Advertisement

- United States

- /

- Capital Markets

- /

- NasdaqGS:MORN

Morningstar (MORN): Rethinking Valuation After CRSP Acquisition and New Index Launches in Benchmarking Expansion

Simply Wall St

Reviewed by Simply Wall St

Morningstar is making strategic moves to solidify its presence in the benchmarking space with the acquisition of the Center for Research in Security Prices and the launch of new indexes designed for semiliquid and evergreen funds.

See our latest analysis for Morningstar.

Morningstar’s big moves in benchmarking and new product launches come right after a busy stretch that included new buyback authorizations, a major credit facility, and solid revenue growth. However, despite the buzz, the share price has tumbled, with a year-to-date share price return of -35.45% and a one-year total shareholder return of -38.4%. This reflects fading investor confidence in the near term even as the company makes strategic bets for the long run.

If Morningstar’s drive for innovation has you thinking bigger, now is a great moment to broaden your search and discover fast growing stocks with high insider ownership

So with Morningstar shares trading at a steep discount to analyst targets and the company rolling out industry-shaping benchmarks, is this the kind of reset that sets up a buying opportunity, or is the market already pricing in all future growth?

Price-to-Earnings of 23.5x: Is it justified?

Morningstar’s current share price implies a price-to-earnings (P/E) ratio of 23.5 times earnings, a level that looks modest relative to both its U.S. capital markets peers and the broader industry average.

The price-to-earnings ratio measures how much investors are willing to pay for each dollar of company earnings, providing a useful temperature check on growth expectations and market sentiment. For a data and analytics leader like Morningstar, it reflects investor views on earnings resilience, repeat business, and industry position.

Morningstar’s P/E of 23.5x is below the peer group average of 27.8x and slightly under the U.S. capital markets industry average of 24x. This discount suggests the market may not be fully recognizing Morningstar’s profit growth or outlook, especially for a company with a history of double-digit earnings expansion and robust return on equity. However, compared to an estimated fair P/E ratio of 14.1x, shares look relatively expensive, which could be tested if growth slows or sentiment fades.

Explore the SWS fair ratio for Morningstar

Result: Price-to-Earnings of 23.5x (ABOUT RIGHT)

However, slowing revenue growth or market skepticism about Morningstar’s long-term earnings power could limit further upside, even as the company pursues recent strategic moves.

Find out about the key risks to this Morningstar narrative.

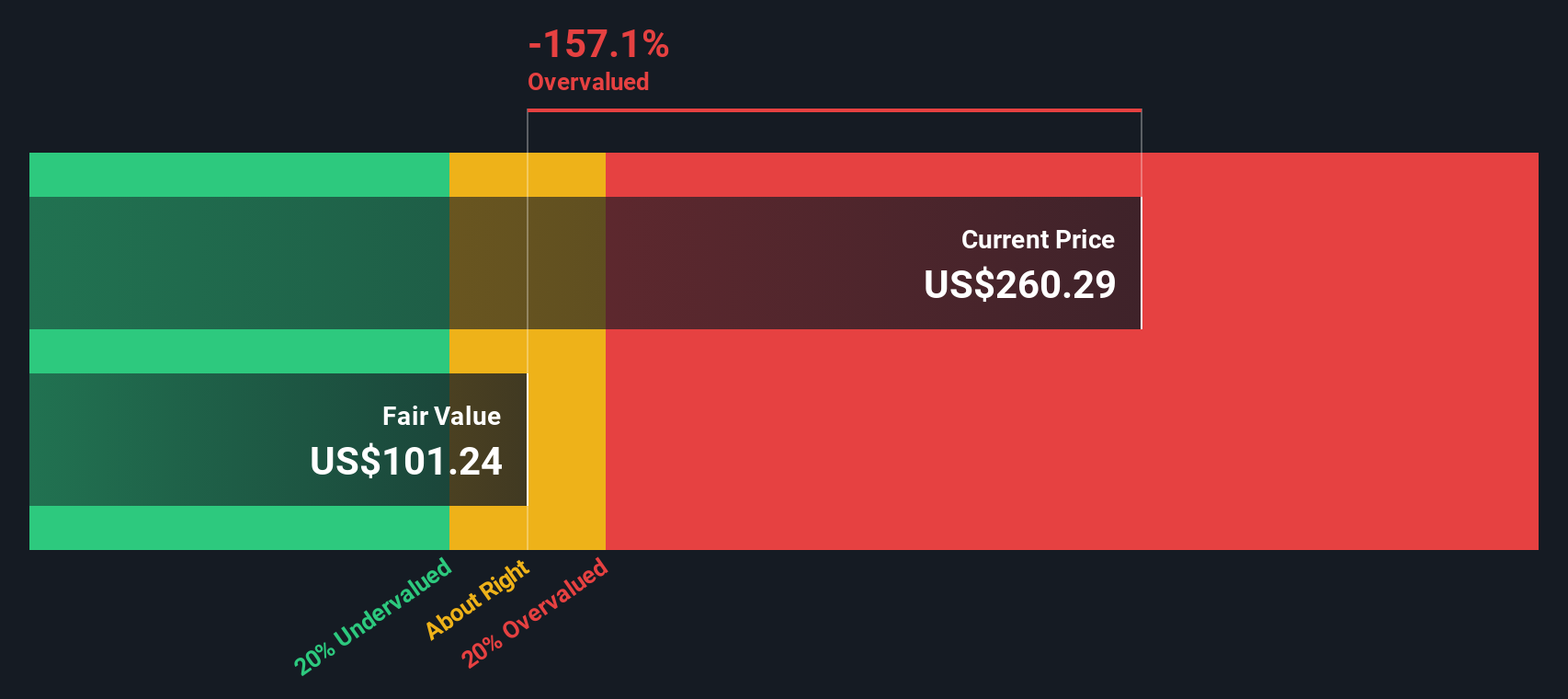

Another View: The SWS DCF Model

While the price-to-earnings approach suggests Morningstar is fairly valued compared to peers, our DCF model paints a very different picture. According to the SWS DCF model, Morningstar’s shares are currently trading well above their estimated fair value. If the market adjusts toward this lower value, how much downside risk could investors face?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Morningstar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 855 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Morningstar Narrative

If you see the story differently or think a better investment argument can be made, you can easily craft your own narrative in just minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Morningstar.

Looking for more investment ideas?

Why limit your ambitions to just one stock when opportunities are everywhere? Uncover smart ways to strengthen your portfolio by using these focused investment lists below. Act now and stay a step ahead of the crowd.

- Earn passive income and unlock reliable potential by tapping into these 15 dividend stocks with yields > 3% offering attractive yields above 3%.

- Capitalize on groundbreaking medical innovation and changing healthcare trends through these 32 healthcare AI stocks at the forefront of AI-powered patient care.

- Ride the next tech revolution by targeting these 25 AI penny stocks driving artificial intelligence breakthroughs with rapid growth prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MORN

Morningstar

Provides independent investment insights in the United States, Asia, Australia, Canada, Continental Europe, the United Kingdom, and internationally.

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor