Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:ET

Does Energy Transfer’s 15% Stock Dip Signal an Opportunity After Pipeline Sector Volatility?

Simply Wall St

Reviewed by Bailey Pemberton

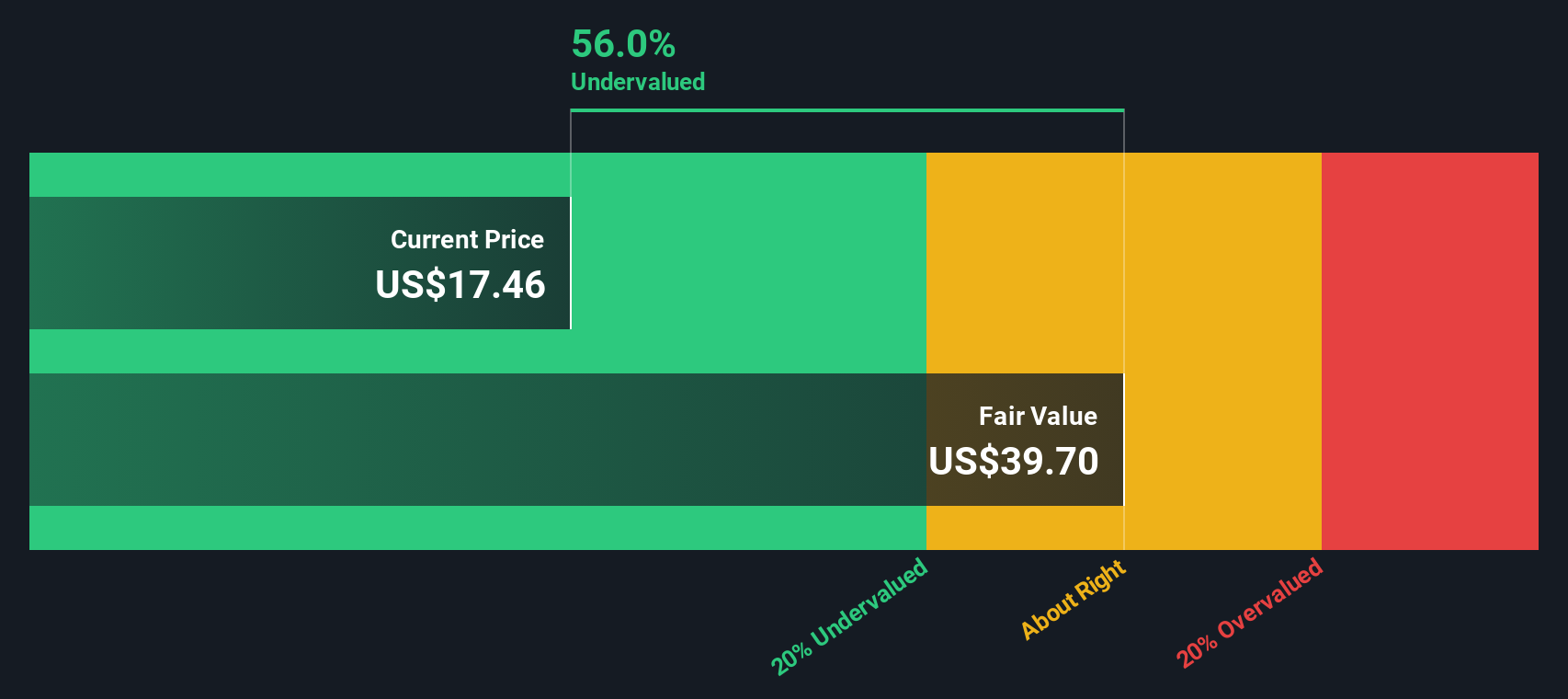

- Wondering if Energy Transfer is fairly priced or if the market is missing something? Let’s dive into what their current stock price really means for anyone considering a position.

- Energy Transfer’s stock has seen some mixed moves recently, with a 1.2% uptick over the past week. However, there has been a year-to-date drop of 15.2% that may have caught some investors off guard.

- Recently, sector headlines about energy infrastructure upgrades and shifting regulations have kept Energy Transfer in the spotlight. Fluctuating oil prices and ongoing discussions around U.S. pipeline expansion have contributed to volatility and renewed debate about the outlook for the midstream sector.

- For those tracking numbers closely, Energy Transfer currently scores 6 out of 6 on our valuation checks, indicating undervaluation by every measure we track. Next, we’ll break down what those models show. At the end of the article, you’ll discover a perspective that goes beyond the numbers.

Find out why Energy Transfer's -9.4% return over the last year is lagging behind its peers.

Approach 1: Energy Transfer Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's true worth by projecting its future cash flows and then discounting those projections back to today's value. This method takes into account both near-term analyst forecasts and longer-term trends, providing a data-driven valuation grounded in fundamental performance.

For Energy Transfer, the latest reported Free Cash Flow stands at $6.8 billion. Analyst estimates see Free Cash Flow rising to $7.8 billion by 2029. After this period, further growth is extrapolated. Beyond the five-year analyst window, Simply Wall St applies moderate long-term growth rates, ultimately projecting Free Cash Flow of about $9.4 billion in a decade. All figures are reported in USD.

Based on these calculations, the DCF-derived intrinsic value for Energy Transfer is $43.63 per share. This represents a steep 61.7% discount compared to the current market price, indicating that the stock may be significantly undervalued at today's levels.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Energy Transfer is undervalued by 61.7%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

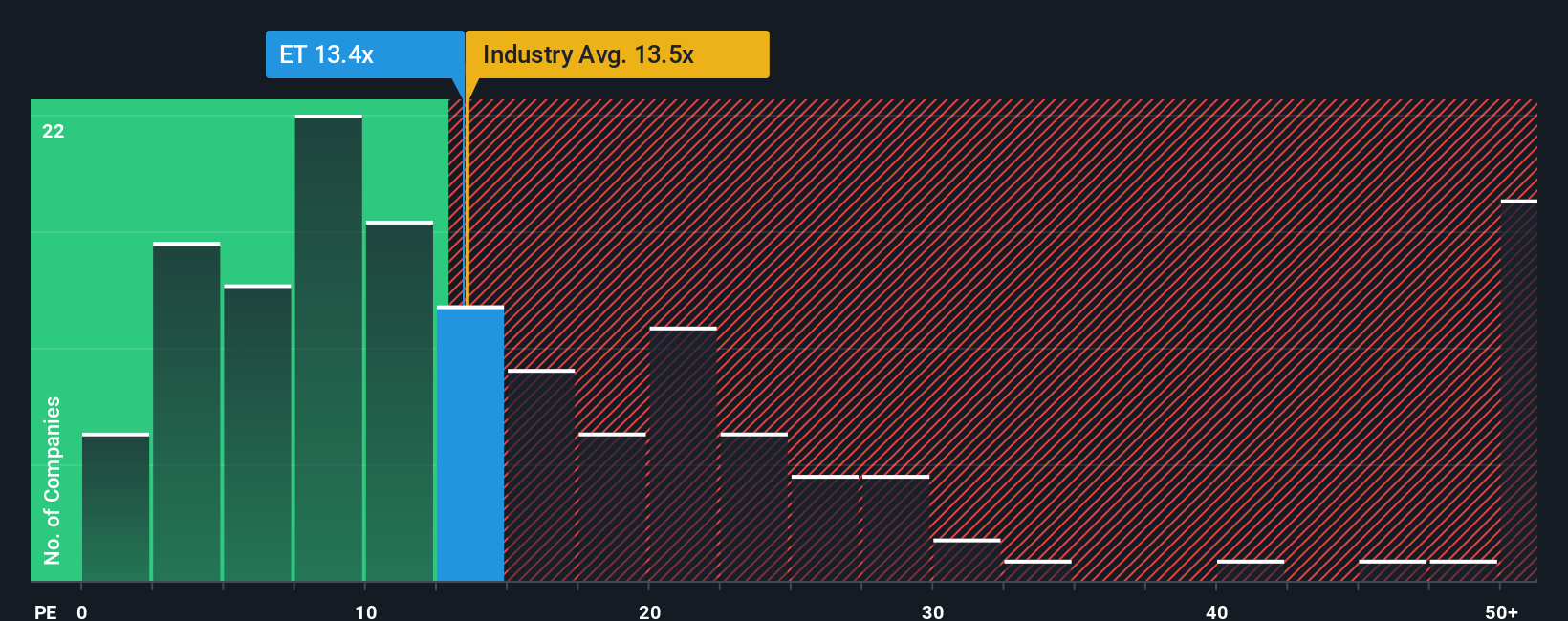

Approach 2: Energy Transfer Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies like Energy Transfer because it directly compares how much investors are willing to pay for a dollar of current earnings. It is especially useful when a company has a steady profit track record, as it helps put its share price into the context of actual performance.

What is considered a “fair” PE ratio is shaped by expectations for growth, the company’s profitability, and overall risk. Faster-growing or more stable companies often command higher PE ratios, while those facing headwinds or increased risks see lower multiples.

Looking at the numbers, Energy Transfer's current PE ratio sits at 13.3x. This is almost in line with the Oil and Gas industry average of 13.4x, but well below the peer group average of 19.2x. This may indicate that investors are more cautious or are pricing in certain risks compared to similar companies.

Simply Wall St’s proprietary “Fair Ratio” digs deeper. It calculates the PE multiple a company should command based on a blend of its earnings growth, profit margins, industry profile, market capitalization, and risk factors. This holistic approach means the Fair Ratio (20.5x for Energy Transfer) often provides a more detailed assessment than simply comparing it to peers or the broad industry, as it incorporates details that standard benchmarks might miss.

With Energy Transfer's PE ratio of 13.3x sitting significantly below its Fair Ratio of 20.5x, the shares appear notably undervalued based on these fundamentals.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

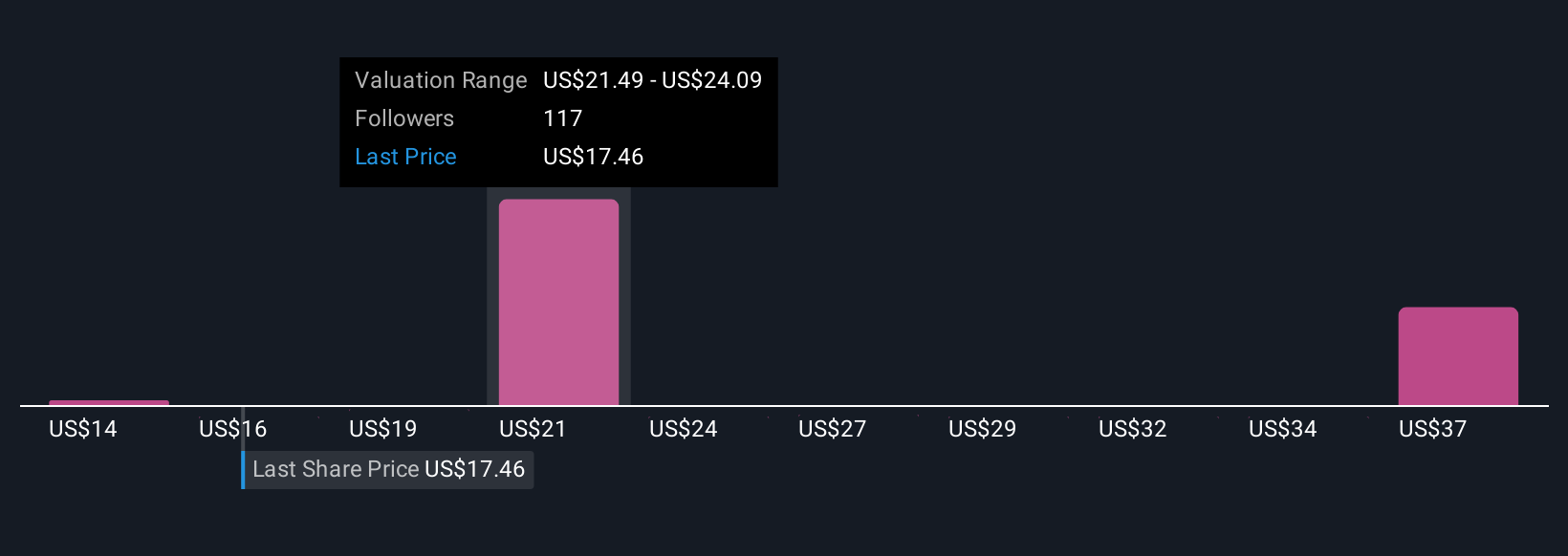

Upgrade Your Decision Making: Choose your Energy Transfer Narrative

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your own story about a company’s future, connecting what you believe about Energy Transfer's business, including its growth, margins, and risks, with financial forecasts and your estimate of fair value. Narratives draw on both the numbers and your perspective, letting you update assumptions and see what a company should be worth based on your chosen scenario.

Narratives are easy and accessible, a tool used by millions of investors within Simply Wall St’s Community page, so you can step beyond static data and link a company’s story to a dynamic model that updates with every new earnings report or news event. They empower you to act confidently by comparing your Fair Value to the current Price, helping you spot when to buy, sell, or hold, all transparently grounded in your beliefs and the latest information.

For example, some investors see Energy Transfer’s diversified assets and rising export capacity supporting higher long-term earnings and assign a fair value close to the most bullish analyst target, while others focus on regulatory or fossil fuel risks and set their fair value toward the lower end of the range. Narratives put your view at the center of your investing process, making smarter investment decisions personal and easy.

Do you think there's more to the story for Energy Transfer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Energy Transfer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ET

Undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative