Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:SPGI

Assessing S&P Global’s (SPGI) Valuation as Long-Term Returns Outpace Recent Performance

Simply Wall St

Reviewed by Simply Wall St

S&P Global (SPGI) has quietly continued its work in the financial data and analytics sector, offering investors steady exposure to essential market infrastructure. With a history stretching back over a century, its diversified business remains an anchor for many portfolios.

See our latest analysis for S&P Global.

After a steady climb throughout much of the past year, S&P Global’s share price has recently cooled. The stock is up just 0.7% year-to-date, while the 1-year total shareholder return sits at -3.8%. Despite the short-term ebb in momentum, long-term shareholders still see impressive gains, with a 3-year total shareholder return of 42% and 53% over five years. This highlights the company’s resilience and compounding potential.

If you’re interested in finding standout companies with strong trajectories, this is a perfect moment to broaden your watchlist and discover fast growing stocks with high insider ownership

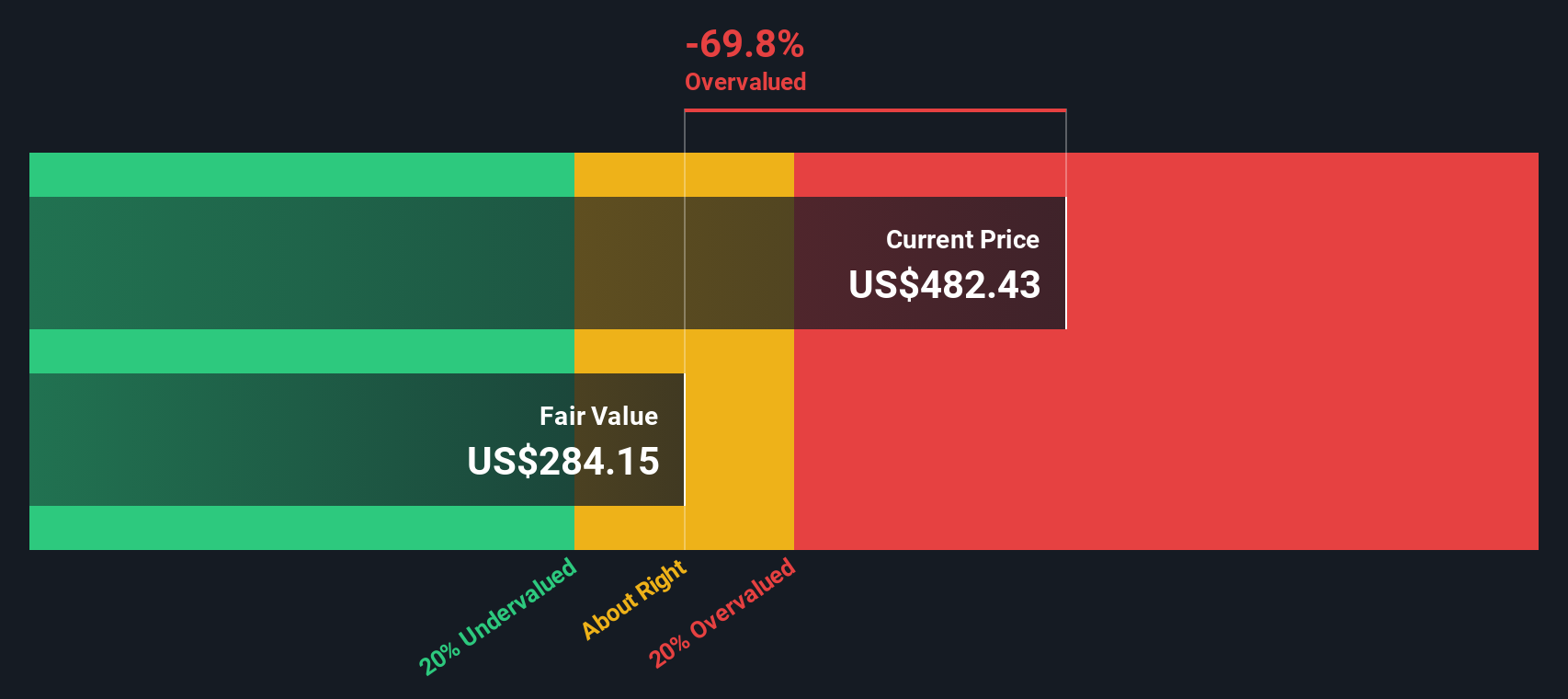

With the stock trading near its recent highs but trailing analyst targets by a wide margin, investors are left to wonder: is S&P Global’s current price a bargain hiding in plain sight, or has the market already factored in its future growth?

Price-to-Earnings of 35.8x: Is it justified?

S&P Global currently trades at a price-to-earnings (P/E) ratio of 35.8x, standing well above both sector and peer averages. This raises important questions about how the market is valuing its long-term earnings potential.

The price-to-earnings ratio measures how much investors are willing to pay for each dollar of the company's earnings. It is commonly used to gauge whether a stock is priced fairly relative to company performance and industry standards. High values often signal market optimism or premium positioning.

S&P Global’s current P/E ratio exceeds both the US Capital Markets industry average of 23.9x and its closest peers, who average 31.7x. This suggests the market is pricing in strong expectations for the company’s future growth and profitability, potentially beyond what is seen in the broader sector. Compared to an estimated fair P/E ratio of 18.2x, S&P Global's valuation appears stretched, indicating the stock could face downward pressure if earnings growth does not materialize as strongly as anticipated.

Explore the SWS fair ratio for S&P Global

Result: Price-to-Earnings of 35.8x (OVERVALUED)

However, sustained overvaluation or slower than expected revenue growth could cause sentiment to shift, putting additional pressure on S&P Global’s share price.

Find out about the key risks to this S&P Global narrative.

Another View: Discounted Cash Flow Says Overvalued

While the price-to-earnings ratio signals that S&P Global is trading at a premium, our DCF model offers a different perspective. According to our analysis, the shares trade well above their estimated intrinsic value of $313.36. This suggests that the stock may be overvalued from a cash flow standpoint. Could the market be too optimistic, or are there qualitative factors not reflected in the numbers?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out S&P Global for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own S&P Global Narrative

If you see things differently or want to test your own insights, you can compile your personal view in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding S&P Global.

Looking for More Investment Ideas?

Don’t limit your opportunities to just one sector. Broaden your research with our hand-picked screeners that spotlight tomorrow’s trends and hidden strengths. Let Simply Wall St help you spot the next big market winners before everyone else.

- Capture the upside of technological innovation by analyzing these 25 AI penny stocks that are transforming industries with smart automation, data science, and real-world AI applications.

- Maximize your income potential by evaluating these 15 dividend stocks with yields > 3% that offer reliable yields above 3% for a steady stream of returns.

- Get ahead of the next financial evolution by looking at these 81 cryptocurrency and blockchain stocks that are powering the future of secure transactions and digital transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SPGI

S&P Global

Provides credit ratings, benchmarks, analytics, and workflow solutions in the global capital, commodity, and automotive markets.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative