Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:AXP

Is Rising Gen-Z and Millennial Demand Reshaping the Investment Case for American Express (AXP)?

Simply Wall St

Reviewed by Sasha Jovanovic

- American Express recently reported strong third quarter results, supported by robust premium cardholder spending, a successful Platinum card refresh, and resilient credit performance, and raised its revenue and earnings guidance.

- An interesting element is that growth was significantly driven by Gen-Z and Millennial customers, highlighting the company's increasing appeal with younger cohorts and supporting long-term growth potential.

- We'll explore how the strength in premium customer spending and Platinum refresh impacts American Express's broader investment outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

American Express Investment Narrative Recap

To be a shareholder in American Express, you need to believe the company can sustainably outperform through a focus on premium customers, innovative card products, and successful engagement with younger generations, especially as premium spending, younger cohort growth, and the Platinum refresh appear to be the biggest catalysts this year. Recent results were strong and the guidance increase is supportive, but the risk from rising competition and shifting consumer payment preferences remains material and unchanged in the near term.

Among the latest announcements, American Express’s Platinum Card enhancements, with elevated benefits and a limited-edition design, directly tie into the company’s product refresh catalyst and its aim to drive deeper premium card member engagement. These upgrades seem intended to reinforce differentiation in a crowded segment, positioning the Platinum offering as a key contributor to the growth highlighted in the latest earnings update.

By contrast, investors should be aware that... even with strong recent numbers, a downturn in premium consumer spending could pose a significant risk to future growth.

Read the full narrative on American Express (it's free!)

American Express is projected to reach $85.7 billion in revenue and $13.5 billion in earnings by 2028. Achieving this outlook would require annual revenue growth of 10.6% and an earnings increase of $3.5 billion from the current earnings of $10.0 billion.

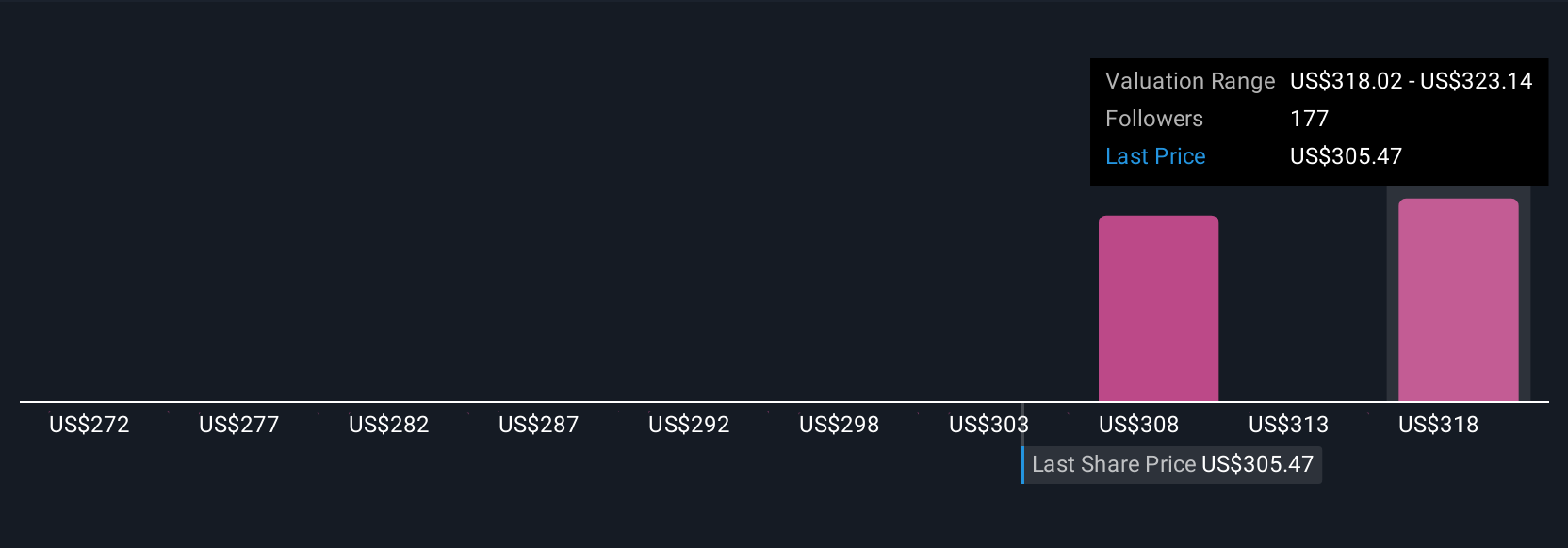

Uncover how American Express' forecasts yield a $350.87 fair value, a 4% downside to its current price.

Exploring Other Perspectives

While recent news has been positive, the least optimistic analysts previously assumed revenue would grow just 9.0% a year and forecast profit margins narrowing to 15.2%. This more pessimistic narrative centers around risks like decelerating airline and entertainment spending. Your own expectations could be quite different, so it’s worth weighing these varied viewpoints.

Explore 7 other fair value estimates on American Express - why the stock might be worth as much as $366.63!

Build Your Own American Express Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your American Express research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free American Express research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate American Express' overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AXP

American Express

Operates as integrated payments company in the United States, Europe, the Middle East and Africa, the Asia Pacific, Australia, New Zealand, Latin America, Canada, the Caribbean, and Internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative