Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:MA

How Mastercard’s (MA) Support for Self-Custody Crypto Wallets Is Shaping Its Digital Payments Narrative

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 18, 2025, Mercuryo, Polygon Labs, and Mastercard announced an expansion of Mastercard Crypto Credential to include self-custody wallets, enabling verified, alias-based crypto transfers for consumers and businesses using blockchain networks.

- This collaboration marks the first time a native blockchain network will support Mastercard's verification platform, signaling growing integration of regulated crypto infrastructure into mainstream digital payments.

- We'll examine how Mastercard's move to support self-custody wallets in crypto could influence its ongoing digital payments growth narrative.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

Mastercard Investment Narrative Recap

Being a Mastercard shareholder means believing in the company's ability to lead and adapt as digital payments transform worldwide, with ongoing innovation playing a key role. The newest self-custody crypto wallet integration demonstrates Mastercard's commitment to broadening its digital payments reach. However, this move does not appear to materially impact the primary catalyst, accelerating adoption of digital payments globally, or the biggest risk, which remains the potential erosion of payment volumes from the rise of alternative payment rails in major emerging markets.

A relevant recent announcement is Mastercard’s expansion into stablecoin infrastructure through its Multi-Token Network and Mastercard Move platform. These partnerships with Circle to facilitate real-time, stablecoin-based settlements across several regions align closely with efforts to ensure the company's payment network remains central to both traditional and blockchain-based transactions.

On the other hand, investors should be aware that as Mastercard diversifies into crypto and blockchain, competitive threats from alternative and domestic payment systems are…

Read the full narrative on Mastercard (it's free!)

Mastercard's outlook anticipates $42.6 billion in revenue and $19.9 billion in earnings by 2028. This calls for 12.1% annual revenue growth and a $6.3 billion increase in earnings from the current $13.6 billion level.

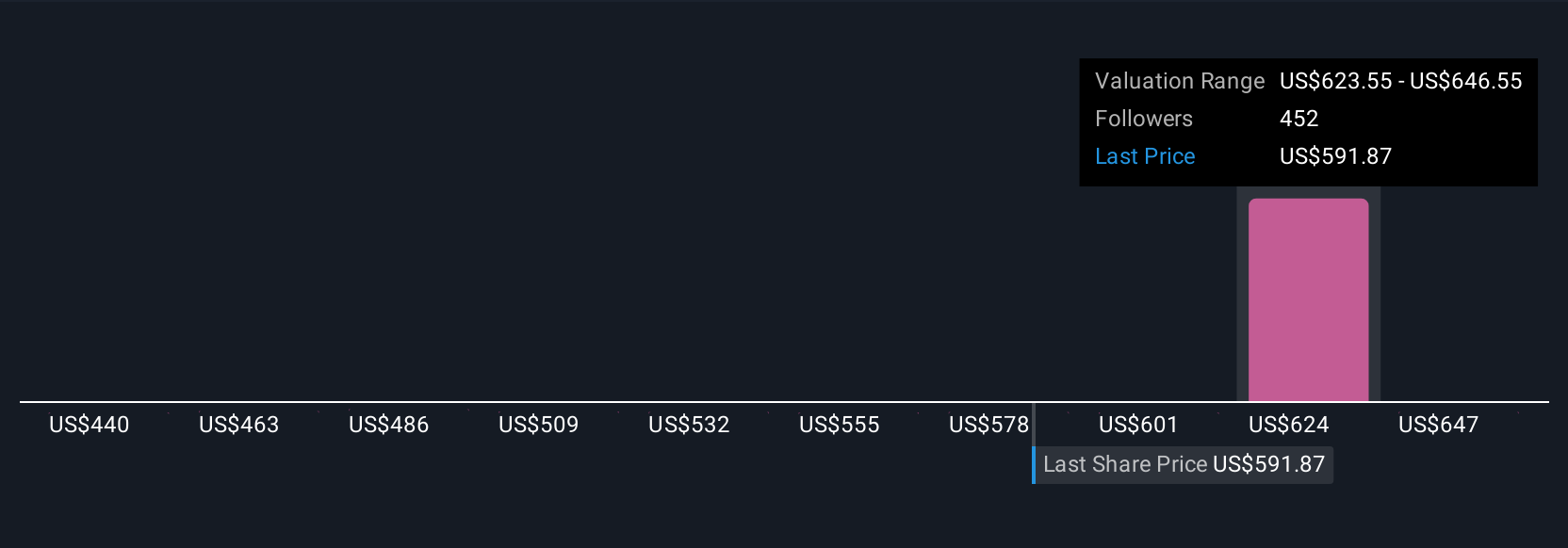

Uncover how Mastercard's forecasts yield a $656.51 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Fifteen fair value opinions from the Simply Wall St Community range from US$512.30 to US$656.51 per share, signaling widely varying expectations for Mastercard’s future. While you review these views, remember that rapid adoption of alternative payment systems in emerging markets could reshape Mastercard’s growth story and is important to watch.

Explore 15 other fair value estimates on Mastercard - why the stock might be worth 6% less than the current price!

Build Your Own Mastercard Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Mastercard research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Mastercard research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mastercard's overall financial health at a glance.

No Opportunity In Mastercard?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MA

Mastercard

A technology company, provides transaction processing and other payment-related products and services in the United States and internationally.

Solid track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

92 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative