Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:CRGY

Will Crescent Energy’s (CRGY) Rocky Mountain Exit Refocus Its Long-Term Growth Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Crescent Energy recently agreed to sell its drilling portfolio in the US Rocky Mountain region for over US$400 million, aiming to reinforce its balance sheet and sharpen its focus on core operations in the Eagle Ford and Uinta basins.

- This move follows a period in which Crescent Energy reported robust third-quarter results, including better-than-expected adjusted EPS and a 16.3% increase in year-over-year revenue.

- We'll examine how the divestment of Rocky Mountain assets may influence Crescent Energy's long-term operational strategy and investment outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Crescent Energy Investment Narrative Recap

To own Crescent Energy stock, you need to believe in the company’s approach of growing through acquisitions and divestitures in key U.S. basins, supported by operational improvements and a stable energy market. The recent sale of Rocky Mountain assets for over US$400 million is not expected to materially disrupt Crescent’s near-term catalysts, which remain tied to balance sheet strength and capital efficiency, but integration risk related to recent and future transactions is still a consideration for shareholders.

Among recent announcements, the substantial upsizing of Crescent’s borrowing base and extension of its credit facility, completed just weeks before the asset sale, stands out. This move further reinforces the company’s liquidity and flexibility, factors that matter as Crescent pivots its capital and operational focus to the Eagle Ford and Uinta basins, supporting its core catalyst of production efficiency and margin improvement.

In contrast, investors should also be aware of how reliance on acquisitions and asset sales raises the stakes if any integration or execution missteps occur...

Read the full narrative on Crescent Energy (it's free!)

Crescent Energy's outlook projects $5.2 billion in revenue and $672.6 million in earnings by 2028. This requires a 14.8% annual revenue growth rate and a $649.5 million increase in earnings from the current $23.1 million.

Uncover how Crescent Energy's forecasts yield a $14.18 fair value, a 61% upside to its current price.

Exploring Other Perspectives

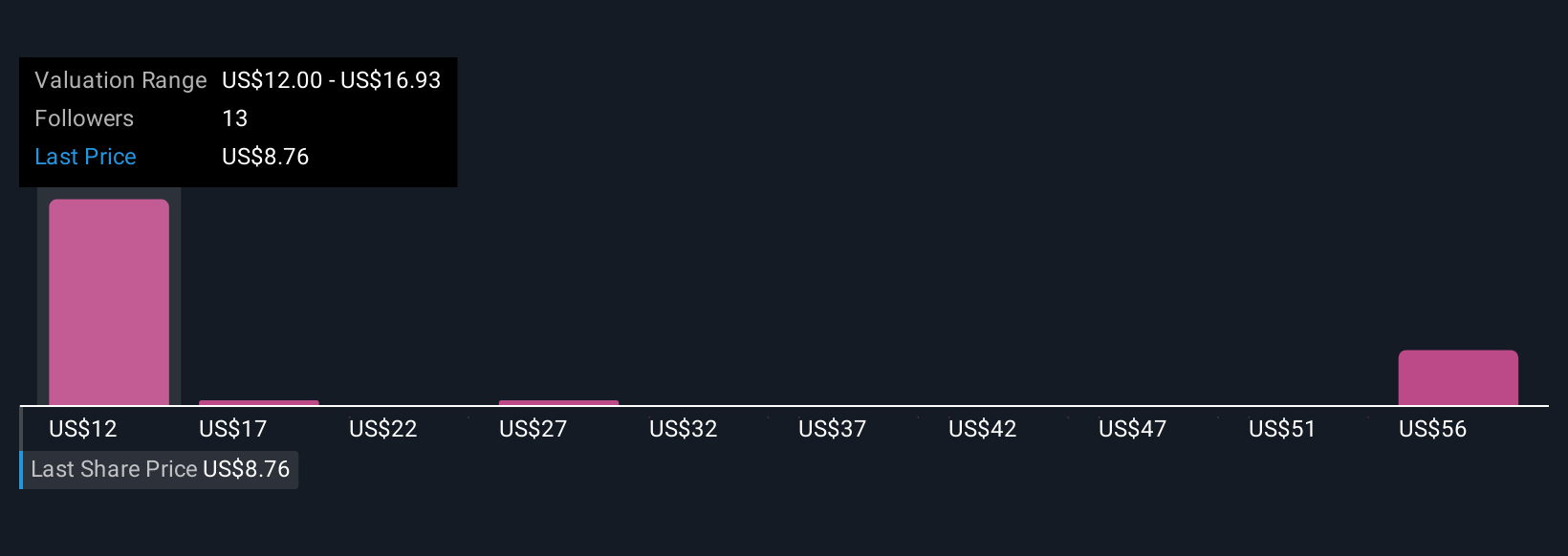

Fair value estimates from five Simply Wall St Community members range from US$12 to US$55.90 per share, reflecting wide variation in growth forecasts and return expectations. As current analyst consensus centers on robust earnings growth supporting future cash flow, it’s clear opinions can widely differ, consider exploring these alternative viewpoints before reaching your own conclusion.

Explore 5 other fair value estimates on Crescent Energy - why the stock might be worth over 6x more than the current price!

Build Your Own Crescent Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Crescent Energy research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Crescent Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crescent Energy's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CRGY

Crescent Energy

An energy company, engages in the exploration and production of crude oil, natural gas, and natural gas liquids in the United States.

Slight risk and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative