CNX Resources (CNX) has quietly outperformed over the past three months, gaining 16%. Investors may be weighing continued revenue and net income growth as they consider the stock's value after recent trading action.

After a solid 16% run-up over the past three months, CNX Resources is starting to capture more attention. While the year-to-date share price return remains negative, the momentum seen recently stands out against the backdrop of a modest one-year total shareholder loss and the stock’s impressive 285% five-year total return. This recent uptick could hint at shifting sentiment, especially as the company continues to deliver steady revenue and net income growth.

But after this surge and a strong track record, is CNX Resources trading at a bargain that investors should seize? Or is the market already factoring in all the company’s future growth potential?

Advertisement

Most Popular Narrative: 4.5% Overvalued

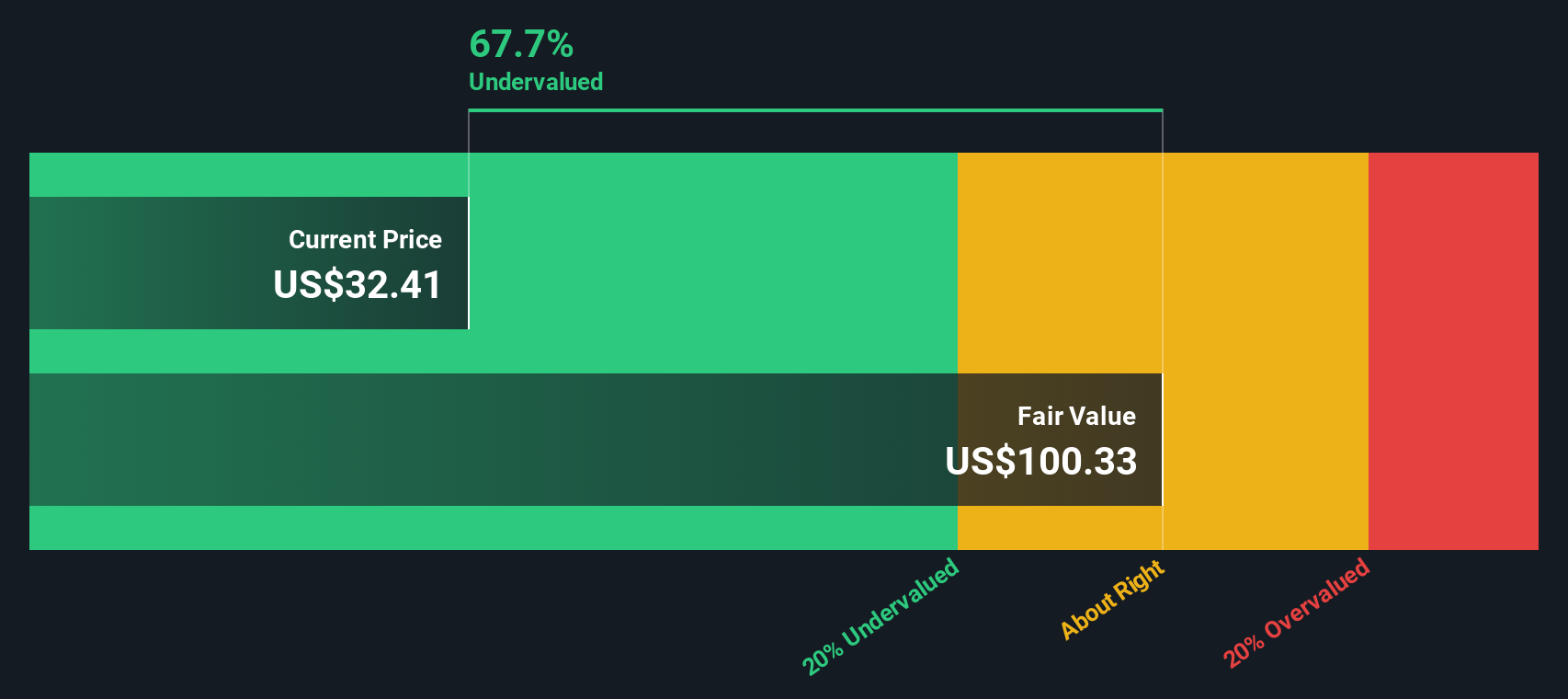

At $33.66 per share, CNX Resources trades above the most widely followed narrative's fair value of $32.21. This market optimism now faces the test of whether the company can deliver on sizable growth assumptions embedded in the consensus price target.

Favorable policy and regulatory shifts towards cleaner-burning natural gas, including programs like 45Z tax credits and renewable energy attribute markets, are creating new, high-margin revenue streams (e.g., RMG sales, environmental credits). These changes have the potential to enhance both net margins and free cash flow.

Curious how these new revenue streams and environmental credits may fuel future profits? The narrative relies on accelerating margins and regulatory tailwinds. What are the bold projections shaping this potential payday? Dig into the full story to uncover the surprising expectations driving that fair value.

While consensus suggests CNX Resources may be a bit overvalued based on analyst targets, our SWS DCF model paints a much different picture, estimating fair value at $152.22, far above the current price. This gap hints at a possible undervalued opportunity or perhaps a disconnect between market consensus and intrinsic value. Which outlook will prove right as market conditions evolve?

If you see things differently or have your own perspective, you can dive into the numbers and craft your own unique narrative in just a few minutes: Do it your way.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

An independent natural gas and midstream company, engages in the acquisition, exploration, development, and production of natural gas properties in the Appalachian Basin.