Beyond Meat (BYND) shares have faced steep declines in recent months, reflecting shifts in market sentiment for plant-based meat alternatives. Despite its well-known brand and global reach, investor interest appears muted as the company navigates ongoing challenges.

This year’s steep slide comes after a string of tough quarters and shifting consumer appetites for plant-based meat. While Beyond Meat enjoyed a 13.85% 7-day share price bounce, the 30-day share price return of -46.79% and a staggering -80.29% total return over the past year highlight how far momentum has faded, both in the near term and over a longer period.

But with Beyond Meat’s struggles now well documented, the key question is whether the recent share price collapse means the stock is undervalued and due for a rebound, or if the market has already priced in its challenges and future prospects.

Advertisement

Most Popular Narrative: 39% Undervalued

With Beyond Meat's last close at $0.98 and a most-followed narrative fair value of $1.61, analysts see significant upside if the company can execute on transformation initiatives. However, this optimism is anchored on the idea that cost reductions and new retail strategies might spark a recovery in margins and revenue.

Beyond Meat is accelerating operational efficiency efforts, including substantial cost reduction, portfolio optimization, and manufacturing investments. These actions are expected to improve gross margins and drive the company toward EBITDA-positive operations, which would benefit future net income and operating cash flow.

Want to know what numbers fuel this bullish perspective? Uncover the fundamental drivers, such as margin improvements and a surprising future profit multiple, that could transform Beyond Meat’s narrative. The assumptions behind this price target might surprise even seasoned investors. Unlock the rationale powering this valuation.

However, persistent weak demand for plant-based meats and ongoing questions about sustainable profitability could quickly challenge the optimism behind Beyond Meat’s recovery narrative.

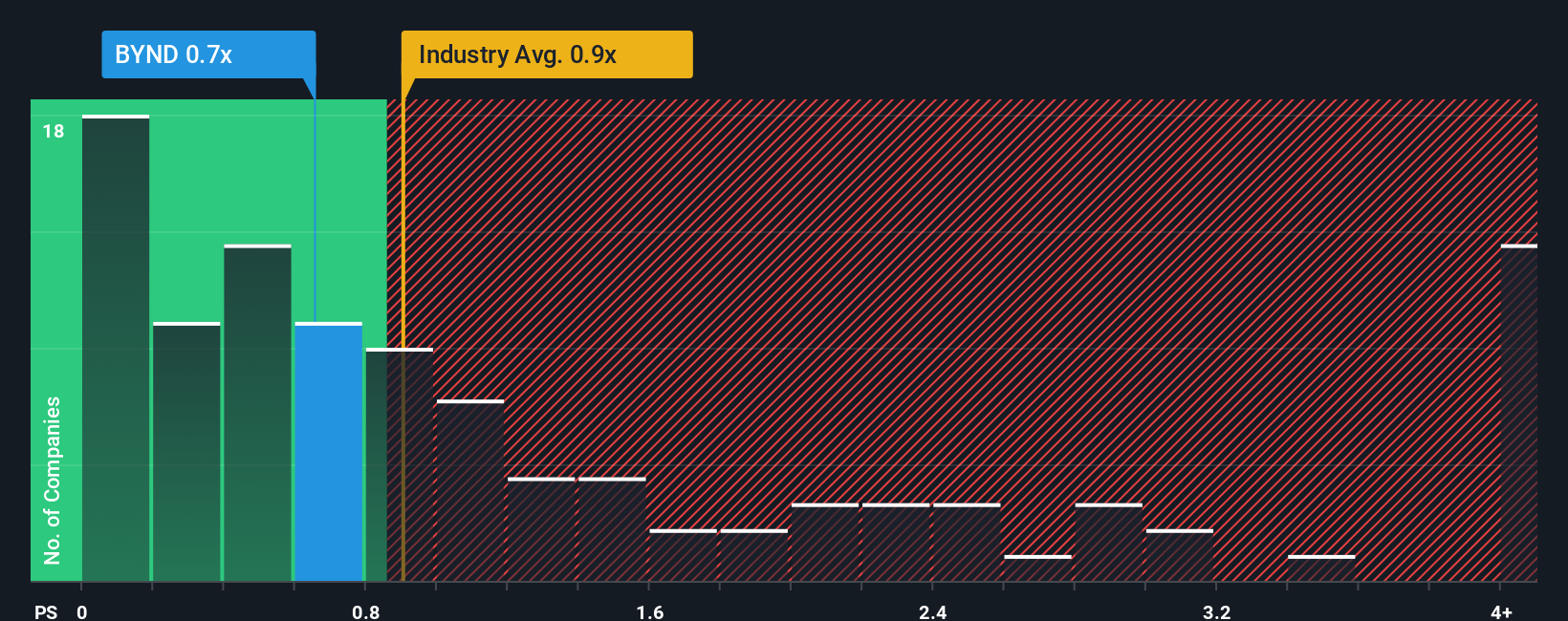

While the previous analysis points to Beyond Meat being undervalued based on narratives and future profit assumptions, the story changes when you compare its price-to-sales ratio to peers. Beyond Meat’s ratio stands at 1.5, higher than the US Food industry’s average of 0.7 and the peer average of 1.4. The fair ratio, which is a level the market could move toward, is 0.6. This emphasizes the risk that the stock may still be too expensive for its sector.

If you see things differently or prefer to dive into the numbers on your own, creating a personalized analysis takes just a few minutes. Do it your way

A great starting point for your Beyond Meat research is our analysis highlighting 4 important warning signs that could impact your investment decision.

Looking for More Standout Investing Opportunities?

Expand your investing playbook and accelerate your portfolio’s growth by targeting stocks with unique potential. Use the Simply Wall Street Screener to quickly zero in on bold trends and tomorrow’s leaders. Don’t miss out while others act.

Capture the momentum of artificial intelligence breakthroughs by adding these 25 AI penny stocks to your watchlist of trailblazers building the next digital frontier.

Maximize your income strategy and lock in attractive yields with these 15 dividend stocks with yields > 3%, focusing on companies proven to deliver stable dividends above 3%.

Get ahead of the curve by identifying companies that may be undervalued right now. See the curated selection at these 920 undervalued stocks based on cash flows and seize the advantage before the crowd moves in.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Beyond Meat might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

A plant-based meat company, engages in the development, manufacture, marketing, and sale of plant-based meat products under the Beyond brand name in the United States and internationally.