Moody's (MCO) shares have seen modest shifts over the past week, with investors keeping an eye on recent trends in the diversified financials sector. The stock has moved slightly, even as broader markets show mixed signals.

This week's dip comes after a gradual fade in momentum for Moody's, with the share price posting a 4.6% drop over the past 7 days and trading at $470.16. However, when you zoom out, the stock's three-year total shareholder return of 63% stands out as a reminder that long-term holders have been well rewarded despite recent softness.

With shares trading below analyst targets but following years of strong gains, the real question is whether Moody's is now offering hidden value or if investors have already factored in all of its future growth.

Advertisement

Most Popular Narrative: 13.8% Undervalued

Compared to Moody's last close at $470.16, the most widely followed narrative suggests there is notable upside, with a fair value set much higher. Investors are watching to see if these forecasts hold up in the months ahead.

Moody's is experiencing accelerating demand from the rapid evolution and expansion of private credit markets. This is evidenced by 75% year-over-year growth in private credit revenues, 25% of first-time mandates coming from private credit, and ongoing issuer and investor demand for independent risk assessment. These factors strongly support future revenue growth and earnings resilience as private credit's share in global financing expands.

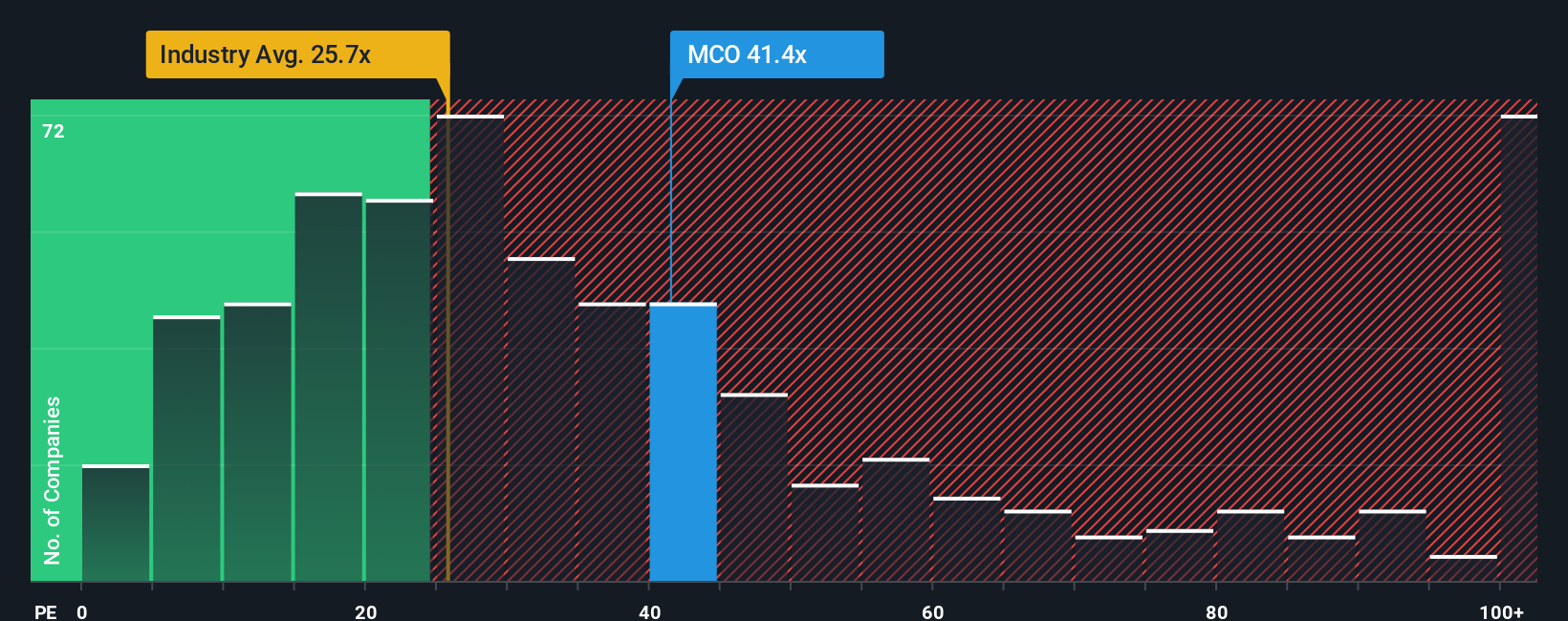

Want to see what headline-grabbing assumptions lead to this bullish price target? Buried in the narrative are aggressive profit forecasts and a multiple that towers over industry averages. Discover the bold expectations that could reshape how the market prices Moody's in the future.

However, increased regulatory scrutiny and rising competition from AI-powered rivals could limit Moody's pricing power and slow its projected margin gains.

Another View: Profit Multiples Challenge the Optimism

While analyst earnings forecasts are bullish, the company's share price still looks lofty by classic profit yardsticks. Moody's trades at a 37.4x earnings multiple, much higher than both the US industry average of 23.7x and the peer average of 30x. Its ratio is also well above the fair ratio of 17.8x. The market could eventually drift toward this level if sentiment shifts. Is the current premium justified by future growth, or does it set up valuation risk as optimism cools?

There’s a whole world of opportunities waiting, and you can unlock them right now with the right tools. Don’t let your next winning investment pass you by.

Jump on the trend toward automation and robotics by checking out these 27 AI penny stocks which are making headlines for their disruptive potential.

Stay ahead of innovation as you uncover growth stories inside these 26 quantum computing stocks that are transforming the future of computing and security.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks