Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:LAZ

Is Lazard Still Attractive After a 77.4% Three Year Surge?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Lazard is still a smart buy at today’s price or if you have already missed the opportunity, you are not alone. This stock attracts investors who care about value just as much as growth.

- After a strong run, Lazard now trades around $54.75, with the share price up 8.4% over the last week and month, 7.9% year to date, and delivering a 77.4% gain over three years.

- Recent moves have been shaped by a steady drumbeat of deal activity across M&A and restructuring, which tends to put advisory names like Lazard back on investors’ radars when confidence in capital markets improves. In addition, Lazard has been in the headlines for sharpening its strategic focus and cost discipline, signaling to the market that it wants to be leaner and more profitable through the cycle.

- On our checks, Lazard scores a solid 5/6 valuation score, indicating it looks undervalued on most of the metrics that matter. However, headline multiples rarely tell the full story, so we will walk through the key valuation approaches next and finish with a broader way to think about what this stock might be worth.

Find out why Lazard's 0.7% return over the last year is lagging behind its peers.

Approach 1: Lazard Excess Returns Analysis

The Excess Returns model looks at how much value Lazard can create above the basic return that shareholders require. Instead of focusing only on earnings multiples, it measures whether the firm is consistently earning more on its equity than its cost of equity, and how that value compounds over time.

For Lazard, book value is about $8.87 per share, while stable earnings are estimated at $5.02 per share, based on its median return on equity over the past 5 years. With a cost of equity of roughly $1.25 per share, the model suggests Lazard is generating excess returns of around $3.78 per share, supported by an average return on equity of 37.56%. Analysts in this framework also project stable book value rising toward about $13.37 per share over the long term.

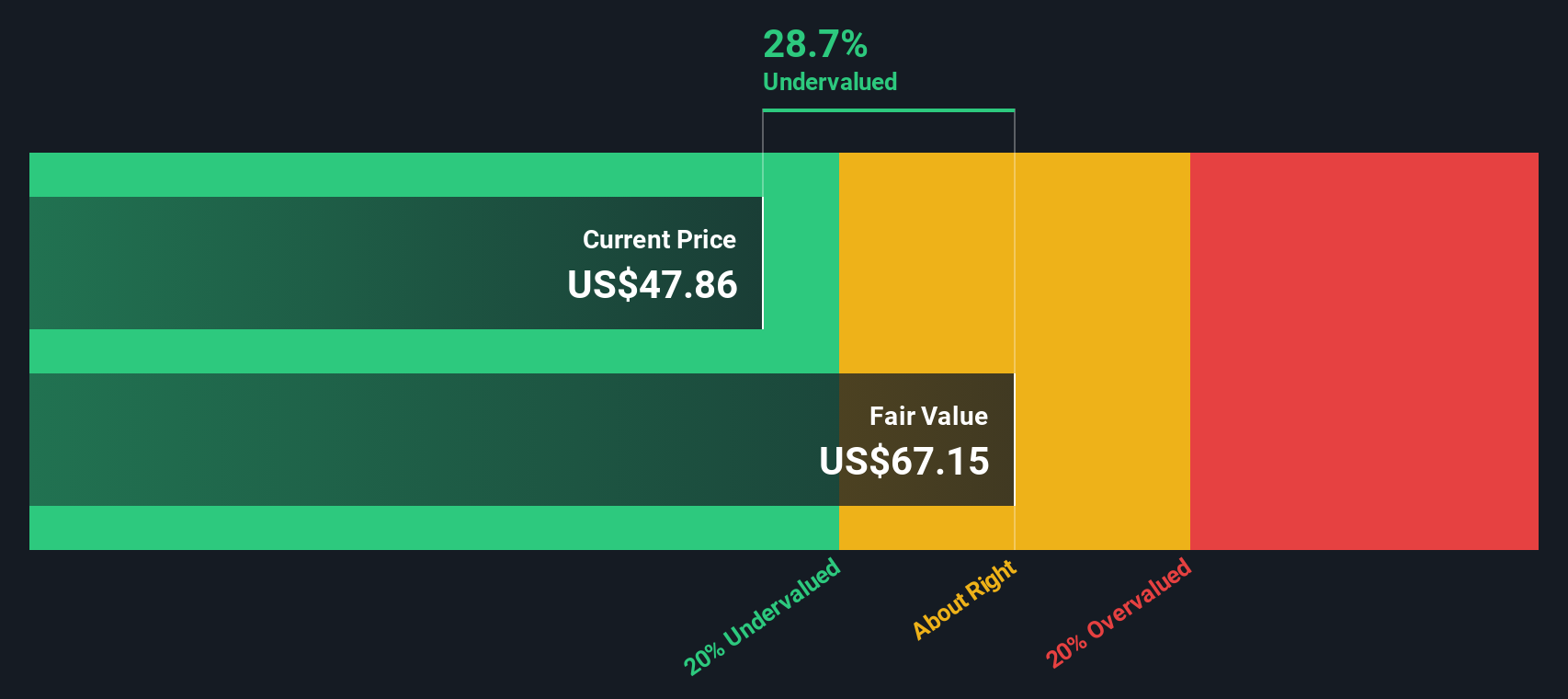

When these excess returns are projected forward, the model arrives at an intrinsic value of about $75.69 per share. Compared with the current price around $54.75, that indicates roughly a 27.7% discount, suggesting the market may not be fully pricing in Lazard’s ability to earn above its cost of equity.

Result: UNDERVALUED

Our Excess Returns analysis suggests Lazard is undervalued by 27.7%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

Approach 2: Lazard Price vs Earnings

For profitable, established businesses like Lazard, the price to earnings multiple is a useful shorthand for how much investors are willing to pay for each dollar of current earnings. It captures not only the company’s profitability today, but also the market’s expectations for how those earnings might evolve.

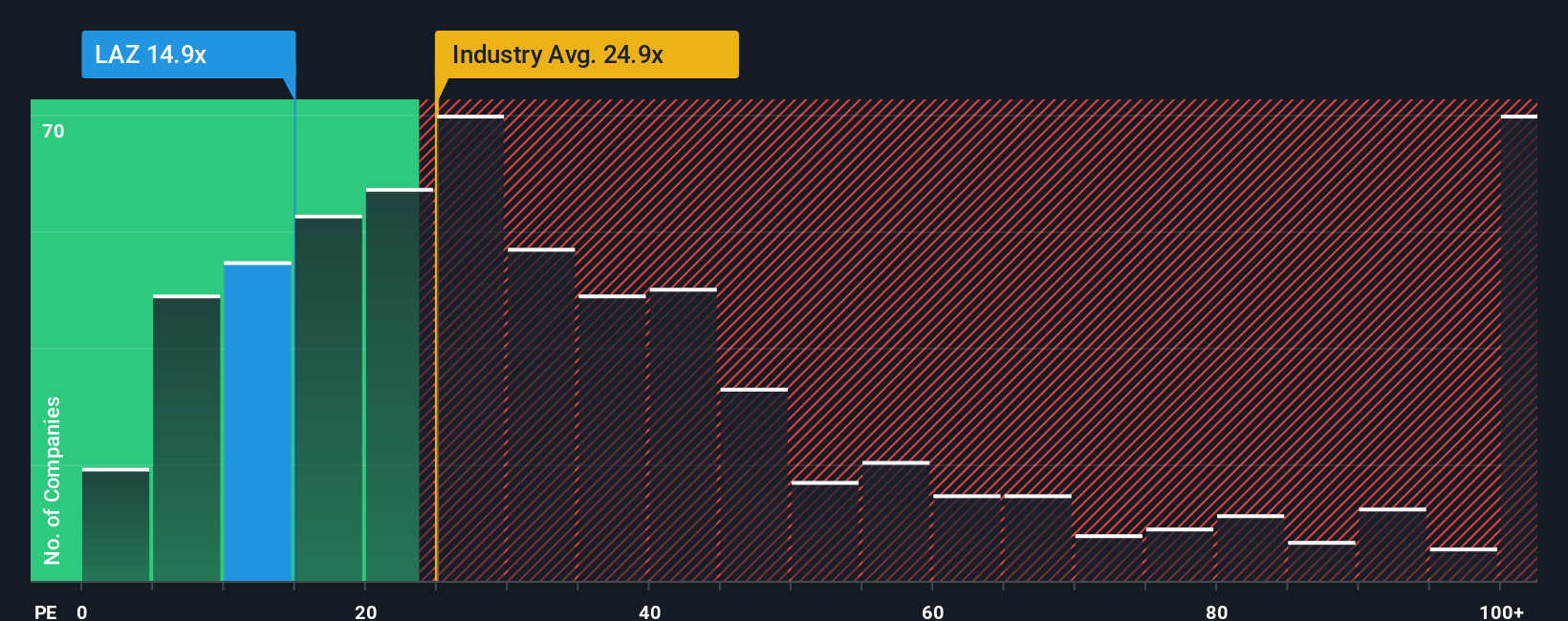

In practice, a higher growth outlook and lower perceived risk usually support a higher normal or fair PE ratio. Slower growth or higher cyclicality, by contrast, tend to justify a lower one. Lazard currently trades on a PE of about 19.5x, which sits below both the Capital Markets industry average of roughly 24.3x and the peer group average of around 25.6x. On those simple comparisons, the stock does not look expensive.

Simply Wall St’s Fair Ratio framework refines this view by estimating what PE multiple Lazard should trade on, given its earnings growth profile, margins, industry, market cap and risk factors. For Lazard, the Fair Ratio is around 19.9x, only slightly above the current 19.5x. Because this approach is tailored to the company rather than broad peer groups, it is a more targeted way to gauge value. It suggests the shares are roughly in line with what the fundamentals justify at present.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1452 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Lazard Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Lazard’s future with a concrete forecast and fair value. A Narrative is your story behind the numbers, where you spell out what you expect for Lazard’s revenue, earnings and margins, and then see how those assumptions translate into a fair value per share. On Simply Wall St’s Community page, used by millions of investors, Narratives turn this story into a living model that compares your Fair Value to today’s Price, helping you decide whether Lazard looks like a buy, a hold or a sell. They also update automatically as new information, such as earnings or news about buybacks and new offices, comes in so your view stays current without extra work. For Lazard, one investor might build a more cautious Narrative that sees fair value closer to the lower analyst target of about $52, while another might lean into the expansion story and land nearer the top of the range around $65, and both perspectives are made explicit and testable through their Narratives.

Do you think there's more to the story for Lazard? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LAZ

Lazard

Operates as a financial advisory and asset management firm in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Undervalued with high growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative