Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:MS

Morgan Stanley’s Valuation After Dutch Tax Resolution and Strategic Crypto Expansion

Simply Wall St

Reviewed by Simply Wall St

Morgan Stanley (NYSE:MS) is making headlines after resolving a Dutch tax case that had been hanging over the bank for years. By accepting penalty orders and repaying withheld taxes, the company has removed a key legal uncertainty.

See our latest analysis for Morgan Stanley.

With the Dutch tax saga finally resolved and fresh fixed-income offerings underscoring stable demand, Morgan Stanley’s shares have maintained strong momentum, posting a year-to-date share price return of nearly 36%. Impressive three- and five-year total shareholder returns, at 104% and 206% respectively, suggest long-term confidence. Recent plans to expand crypto services and a dip in short interest also point to intensifying investor optimism.

If you’re interested in what else is capturing market attention, now’s the perfect moment to broaden your perspective and discover fast growing stocks with high insider ownership

The question for investors now is whether Morgan Stanley’s impressive run still leaves room for upside, or if the market has already factored in all future growth. Is there a new buying opportunity, or is everything priced in?

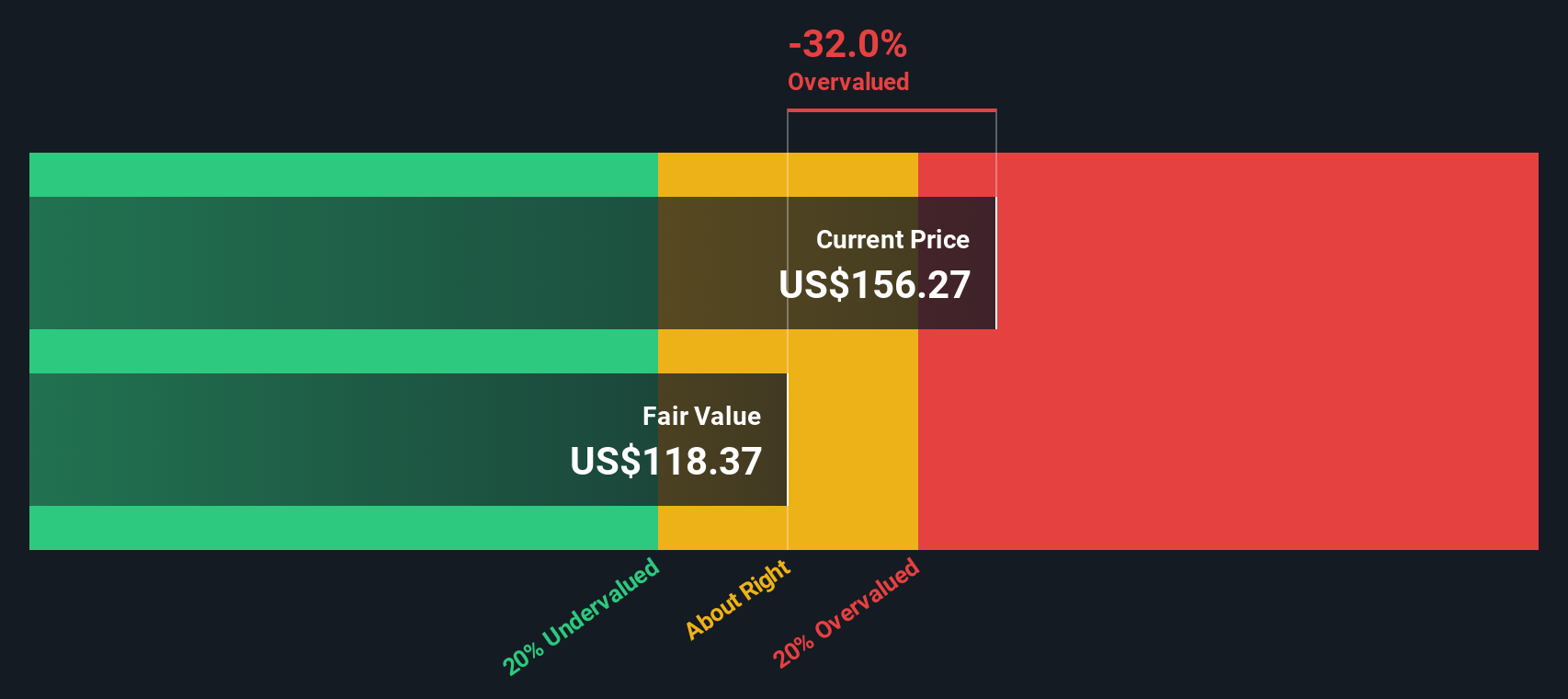

Most Popular Narrative: Fairly Valued

With Morgan Stanley's last close price closely matching the consensus narrative’s fair value estimate, the market appears to be in balance. Investors seem divided, creating an opportunity for deeper analysis of the factors maintaining this equilibrium.

The ongoing increase in global wealth, combined with the accelerating intergenerational transfer of assets, is boosting demand for comprehensive advisory and wealth management solutions. This is evidenced by record net new assets and a growing client base, which may drive higher recurring fee-based revenue and long-term earnings growth.

Looking to understand what is influencing the current price? The prevailing narrative centers on strong forecasts for recurring revenues, an expanding presence, and the expectation of margin growth beginning to gain traction. What underlying assumptions support these high expectations? The answers may be unexpected.

Result: Fair Value of $168.15 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising regulatory scrutiny and surging competition from low-fee products could quickly shift Morgan Stanley’s outlook. This could challenge both margins and growth expectations.

Find out about the key risks to this Morgan Stanley narrative.

Another View: Discounted Cash Flow Model Raises Questions

While current market multiples suggest Morgan Stanley is fairly valued, our SWS DCF model presents a different perspective. According to this approach, Morgan Stanley is trading above its intrinsic value, indicating potential overvaluation if future cash flows do not meet high expectations. Which story should investors trust?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Morgan Stanley Narrative

If you’d rather form your own view or bring a fresh angle to the table, you can analyze the latest data and build your own take in just a few minutes by starting with Do it your way.

A great starting point for your Morgan Stanley research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Sharpen your strategy and get ahead by tapping into new sectors and market trends. Don’t let opportunities pass you by when powerful tools are just a click away.

- Capitalize on remarkable cash flow potential by tracking these 920 undervalued stocks based on cash flows that could be flying under the radar today.

- Target stability and income with these 15 dividend stocks with yields > 3% yielding over 3%, which is ideal for building a robust, income-driven portfolio.

- Unleash your portfolio’s growth with these 25 AI penny stocks making waves at the cutting edge of artificial intelligence innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MS

Morgan Stanley

A financial holding company, provides various financial products and services to governments, financial institutions, and individuals in the Americas, Asia, Europe, Middle East, and Africa.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative