Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:ARES

Ares Management (ARES): Unpacking Current Valuation After Recent Trading Momentum

Simply Wall St

Reviewed by Simply Wall St

Ares Management (NYSE:ARES) has caught investor interest lately, partly due to recent trading activity and ongoing shifts in the financial sector. Shares have moved quietly, and valuation discussions remain relevant for long-term watchers of the stock.

See our latest analysis for Ares Management.

Ares Management's share price recently climbed to $156.85 after a solid 1.49% gain over the last day and 6.39% over the past week, but it is still down roughly 12% so far this year. Momentum has cooled in the short term. However, the longer view is impressive. With a five-year total shareholder return of 288%, the company has handsomely rewarded patient investors even as the current environment adds some caution to the outlook.

If you’re exploring for your next big opportunity, now is the perfect moment to broaden your horizons and discover fast growing stocks with high insider ownership.

Given Ares Management’s recent performance and strong multi-year returns, the key question emerges: is the current share price an opportunity for investors to capitalize on undervaluation, or is the market already factoring in the company’s future growth potential?

Most Popular Narrative: 14.7% Undervalued

Compared to the last close price of $156.85, the most widely followed narrative places Ares Management’s fair value at $183.94, highlighting a substantial gap that is fueling fresh interest in the stock’s true upside.

Robust international fundraising, particularly in Europe and Asia-Pacific, and ongoing success in deepening distribution partnerships are broadening Ares' addressable markets, increasing global deal flow, and positioning the company for sustained earnings growth. The significant ramp in perpetual capital (now nearly 50% of fee-paying AUM), combined with consistent investment performance and low client redemptions, is expected to drive higher recurring fee revenues, greater profitability, and improved earnings visibility.

Big future numbers. Bullish forecasts. But what is really driving the optimism? The narrative hinges on bold assumptions for growth, margins, and a premium earnings multiple rarely seen outside of tech giants. Dive in to explore the details behind that fair value.

Result: Fair Value of $183.94 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, intensifying competition or increased redemptions from retail and wealth channels could quickly challenge assumptions and undermine the bullish expectations for Ares.

Find out about the key risks to this Ares Management narrative.

Another View: Multiples Suggest a Different Story

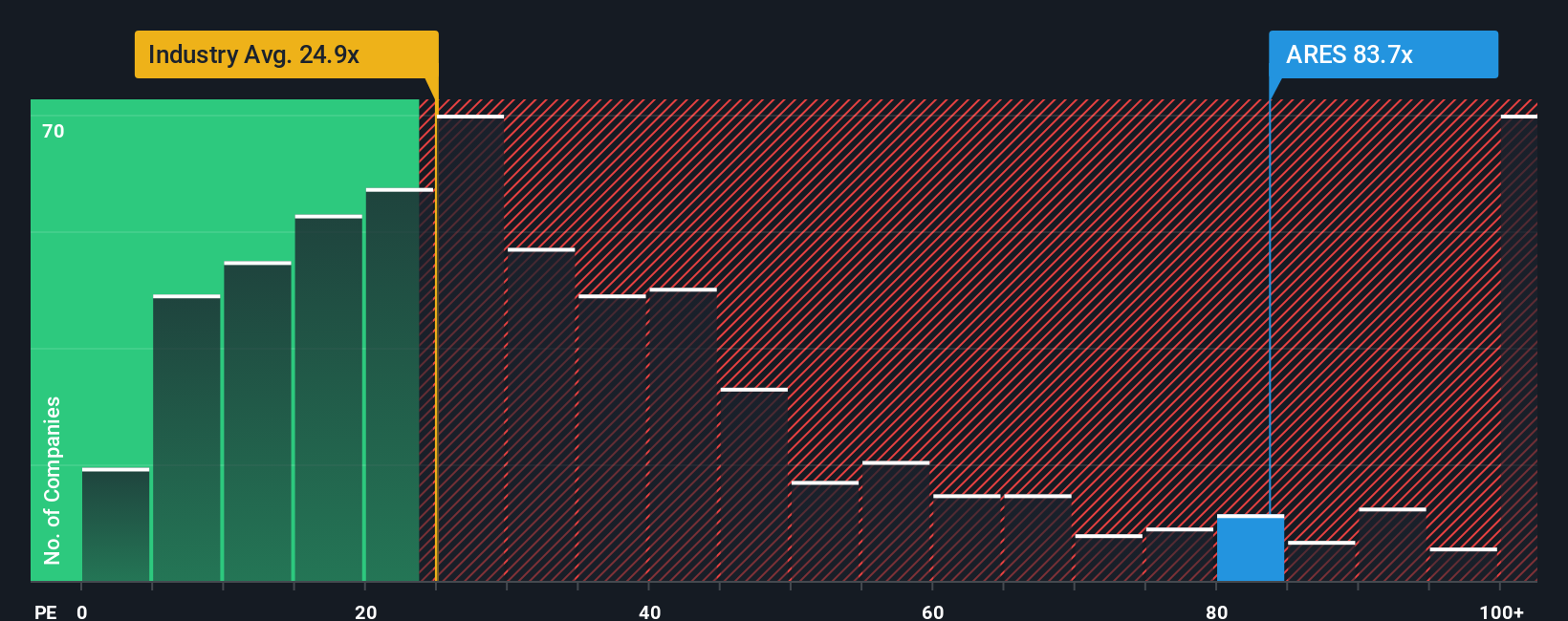

Looking at valuation through the lens of price-to-earnings, Ares Management appears a lot more expensive. Its P/E ratio stands at 67.5x, well above both the industry average of 23.6x and the peer average of 13.5x, and far higher than the fair ratio of 23.2x. This wide gap suggests that, despite growth optimism, there is significant valuation risk if the market adjusts toward more typical levels. The question remains whether future performance will justify such a premium or if the company could face a reality check.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Ares Management Narrative

If the current outlook does not quite match your perspective, or if you would prefer to explore the details on your own terms, you can have your personalized view in just minutes: Do it your way.

A great starting point for your Ares Management research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Seize the moment and find your next winning stock by tapping into unique opportunities others might miss. Don’t let potential breakthroughs and strong performers pass you by. Use the screener to uncover smart investment moves waiting for you today.

- Capture the growth potential in cutting-edge medicine with these 30 healthcare AI stocks, where companies use AI to transform patient care, diagnostics, and drug discovery.

- Unlock high-yield potential by reviewing these 15 dividend stocks with yields > 3% featuring robust businesses consistently rewarding shareholders with strong dividends above 3%.

- Ride the momentum in innovation by targeting these 25 AI penny stocks that are leading advancements across artificial intelligence, automation, and smart data solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ARES

Ares Management

Operates as an alternative asset manager in the United States, Europe, and Asia.

High growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative