Shake Shack (SHAK) shares staged a mild rebound, rising less than 2% after a stretch of declines over the past month. Investors appear to be weighing recent performance trends as the broader fast-casual sector remains competitive.

Shake Shack’s share price has been under pressure this year, with its 2024 drop reflecting cooling sentiment after last year’s gains. While the 3-year total shareholder return is still up over 70%, momentum has faded lately as investors digest both sector-wide and company-specific developments.

But after months of sideways trading and mixed short-term returns, is Shake Shack’s current valuation reflecting real upside for long-term investors? Or has the market already priced in the company’s recent growth and improvement?

Advertisement

Most Popular Narrative: 22.6% Undervalued

With Shake Shack's widely followed narrative setting a fair value well above its latest close, attention is turning to bold growth assumptions and catalyst events that fuel the optimism.

The company's strategic focus on urban expansion and accelerated domestic and international store openings, especially in untapped markets and through new formats such as drive-thru and licensed partnerships (for example, casinos, Panama), directly taps into growing urbanization and demand for experiential fast-casual dining. This supports long-term, system-wide revenue growth.

What is the secret recipe behind this bullish outlook? The narrative relies on aggressive financial targets, ambitious expansion plans, and a premium profit multiple that is usually reserved for high-flying growth stories. Discover which key forecasts and controversial assumptions are driving this striking valuation.

However, rising input costs and continued softness in same-store traffic could still challenge Shake Shack’s growth outlook and disrupt even the most optimistic forecasts.

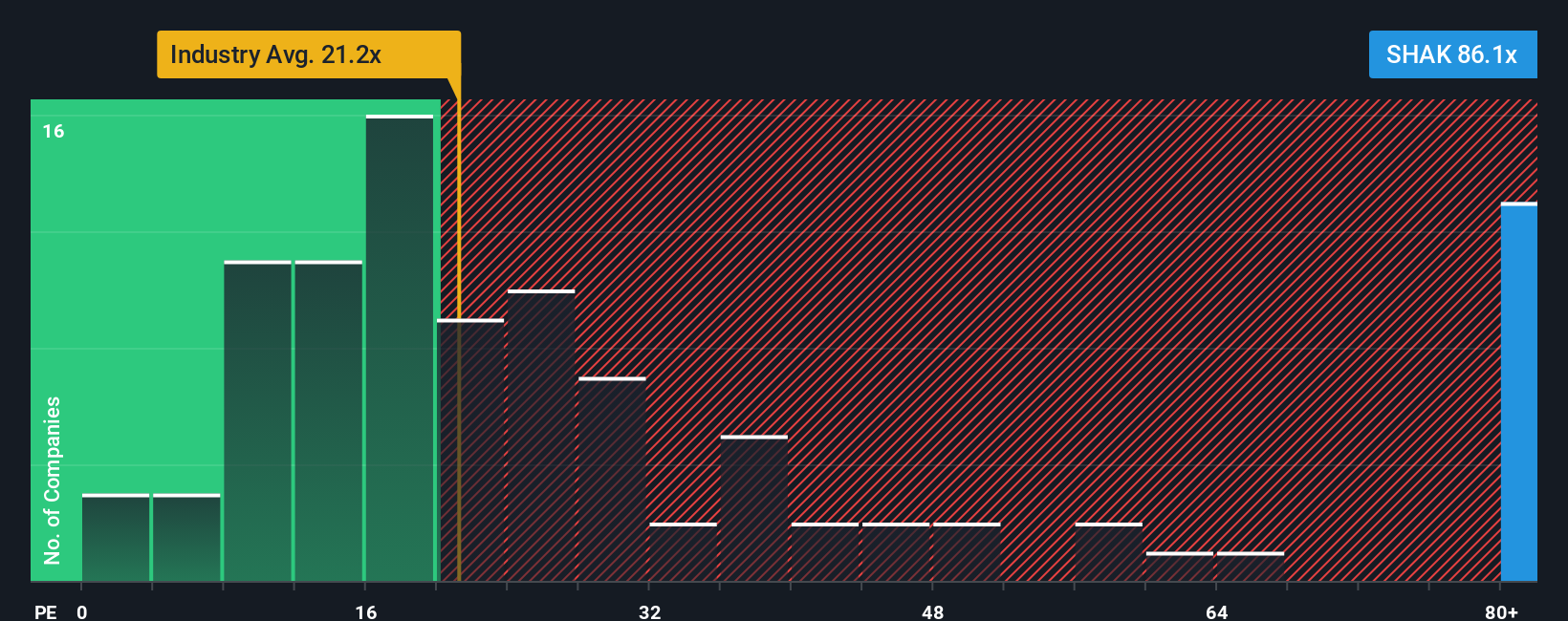

While valuation based on cash flows points to upside, the current price-to-earnings ratio tells a different story. Shake Shack trades at 83.6x earnings, which is far higher than the industry average of 21.4x and the peer average of 22.7x. Even compared to the fair ratio of 27.4x, today's multiple significantly raises the bar for future growth.

If this analysis doesn't quite fit your perspective, or if you're eager to dig into the numbers firsthand, you can build your own in just minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Shake Shack.

Looking for more investment ideas?

Level up your portfolio with fresh opportunities that most investors overlook. The Simply Wall Street Screener helps you act quickly and identify tomorrow’s potential winners.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks