Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:LNG

How Early Project Delivery and Accelerated Buybacks at Cheniere Energy (LNG) Have Changed Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent weeks, Cheniere Energy reported strong third-quarter results, beating revenue and EPS expectations, lifting full-year distributable cash flow guidance, and completing the third Train of Corpus Christi Stage 3 ahead of schedule.

- Despite some operational headwinds from feedgas quality issues, positive insider sentiment and sizeable share buybacks have further shaped the company's outlook.

- Now, we'll explore how early project delivery and ongoing buyback activity influence Cheniere Energy's updated investment narrative.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Cheniere Energy Investment Narrative Recap

To own Cheniere Energy, an investor needs to have confidence in the ongoing global demand for LNG and the company’s ability to capitalize on capacity expansions despite growing competition and decarbonization trends. The most important short-term catalyst remains the commissioning of new liquefaction trains and timely completion of expansion projects, while the biggest current risk is a looming global LNG oversupply; the latest operational and financial updates do not materially alter these central drivers.

One particularly relevant announcement is the early completion of the third Train at Corpus Christi Stage 3, which directly supports Cheniere’s capacity-led growth narrative. Bringing new capacity online ahead of schedule can enhance near-term export volumes, underpinning distributable cash flow guidance and helping offset concerns about potential market oversupply as new global projects come online.

However, what some investors may overlook is that capacity expansions alone cannot guard against the risk of prolonged LNG market oversupply, especially as new entrants ramp up output in...

Read the full narrative on Cheniere Energy (it's free!)

Cheniere Energy's outlook anticipates $24.1 billion in revenue and $3.1 billion in earnings by 2028. This forecast requires annual revenue growth of 9.8%, but reflects a decrease of $0.7 billion in earnings from the current $3.8 billion.

Uncover how Cheniere Energy's forecasts yield a $270.67 fair value, a 30% upside to its current price.

Exploring Other Perspectives

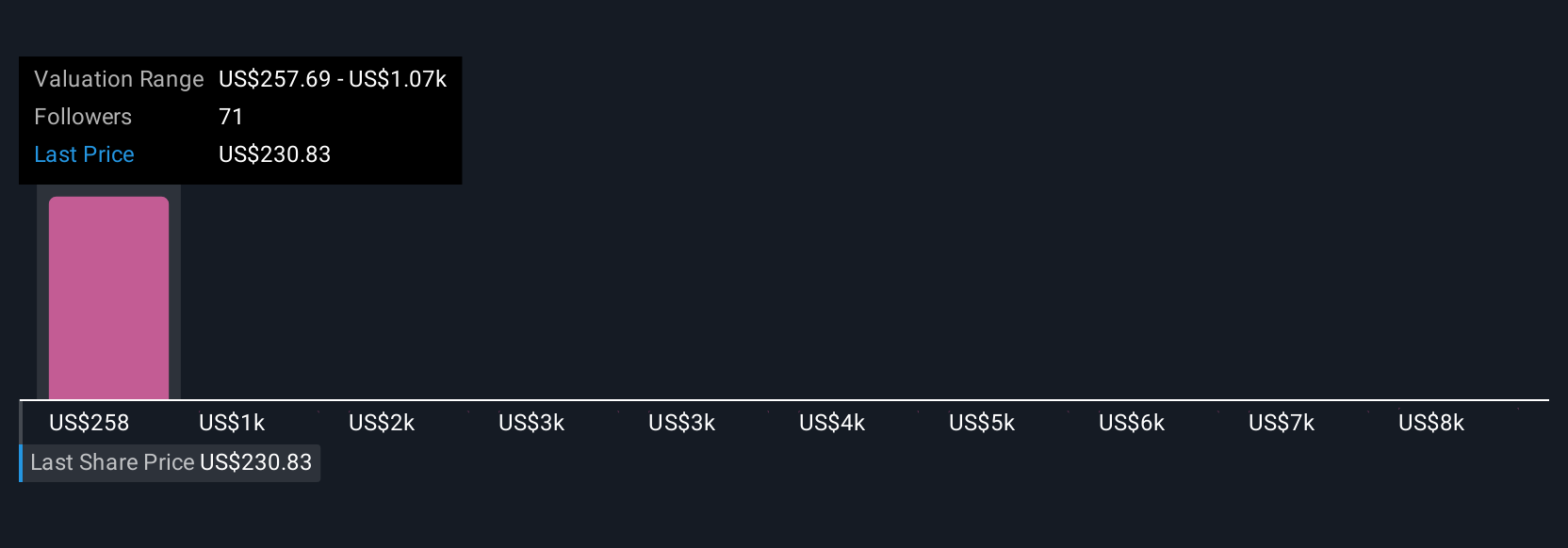

Five independent fair value estimates from the Simply Wall St Community range from US$270.67 to a striking US$6,591.19 per share. As opinions widely differ, keep in mind that the prospect of LNG market oversupply could shift the outlook for Cheniere’s growth and returns, consider looking into several viewpoints before making decisions.

Explore 5 other fair value estimates on Cheniere Energy - why the stock might be worth just $270.67!

Build Your Own Cheniere Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cheniere Energy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Cheniere Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cheniere Energy's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LNG

Cheniere Energy

An energy infrastructure company, primarily engages in the liquefied natural gas (LNG) related businesses in the United States.

Very undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

79 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative