Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:MAIN

Is MAIN’s Added Senior Secured Exposure to Chamberlin Quietly Reframing Main Street Capital’s Risk Profile?

Simply Wall St

Reviewed by Sasha Jovanovic

- Main Street Capital Corporation recently completed a follow-on investment, providing an additional US$20.0 million first lien, senior secured term debt to portfolio company Chamberlin Holding LLC to support its acquisition of a commercial roofing contractor in the Southeastern United States.

- This additional capital deepens Main Street Capital’s multi-year relationship with Chamberlin and backs an expansion of the roofing contractor’s geographic footprint beyond its Southwest base.

- We’ll now explore how Main Street Capital’s expanded senior secured exposure to Chamberlin influences the company’s existing investment narrative and risk profile.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Main Street Capital Investment Narrative Recap

Main Street Capital appeals to investors who want diversified, income focused exposure to lower middle market and private loans, backed by secured lending and a long record of regular and supplemental dividends. The additional US$20.0 million first lien term debt to Chamberlin modestly increases portfolio concentration in one borrower, but does not materially change the near term focus on credit quality and nonaccrual risk as the key swing factor for the stock.

The most relevant recent announcement alongside this Chamberlin follow on is Main Street’s decision, via MSC Income Fund, to concentrate that vehicle solely on private loan investments with adjusted fees. Together, these moves tilt the overall platform further toward interest income from secured credit, which can support dividends but also amplifies the importance of underwriting discipline and the internal resources needed to manage a larger, more complex loan book.

Yet beneath the steady stream of dividends, investors should be aware of the growing execution risk around underwriting and monitoring an expanding portfolio...

Read the full narrative on Main Street Capital (it's free!)

Main Street Capital's narrative projects $611.1 million revenue and $227.4 million earnings by 2028. This requires 4.9% yearly revenue growth and an earnings decrease of $245.5 million from $472.9 million today.

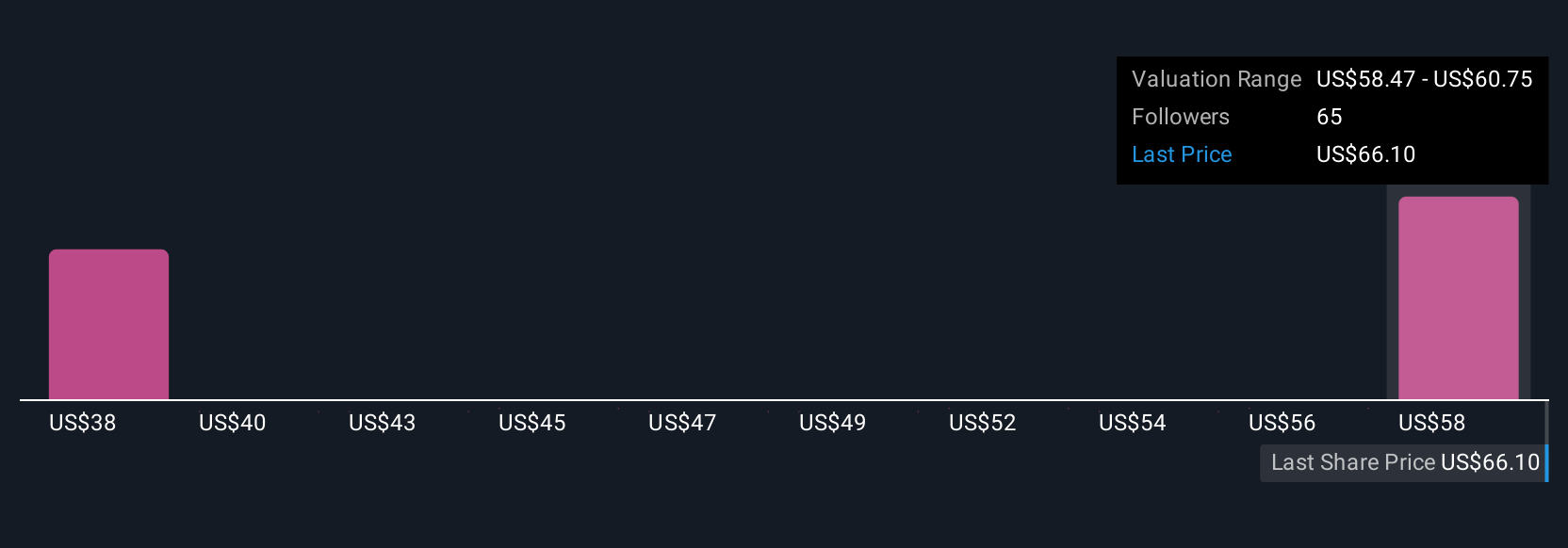

Uncover how Main Street Capital's forecasts yield a $60.67 fair value, in line with its current price.

Exploring Other Perspectives

Eight fair value estimates from the Simply Wall St Community span roughly US$37 to about US$60.67, so you see very different views on Main Street Capital’s worth. Set against concerns about rising nonaccrual risk and the strain of vetting more lower middle market deals, this spread underlines why you may want to compare several independent viewpoints before forming your own expectations for the stock.

Explore 8 other fair value estimates on Main Street Capital - why the stock might be worth 39% less than the current price!

Build Your Own Main Street Capital Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Main Street Capital research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Main Street Capital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Main Street Capital's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MAIN

Main Street Capital

A business development company and a small business investment company specializing in direct and indirect investments.

Average dividend payer with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

54 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

54 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative