Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:KKR

Is There Still Upside in KKR After Its Strong Multi Year Share Price Run?

Simply Wall St

Reviewed by Bailey Pemberton

- Investors may be wondering whether KKR remains a smart buy after its large multi year run, or if most of the upside is already reflected in the price. In this article we are going to examine what the current share price really implies.

- After a rough patch this year, with the stock down about 13.3% year to date and 17.6% over the past year, KKR has recently bounced 5.8% in the last week and 8.9% over the last month from a recent close near $129.42.

- Those swings sit on top of a substantial 3 year gain of roughly 175.9% and a 5 year return of about 241.3%. This reflects how investors have steadily re rated alternative asset managers such as KKR as private markets have expanded. More recently, shifting expectations for interest rates, deal activity, and fundraising across private equity and credit have helped drive the latest moves as investors reassess where KKR fits within that landscape.

- Right now KKR only scores a 1/6 valuation check score, which might surprise anyone who views it as a long term compounder. Next, we walk through what different valuation approaches suggest about that score and introduce a potentially better way to evaluate KKR's value that we will return to at the end of the article.

KKR scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: KKR Excess Returns Analysis

The Excess Returns model looks at how much profit KKR can generate above the return that equity investors reasonably demand, and then capitalizes those excess profits into an intrinsic value per share.

For KKR, the starting point is a Book Value of $30.54 per share and a Stable EPS estimate of $5.46 per share, based on weighted future return on equity forecasts from six analysts. The model assumes a Cost of Equity of $4.59 per share. On this basis, KKR is expected to generate an Excess Return of about $0.87 per share each year. That equates to an Average Return on Equity of 11.16%, applied to a Stable Book Value projected to rise to $48.89 per share, based on estimates from two analysts.

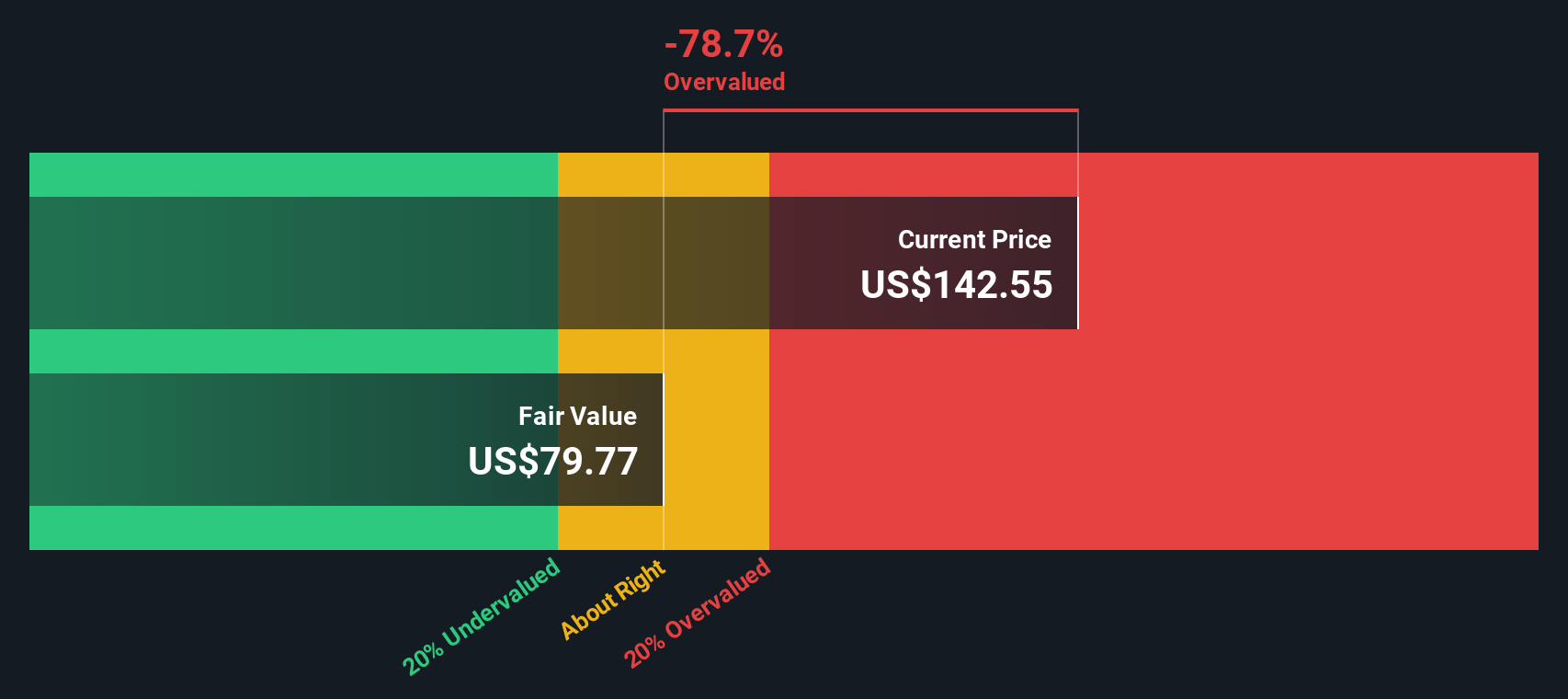

Rolling these inputs together, the Excess Returns valuation implies an intrinsic value of about $63.01 per share. Compared with the recent price near $129.42, the model output indicates that KKR is roughly 105.4% overvalued, so very little margin of safety appears to be present at current levels.

Result: OVERVALUED

Our Excess Returns analysis suggests KKR may be overvalued by 105.4%. Discover 905 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: KKR Price vs Earnings

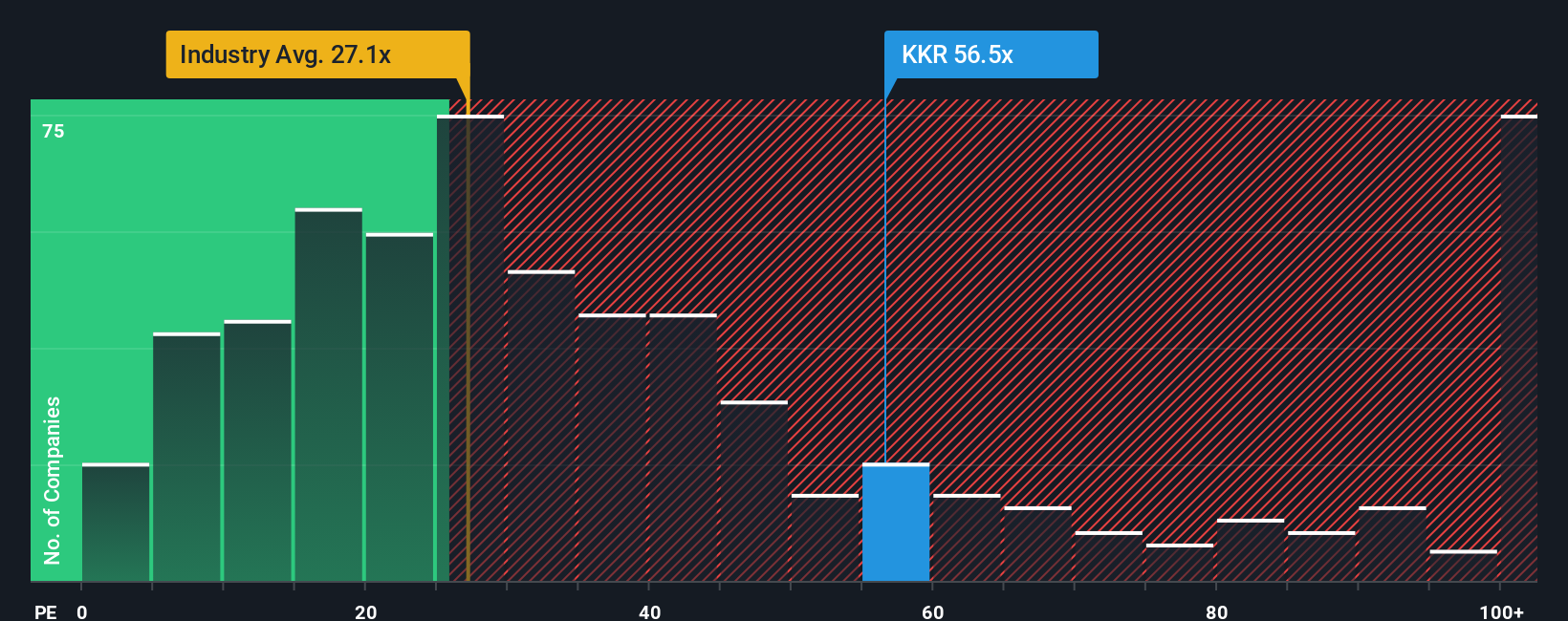

For profitable businesses like KKR, the price to earnings ratio is a useful yardstick because it directly links what investors pay today with the profits the company is generating. In general, faster earnings growth and lower perceived risk justify a higher PE, while slower growth or higher uncertainty tend to pull a normal or fair PE lower.

KKR currently trades on a PE of about 50.8x, well above both the broader Capital Markets industry average of roughly 24.0x and the peer group average near 36.4x. That premium suggests the market is pricing in strong growth and resilient profitability for years to come.

Simply Wall St’s Fair Ratio framework refines this comparison by estimating what PE would be reasonable for KKR specifically, given its earnings growth outlook, risk profile, margins, industry and size. For KKR, the Fair Ratio is 26.7x, which is notably lower than the current 50.8x. Because this approach adjusts for company specific fundamentals rather than relying only on blunt peer or industry averages, it provides a more tailored benchmark, and on that basis KKR screens as materially overvalued.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your KKR Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page that helps you turn your view of KKR’s business into a financial forecast and a fair value estimate you can actually act on.

A Narrative is your story behind the numbers, where you spell out what you believe about a company’s future revenue, earnings and margins, then link that story to a forecast and, ultimately, to a fair value that you can compare with today’s share price to decide whether to buy, hold or sell.

Because Narratives on Simply Wall St are updated dynamically as new news, earnings and analyst revisions come in, they stay aligned with reality instead of going stale. You can also easily see how changes in assumptions ripple through to fair value.

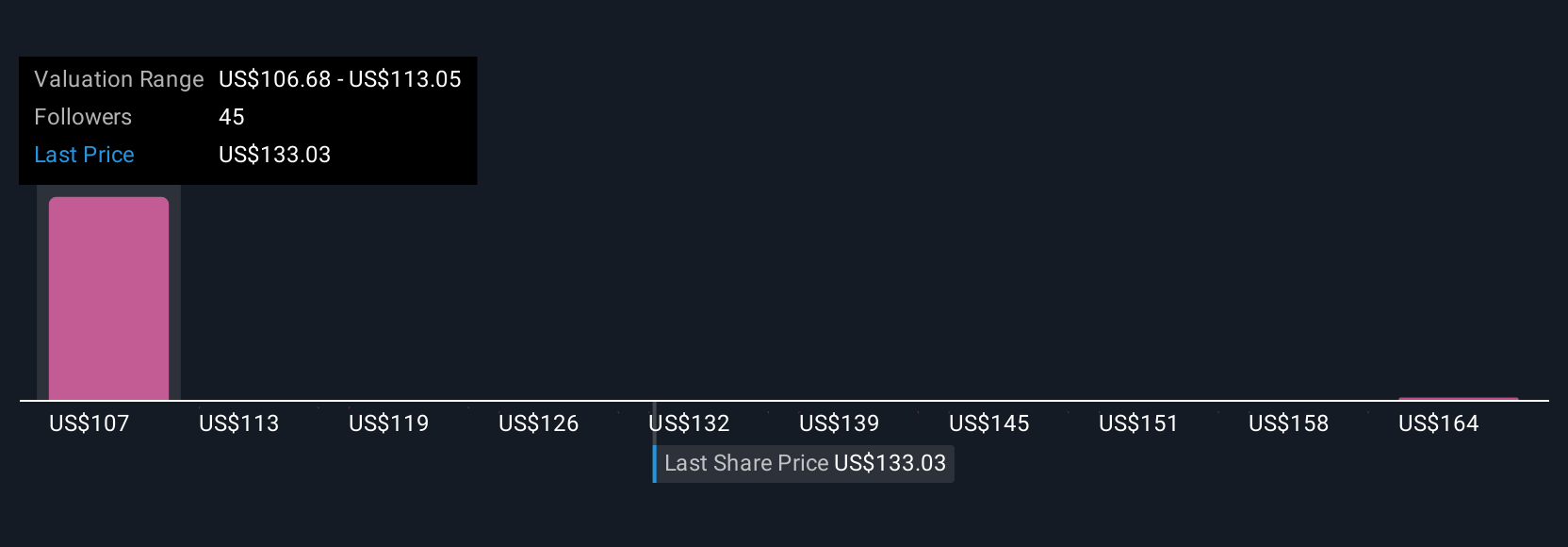

For example, one KKR Narrative might lean bullish and land near the top analyst target of about $187 per share. Another more cautious view could sit closer to the $135 low target, showing how different perspectives on fundraising momentum, margins and market risks can justify very different but still coherent fair values for the same stock.

Do you think there's more to the story for KKR? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KKR might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KKR

KKR

A private equity and real estate investment firm specializing in direct and fund of fund investments.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.70.8% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative