Advertisement

- United States

- /

- Hospitality

- /

- NYSE:YUM

Yum! Brands (YUM): Assessing Valuation as Pizza Hut Strategic Review Signals Major Portfolio Shift

Simply Wall St

Reviewed by Simply Wall St

Yum! Brands has begun a formal review of strategic alternatives for its Pizza Hut business following ongoing underperformance in the U.S. This move could reshape the company’s portfolio and has important implications for investors.

See our latest analysis for Yum! Brands.

This decision to review options for Pizza Hut comes following several notable developments, including a third-quarter earnings lift and a new EV charging partnership for multiple U.S. locations. Yum! Brands has delivered a healthy 11% year-to-date share price return, with its total shareholder return reaching over 10% in the past twelve months. This reflects decent long-term momentum as management signals new directions for the business.

If this shake-up has sparked your curiosity, now is the perfect time to see what else is trending. Discover fast growing stocks with high insider ownership.

With the Pizza Hut review now underway and solid overall momentum across the rest of the company, the big question is whether Yum! Brands’ current share price accurately reflects these changes or if a buying opportunity is emerging for investors seeking growth.

Most Popular Narrative: 8.1% Undervalued

With the most popular narrative estimating fair value at $161.40 and Yum! Brands last closing at $148.26, this perspective points to room for further value. What is driving this confidence? The answer lies in several forward-looking fundamentals.

The rapid acceleration and global rollout of Yum!'s Byte digital platform, including AI-driven marketing, operational automation, and proprietary ordering and delivery solutions, positions the company to capture higher transaction volumes, expand check sizes, and enhance customer loyalty. This supports both top-line revenue growth and improved net margins over the long term.

What is really powering this premium fair value? Analysts have built their narrative around a blend of resilient earnings, digital transformation, and unexpectedly bold assumptions for future profitability. Curious how these projections add up? Do not miss the deep dive to uncover the full financial case behind the target price.

Result: Fair Value of $161.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent choppy sales and slow brand innovation could undermine the upbeat scenario, particularly if consumer demand remains weaker than analysts expect.

Find out about the key risks to this Yum! Brands narrative.

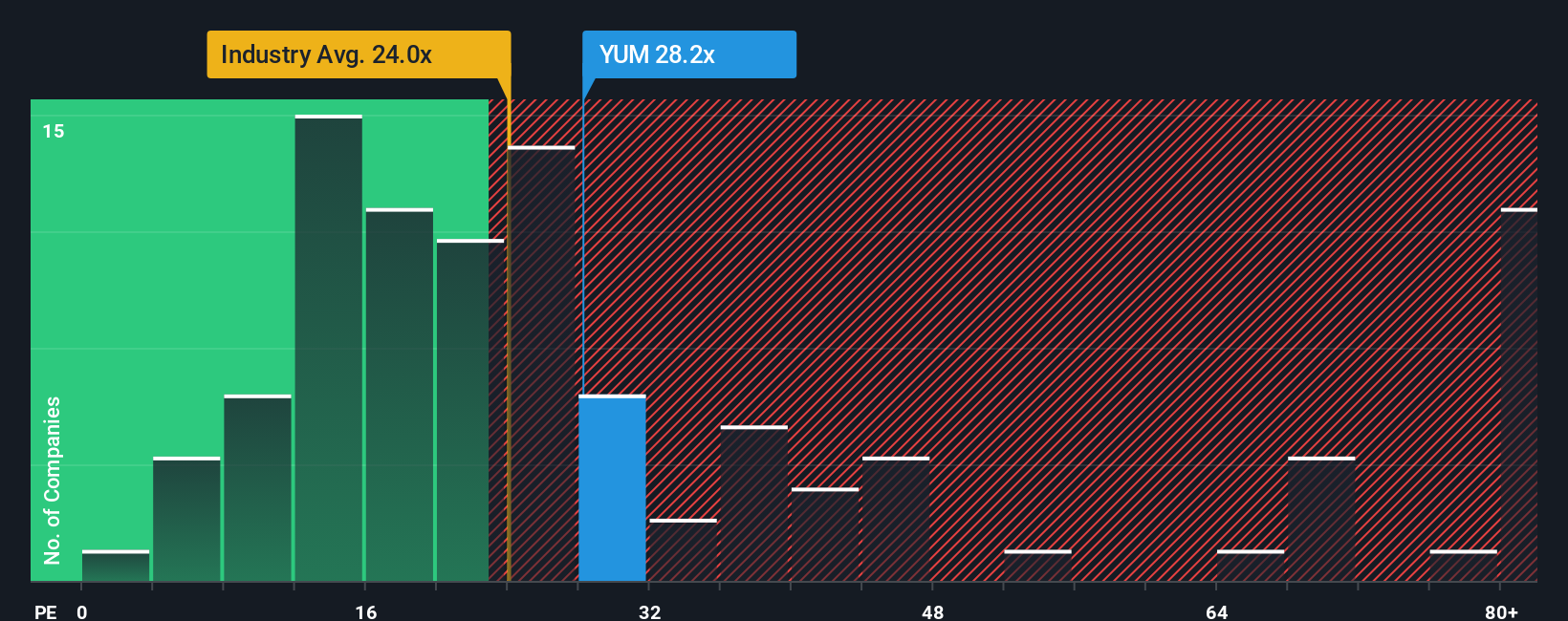

Another View: Multiples Suggest a Premium Valuation

Taking a closer look at valuation based on price-to-earnings, Yum! Brands trades at 28.4x, well above both the industry average of 21.2x and its peer average of 26.4x. The fair ratio suggests the market could drift lower and highlights risk if expectations reset. Is the premium justified by future growth?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Yum! Brands Narrative

If you are keen to see the numbers for yourself or want your own perspective to lead the story, you can shape your own analysis in just a few minutes. Do it your way.

A great starting point for your Yum! Brands research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Step beyond the obvious and get ahead of the market. The Simply Wall Street Screener puts you in control with investment themes that could shape tomorrow’s winners. Take your research further and seize opportunities you won’t want to miss.

- Target reliable growth and income by tapping into these 16 dividend stocks with yields > 3% that consistently deliver high-yield returns above 3%.

- Access a new era of digital disruption by reviewing these 24 AI penny stocks leading advancements in artificial intelligence and transforming global industries.

- Position yourself early by tracking these 82 cryptocurrency and blockchain stocks, where pioneering companies are reshaping finance with blockchain innovation and crypto adoption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:YUM

Yum! Brands

Develops, operates, and franchises quick service restaurants worldwide.

Average dividend payer with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor