Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:COO

Cooper Companies (COO) Margin Decline Tests Bullish 21% Earnings Growth Narrative

Simply Wall St

Reviewed by Simply Wall St

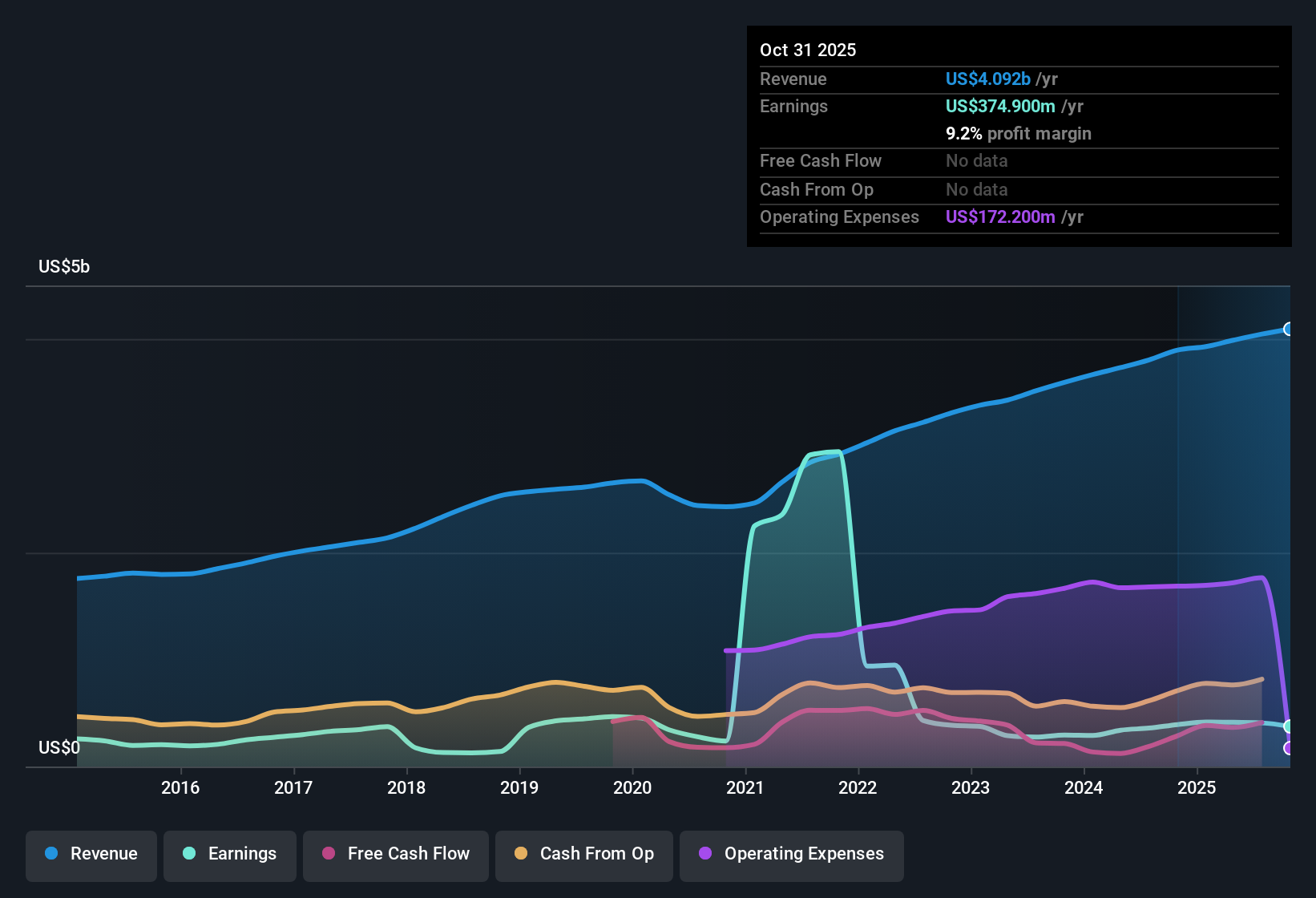

Cooper Companies (COO) just wrapped up FY 2025 with fourth quarter revenue of $1.1 billion and basic EPS of $0.43, capping a trailing twelve month run of $4.1 billion in revenue and $1.87 in EPS that investors will be dissecting closely. The company has seen revenue move from $3.9 billion and EPS of $1.97 over the twelve months to Q4 2024 to $4.1 billion and EPS of $1.87 over the latest twelve month period, setting a nuanced backdrop for how the current year’s performance fits into its longer term earnings and margin story.

See our full analysis for Cooper Companies.With the headline numbers on the table, the next step is to see how this trajectory lines up with the dominant narratives around Cooper Companies, from earnings growth potential to margin sustainability.

See what the community is saying about Cooper Companies

Margins Slip as Net Income Eases Back

- Trailing twelve month net income slipped from $415.4 million in Q1 2025 to $374.9 million by Q4 2025, alongside net margin easing from 10.1% to 9.2% year over year.

- Consensus narrative expects automation and cost discipline to lift margins and free cash flow, which contrasts with the recent margin dip.

- Analysts are modeling profit margins rising to 16.2% over three years even though current trailing margin is 9.2% and down from 10.1%.

- This gap between forecasted margin expansion and the recent $40.5 million drop in trailing net income prompts investors to scrutinize how quickly efficiency gains can flow through.

Earnings Forecasts Race Ahead of 5.2% Revenue Growth

- Earnings are forecast to grow about 21.4% per year while revenue is only expected to grow around 5.2% annually, slower than the US market’s 10.6% pace.

- Consensus narrative leans bullish on new products like MyDAY and MiSight driving growth, yet the current revenue trend remains moderate.

- Quarterly revenue moved from $964.7 million in Q1 2025 to $1.1 billion in Q4 2025 and analysts see revenue reaching about $4.9 billion by 2028.

- Expected earnings of $786.2 million and EPS of $3.95 by roughly 2028 rely on that 21.4% earnings growth materializing even though recent trailing net income is $374.9 million.

As forecasts call for faster profit growth than sales, many bulls are watching closely to see whether MyDAY and other launches can overcome slower industry growth.

🐂 Cooper Companies Bull CaseRich 43.2x P/E Versus Slowing Five Year Earnings

- The stock trades on a 43.2x trailing P/E versus 28.9x for the US Medical Equipment industry and 26.2x for peers, even as five year earnings declined at about 43% per year and net margin slipped to 9.2%.

- Bears highlight that a premium multiple on shrinking historical earnings leaves little room for disappointment, despite a modeled DCF fair value of about $113.04 versus the current $81.40 share price.

- The roughly 28% discount to DCF fair value sits alongside a weaker trailing margin profile and that steep multi year earnings decline.

- With the stock below the allowed analyst target reference of $88.88 yet above what recent earnings trends might justify, skeptics focus on the risk if the 21.4% earnings growth forecast falls short.

For cautious investors, the combination of a 43.2x multiple and a five year earnings slide is a clear reason to test every growth assumption twice.

🐻 Cooper Companies Bear CaseNext Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Cooper Companies on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Spot something in the numbers others might be missing? In just a few minutes, you can shape that view into a full narrative, Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Cooper Companies.

See What Else Is Out There

Cooper Companies’ rich valuation, slipping margins, and slower revenue growth versus earnings forecasts leave little room for missteps or disappointment.

If you want stocks where price better reflects fundamentals and expectations, use our these 906 undervalued stocks based on cash flows today to hunt for candidates with more upside and fewer valuation compromises.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:COO

Cooper Companies

Develops, manufactures, and markets contact lens wearers.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.70.8% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative