Advertisement

- United States

- /

- Hospitality

- /

- OTCPK:LKNC.Y

Is Luckin Coffee’s Recent Expansion News Justifying Its Current Valuation in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if Luckin Coffee is worth your attention right now? You are not alone. Plenty of investors are eyeing the stock’s dramatic run and wondering if the price still makes sense.

- The stock may have dipped slightly over the last week and month, down 1.8% and 11.1% respectively. Its year-to-date gain of 35% and an 820% return over five years are noteworthy.

- Recent headlines have spotlighted Luckin Coffee’s expansion strategies and partnerships, fueling market speculation. Coverage of the company’s rapid store growth and notable deals in China has helped keep investor sentiment upbeat despite occasional price volatility.

- On Simply Wall St valuation checks, Luckin Coffee scores a 4 out of 6, signaling some pockets of undervaluation. This score reflects how traditional metrics stack up, and can be a useful starting point for judging whether Luckin Coffee truly offers value.

Approach 1: Luckin Coffee Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s value. For Luckin Coffee, this involves analyzing the money it generates, forecasting potential growth in those figures, and calculating what those future profits are worth in present terms.

According to the latest data, Luckin Coffee generated trailing twelve-month Free Cash Flow (FCF) of roughly CN¥4.39 billion. Analysts have provided estimates for the next several years, with projected FCF reaching about CN¥4.52 billion by 2027. Beyond 2027, forecasts are extrapolated by Simply Wall St, with FCF potentially surpassing CN¥5.39 billion by 2035.

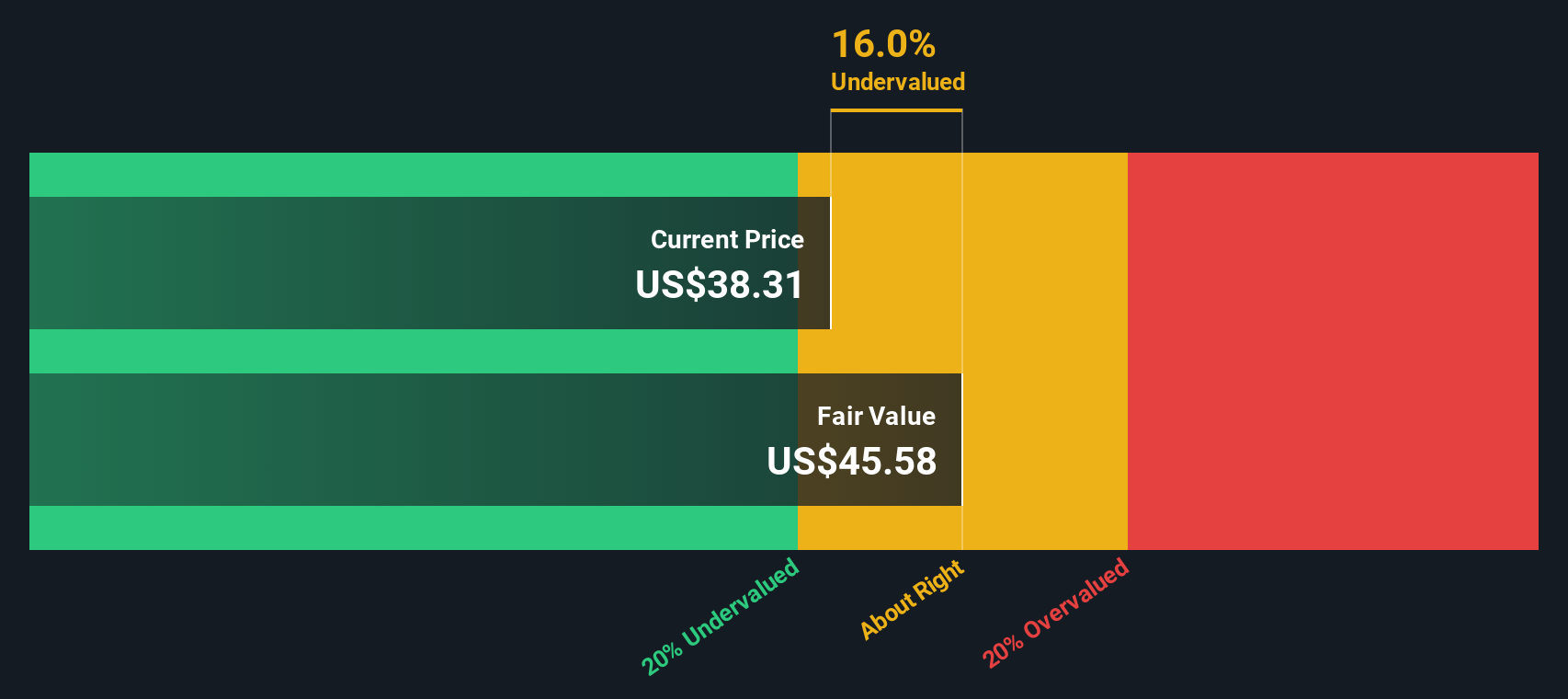

Based on these estimates and the 2 Stage Free Cash Flow to Equity model, the DCF calculation places the company’s intrinsic value at $29.98 per share. The DCF model currently indicates the stock is trading at a 21.2% premium to its intrinsic value, suggesting that Luckin Coffee appears overvalued at present levels.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Luckin Coffee may be overvalued by 21.2%. Discover 926 undervalued stocks or create your own screener to find better value opportunities.

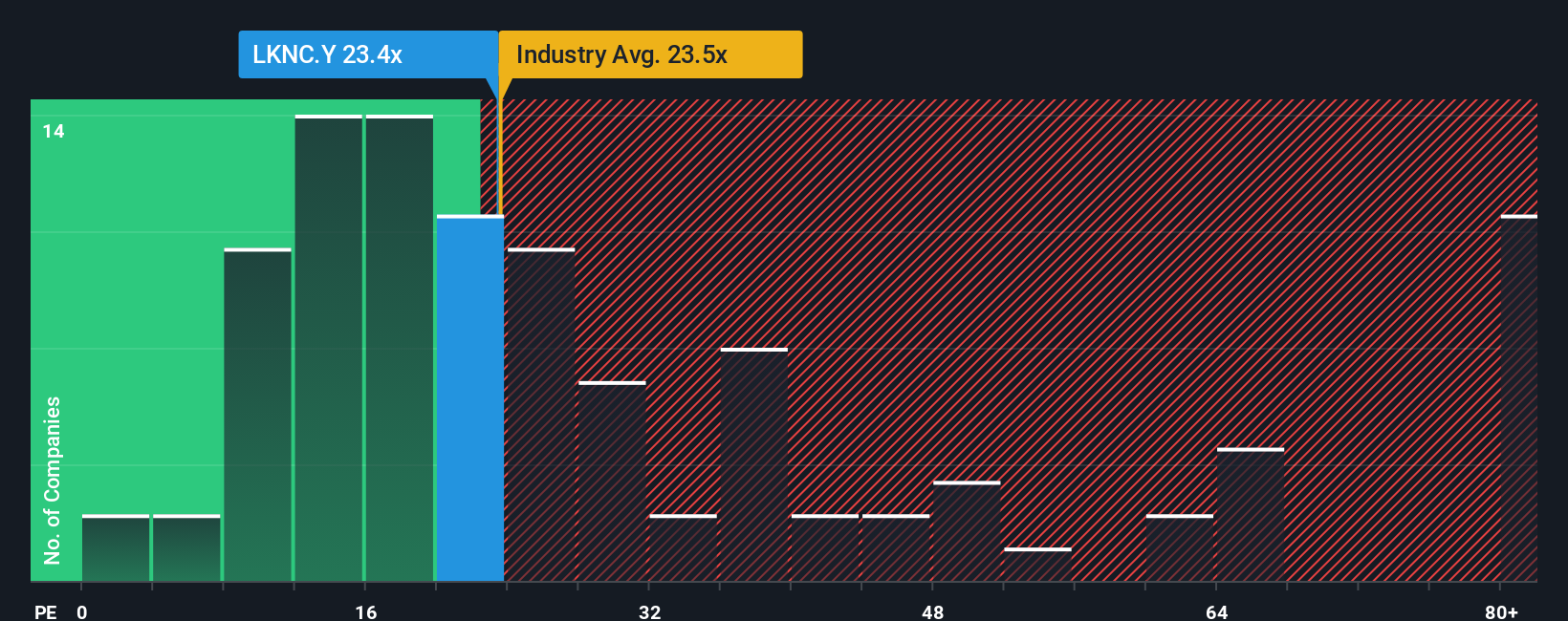

Approach 2: Luckin Coffee Price vs Earnings

For profitable companies like Luckin Coffee, the price-to-earnings (PE) ratio is a widely accepted way to gauge whether a stock is expensive or cheap relative to its profits. The PE ratio works because it directly compares the price investors are willing to pay for a dollar of current earnings, making it simple and effective for evaluating established businesses with positive earnings. However, it is important to remember that a “fair” PE can shift depending on how quickly the company is expected to grow and the level of risk investors perceive. The faster the growth or the lower the risk, the higher the justifiable PE.

Luckin Coffee trades at a PE of 21.1x, which is in line with the hospitality industry average of 21.4x but well below the average for its listed peers at 54.3x. However, a straight comparison with peer and industry averages does not always tell the full story, since such benchmarks can be heavily skewed by outliers or differences in growth prospects and profitability.

That is where Simply Wall St’s proprietary “Fair Ratio” comes in. The Fair Ratio is built to reflect a more holistic measure of where the PE should be, by factoring in not just industry and market cap but also Luckin Coffee’s earnings growth, profit margins and business risks. For Luckin Coffee, the Fair Ratio is calculated to be 28.0x, which is only modestly higher than its current multiple of 21.1x. This indicates that when adjusting for company-specific factors, the current valuation is roughly fair.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Luckin Coffee Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a clear, approachable way for you to attach your personal story and assumptions about a business, such as its fair value, expected revenue growth, and profit margins, to the numbers. This connects what you believe about a company’s future directly to its financial forecasts and valuation. Narratives provide structure beyond formulas, allowing you to link the company’s journey and prospects to a tailor-made fair value that reflects your perspective.

On Simply Wall St’s Community page, Narratives make this process accessible to all investors and update automatically when news or earnings results are released, so your view is always informed by the latest facts. Comparing your Narrative’s fair value to the current price helps you decide whether it’s time to buy, hold, or sell, with transparency around the reasons behind your decision.

For example, some Luckin Coffee Narratives are optimistic, expecting aggressive growth, margin expansion, and a fair value above $48, while others are more cautious, forecasting slower growth and potential pricing pressures, with fair values as low as $32. Narratives help you see these differing perspectives clearly and decide which story fits your investment outlook best.

Do you think there's more to the story for Luckin Coffee? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OTCPK:LKNC.Y

Luckin Coffee

Offers retail services of freshly brewed drinks, and pre-made food and beverage items in the People's Republic of China.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative