Advertisement

- United States

- /

- Food

- /

- NYSE:POST

How Post Holdings’ US$500 Million Buyback and Leadership Changes Are Shaping Its Story (POST)

Simply Wall St

Reviewed by Sasha Jovanovic

- In November 2025, Post Holdings, Inc. announced a new share repurchase program authorizing up to US$500 million in buybacks over the next two years, following the completion of several recent buyback tranches and reporting fourth-quarter and full-year earnings results.

- An additional highlight from the past week includes the retirement of long-standing Chairman William P. Stiritz, with CEO Rob Vitale set to take on the Chairman role, signaling important leadership changes for the company.

- We’ll examine how Post Holdings’ newly authorized US$500 million share repurchase program may influence the company’s investment narrative and future outlook.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

Post Holdings Investment Narrative Recap

To be a shareholder in Post Holdings, investors typically look for steady demand in packaged foods, margin support from cost-saving initiatives, and benefits from product innovation and acquisitions. The recent US$500 million buyback authorization could boost investor sentiment but does not materially change the most important short-term catalyst: stabilizing branded and private label cereal volumes. Ongoing competitive pressures in these core categories remain the most significant risk, with the buyback program having minimal immediate impact on these challenges.

The recent disclosure of a US$29.8 million goodwill impairment charge is especially relevant. This write-down, caused by increased competition and pricing pressure from private label brands, highlights ongoing profitability challenges in key segments, issues that tie directly into concerns about volume declines and the durability of Post’s growth driver categories.

However, investors should also be aware that persistent volume declines in branded cereals could...

Read the full narrative on Post Holdings (it's free!)

Post Holdings' narrative projects $9.2 billion in revenue and $537.3 million in earnings by 2028. This requires 5.2% yearly revenue growth and a $171 million earnings increase from current earnings of $366.3 million.

Uncover how Post Holdings' forecasts yield a $123.22 fair value, a 20% upside to its current price.

Exploring Other Perspectives

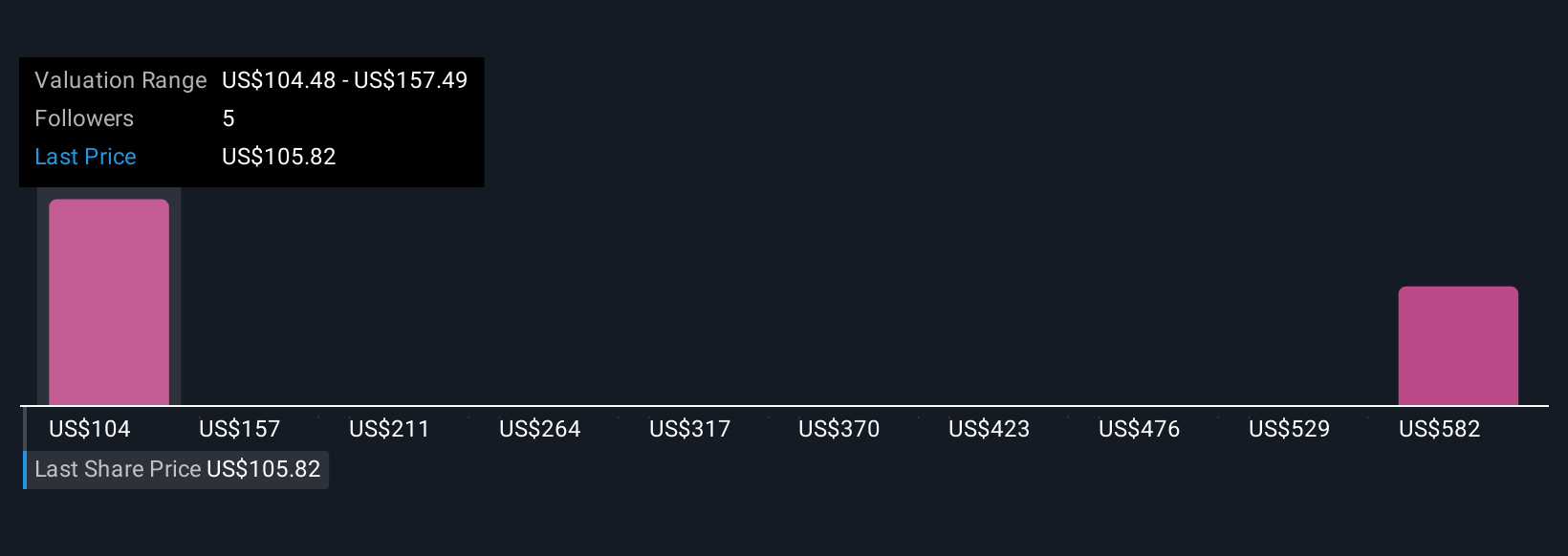

Four recent fair value estimates from the Simply Wall St Community span from US$104.48 to US$628.97, reflecting wide opinion differences. Price competition and profit pressures continue to shape what matters for Post’s long-term performance, so compare these viewpoints to your own research.

Explore 4 other fair value estimates on Post Holdings - why the stock might be worth just $104.48!

Build Your Own Post Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Post Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Post Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Post Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:POST

Post Holdings

Operates as a consumer packaged goods holding company in the United States and internationally.

Undervalued with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative