Delek Logistics Partners (DKL) has seen its stock move higher recently, continuing a steady performance over the past year. Investors may be taking notice of consistent revenue growth paired with improving net income, as reflected in its returns.

DKL’s latest share price of $45.82 reflects steady upward momentum, with a 1-year total shareholder return of 27.0%. This points to a healthy mix of near-term enthusiasm and confidence in its long-term trajectory. In the past several months, performance has built rather than faded, giving investors more reason to watch for emerging growth signals as the year unfolds.

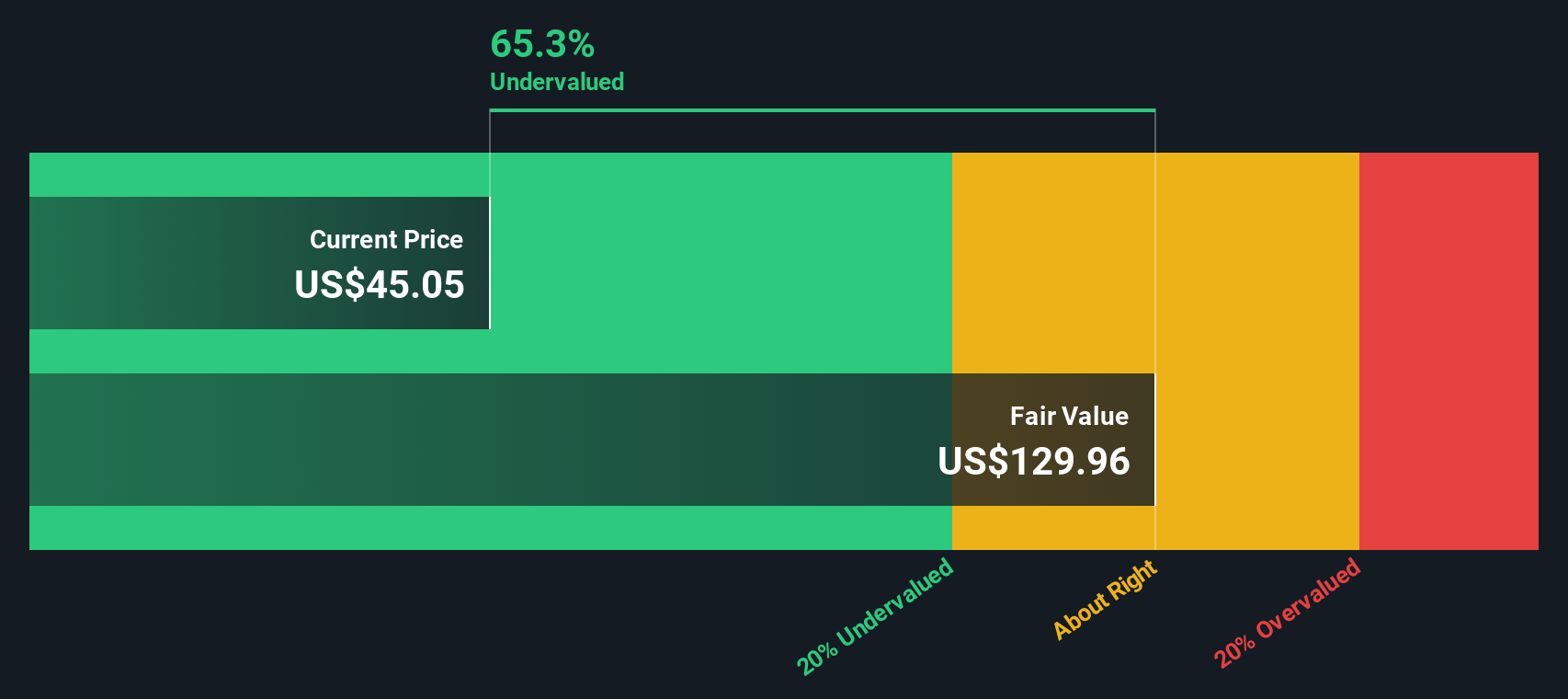

With the stock’s strong run and positive returns, the key question is whether Delek Logistics Partners remains undervalued, or if the market has already factored in all the potential upside for future growth.

Advertisement

Most Popular Narrative: 4.7% Overvalued

With Delek Logistics Partners' fair value estimate coming in just below its recent closing price, market expectations are closely aligned with the most popular valuation narrative. Investors eyeing the current share price may want to consider what is underpinning this consensus, especially in a sector defined by shifting demand and capital investment cycles.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs. This is likely to boost gathering and processing volumes, EBITDA, and revenue growth. Delek Logistics' unique, vertically integrated offerings in the Permian, including handling of crude, gas, and water, plus advanced sour gas solutions, provide a competitive advantage as supply chain resilience and U.S. energy security remain priorities. These factors support high utilization of existing assets and margin improvement.

Want to decode what is fueling this valuation call? The engine of this narrative is bold expansion bets and future profit margins that could flip expectations on their head. Engines are firing, but will the market buy the long-term growth pitch? Dive in to uncover the projections this narrative is built on.

However, recent acquisitions and rising leverage mean that any slowdown in energy demand or cash flows could quickly challenge Delek Logistics Partners' bullish outlook.

Another View: Discounted Cash Flow Signals Undervaluation

While conventional valuation suggests Delek Logistics Partners is slightly overvalued, our SWS DCF model offers a sharply different perspective. According to this approach, DKL shares are actually trading well below their calculated fair value, which may indicate a hidden upside the market is overlooking. Could this disconnect present a window of opportunity, or is there something the DCF model does not capture?

If you have your own perspective or want to dig into the data first-hand, you can easily piece together your own investment story in just a few minutes. Do it your way

A great starting point for your Delek Logistics Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock your advantage by tapping into smart, pre-screened stock selections that align with tomorrow's trends. Discover expertly curated opportunities designed to put you ahead.

Spot growing tech giants early by checking out these 26 AI penny stocks, leading the way in artificial intelligence innovation.

Start building a portfolio of reliable passive income by browsing these 14 dividend stocks with yields > 3%, offering yields that beat the traditional market average.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Provides gathering, pipeline, transportation, and other services for crude oil, intermediates, refined products, natural gas, storage, wholesale marketing, terminalling water disposal and recycling customers in the United States.