Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:MSCI

Exploring MSCI (MSCI) Valuation as Wall Street Buy Calls and Strategic Moves Boost Investor Optimism

Simply Wall St

Reviewed by Simply Wall St

MSCI (MSCI) has caught the market’s attention following a fresh round of buy and overweight calls from Wall Street. The company has also seen recent insider share purchases and ongoing executive transitions within the firm.

See our latest analysis for MSCI.

MSCI has traded in a fairly tight range this year despite policy changes and a continued stream of strategic updates, with the share price hovering near $563.45 and a one-year total shareholder return of -6.4%. While momentum has paused, the company’s longer-term gains remain intact, highlighted by a 41% total return over five years. This suggests that investors remain optimistic about MSCI’s ability to adapt and expand, even as leadership roles shift and the outlook for digital asset exposure in its indexes evolves.

If MSCI’s blend of innovation and executive change has you wondering what else is gaining traction, now might be the perfect time to discover fast growing stocks with high insider ownership

With the stock trading below analyst price targets and fresh buy ratings still arriving, investors are left to wonder whether MSCI is currently underappreciated by the market or if future growth is already fully reflected in its share price.

Most Popular Narrative: 14.0% Undervalued

With the narrative’s fair value of $655.06 sitting well above the last close price of $563.45, there is a clear disconnect between what analysts expect and where the market currently stands.

Accelerated development and cross-selling of proprietary data, analytics, and private capital solutions (including recently launched products and business lines like private equity benchmarks and risk tools) will tap into new client bases and increase wallet share among institutional clients. This may drive durable multi-year compounded revenue growth.

Curious what is behind this bullish narrative? The foundation for this premium valuation is not just historical performance. Deep within the forecasts are assumptions about high-margin revenue growth and profit expansion that could surprise even seasoned investors. Only a closer look reveals which metrics move the needle and why the consensus is so confident.

Result: Fair Value of $655.06 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slowing growth in Sustainability products and increasing competition could challenge MSCI’s ability to maintain its strong premium and consistent revenue momentum.

Find out about the key risks to this MSCI narrative.

Another View: Multiples Tell a Cautionary Tale

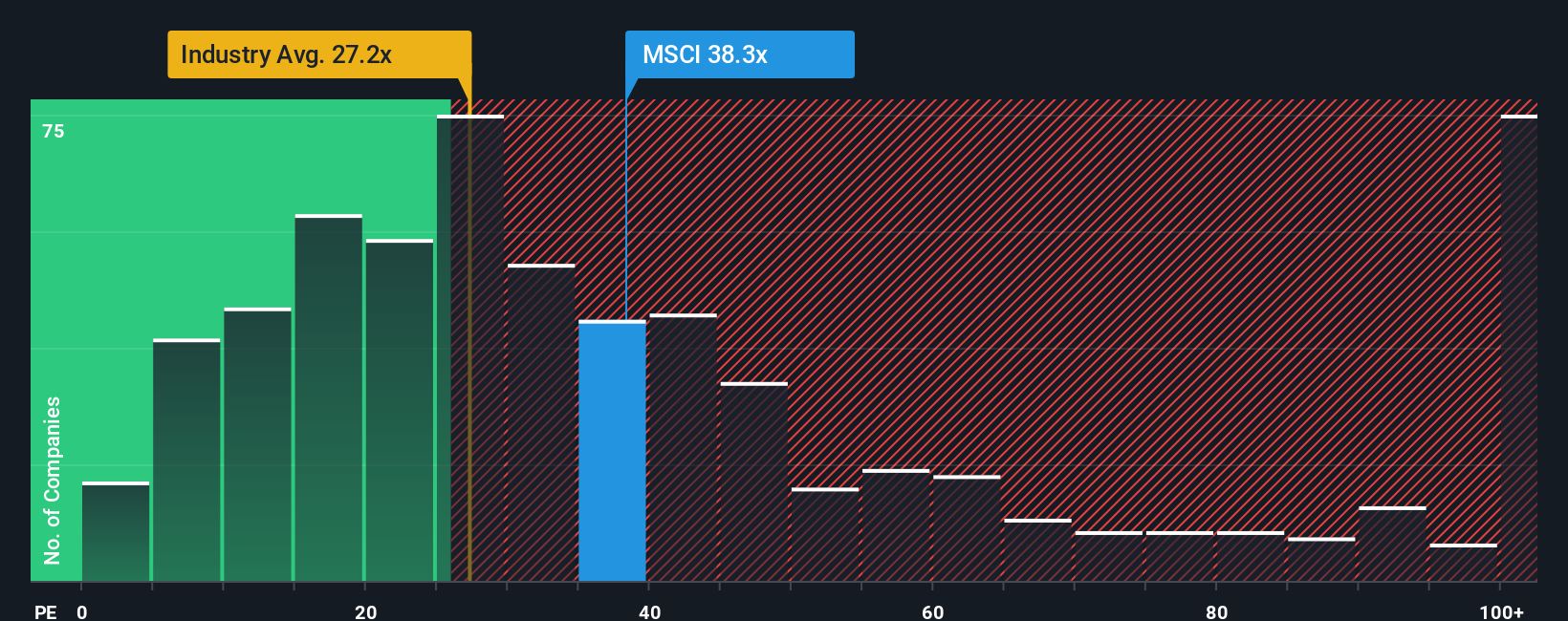

Looking at valuation through the lens of the price-to-earnings ratio, MSCI trades at 34.6x, making it more expensive than the US Capital Markets industry (23.6x), its peer average (33.9x), and notably higher than the fair ratio of 16.6x. This sizable premium signals that investors are paying a hefty price for future growth, raising the risk if expectations are not met. Does this reflect justified optimism, or could the stock be vulnerable to a shift in market sentiment?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own MSCI Narrative

If you see a different story in the numbers or want to dive deeper on your own terms, it’s quick and easy to form your own perspective. Do it in just a few minutes and Do it your way.

A great starting point for your MSCI research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Seize the opportunity to broaden your portfolio with some of the market’s most intriguing stocks, handpicked for breakout potential, steady yields, and innovation. Don’t wait and risk missing your edge in today’s fast-moving market.

- Supercharge your watchlist by targeting impressive yields. Unlock opportunities with these 15 dividend stocks with yields > 3% offering above-average income potential.

- Get ahead of market trends and position yourself for tomorrow’s breakthroughs by checking out these 25 AI penny stocks transforming industries with artificial intelligence.

- Tap into unique value plays before the crowd by exploring these 920 undervalued stocks based on cash flows that might be flying under Wall Street’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MSCI

MSCI

Provides critical decision support tools and solutions for the investment community to manage investment processes worldwide.

Average dividend payer with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative