth rate, sector, profit margins, company size, and risk. For LeMaitre Vascular, the Fair Ratio is estimated at 17.6x. This approach goes beyond basic comparisons, incorporating the company’s specific fundamentals and outlook rather than relying solely on the influences of the group.

With the current PE of 35.3x compared to a Fair Ratio of 17.6x, LeMaitre Vascular appears to be trading at a significant premium. This suggests the stock is likely overvalued on an earnings multiple basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your LeMaitre Vascular Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple but powerful framework where investors connect a company’s story, including its recent news, industry changes, and long-term vision, to a specific financial forecast and a fair value estimate. Unlike traditional valuation models that focus solely on numbers, Narratives allow you to shape your own perspective on LeMaitre Vascular’s future, grounded in your assumptions about future revenues, earnings, and profit margins.

Narratives are available directly on Simply Wall St’s platform within the Community page, making this tool accessible to everyone from beginners to experienced investors. By comparing your Narrative’s fair value with the current share price, you gain a clearer, more personalized view of whether it could be time to buy or sell. The dynamic nature of Narratives means that if there is new news, earnings, or regulatory changes, your Narrative updates in real time. This ensures you are always working with the latest information.

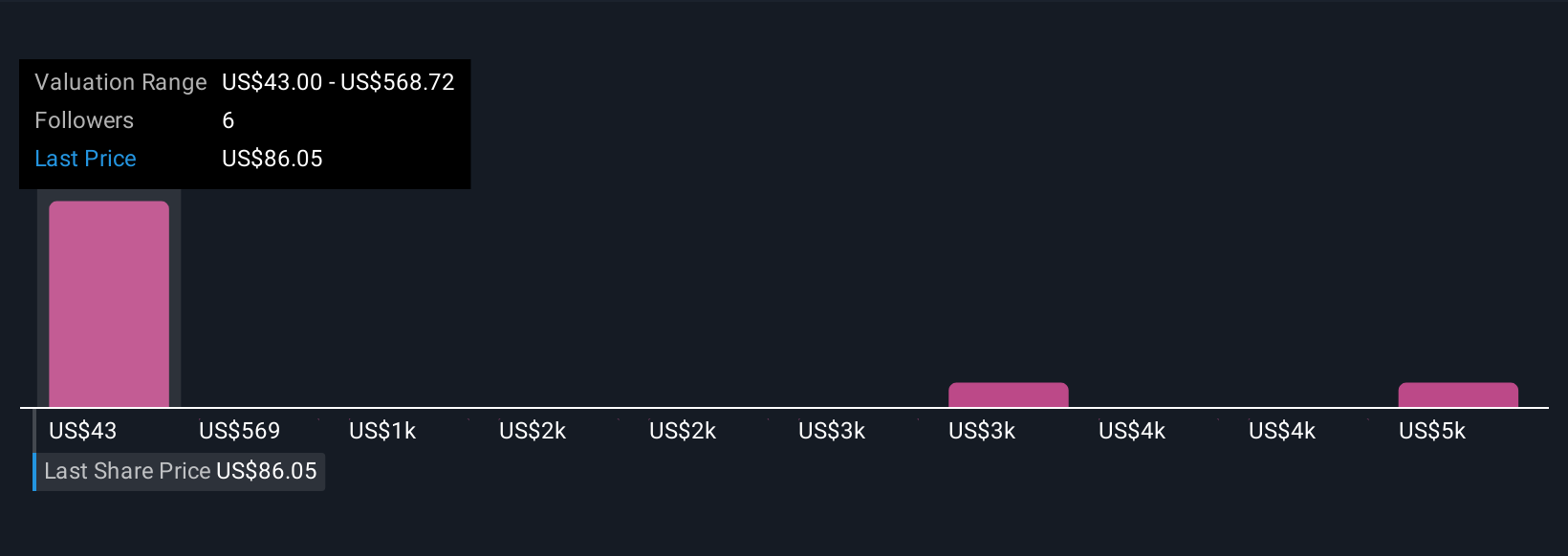

For example, some investors believe aggressive international growth and product innovation will see LeMaitre Vascular reaching the top end of analyst targets at $120 per share, while others take a more cautious view, citing niche risks and pricing pressures, with estimates landing closer to $92.

Do you think there's more to the story for LeMaitre Vascular? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:LMAT

LeMaitre Vascular

Develops, manufactures, and markets medical devices and implants used in the field of vascular surgery in the Americas, Europe, the Middle Esat, Africa, and the Asia Pacific.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative