Advertisement

- United States

- /

- Hospitality

- /

- NYSE:QSR

Is There Value in Restaurant Brands International After Drive-Thru Modernization News?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Restaurant Brands International is trading at a bargain or looks overheated? You are not alone; we are diving into what its numbers tell us about value right now.

- The stock is up 2.7% in the last week and has climbed 9.6% over the past month, which suggests shifting sentiment and renewed interest in its growth story.

- Headlines have focused on the company’s bold expansion efforts and ongoing brand revamps. Investors hope these changes could propel future sales. The buzz was fueled by recent announcements about drive-thru modernization and new international partnerships.

- Right now, Restaurant Brands International scores a 2 out of 6 on our undervaluation checks. Let’s break down what this means by looking at a few tried-and-true valuation methods, and stick around for a more nuanced take at the end of the article.

Restaurant Brands International scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Restaurant Brands International Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future cash flows and discounting them back to their present value. This approach attempts to answer the question: how much are Restaurant Brands International’s future profits worth today?

Currently, Restaurant Brands International generates Free Cash Flow (FCF) of about $1.3 Billion. Analyst projections cover several years ahead, forecasting FCF to grow steadily and reach over $2.3 Billion by 2028. Cash flows beyond this time frame are extrapolated with long-term estimates suggesting nearly $3.6 Billion in FCF by 2035, according to Simply Wall St’s model.

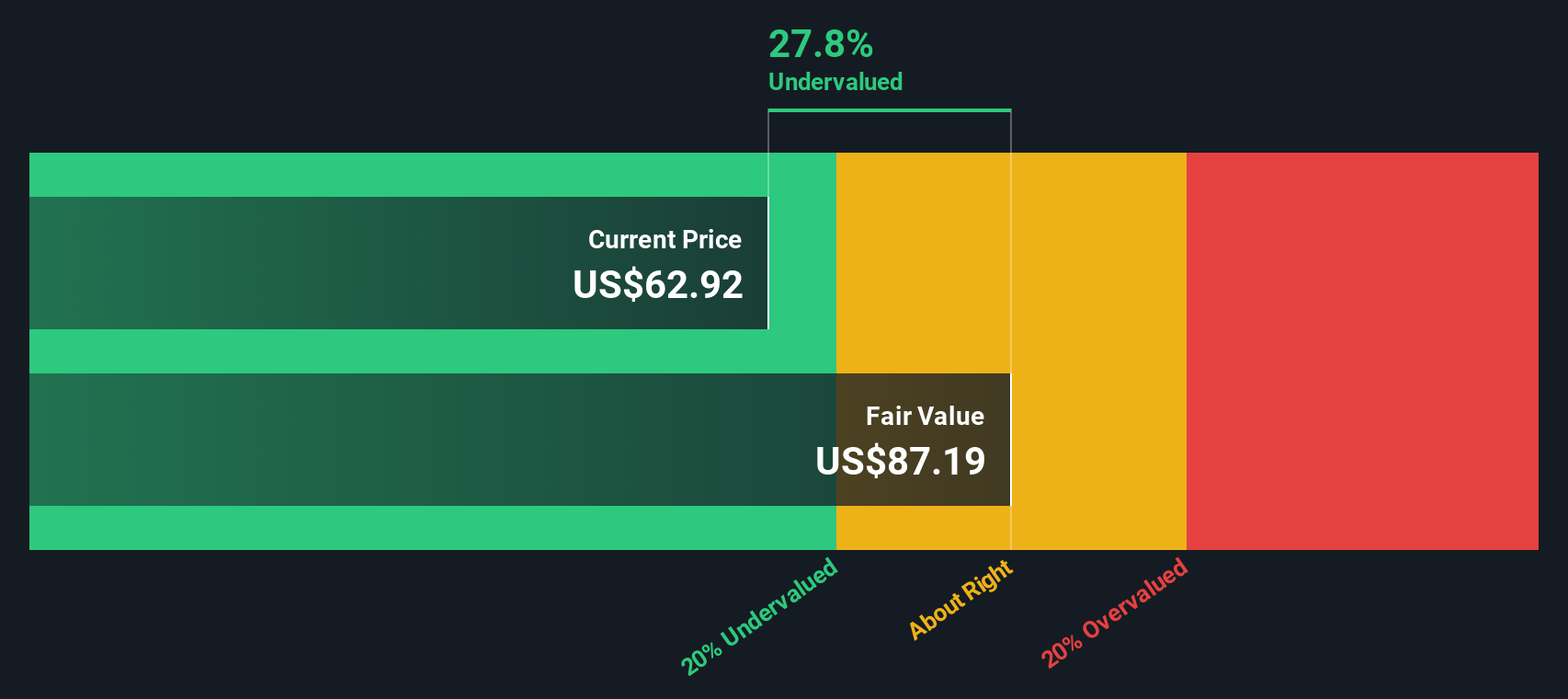

Applying the 2 Stage Free Cash Flow to Equity model, the DCF analysis produces an intrinsic value of $89.13 per share. This is around 18.8% higher than the company’s current share price. This figure indicates that Restaurant Brands International may be undervalued by the market at the moment.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Restaurant Brands International is undervalued by 18.8%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: Restaurant Brands International Price vs Earnings

The Price-to-Earnings (PE) ratio is widely considered the go-to valuation tool for profitable companies like Restaurant Brands International. It offers a quick snapshot of how much investors are willing to pay for each dollar of current earnings, helping to gauge if a stock price reflects realistic growth and profitability expectations.

Determining what qualifies as a “normal” or “fair” PE ratio is not one-size-fits-all. Companies with stronger growth prospects or more stable profit streams typically justify higher PE multiples, while those with greater risks or slower growth often deserve a lower price tag. Market context, sector trends, and company-specific risks all have sway.

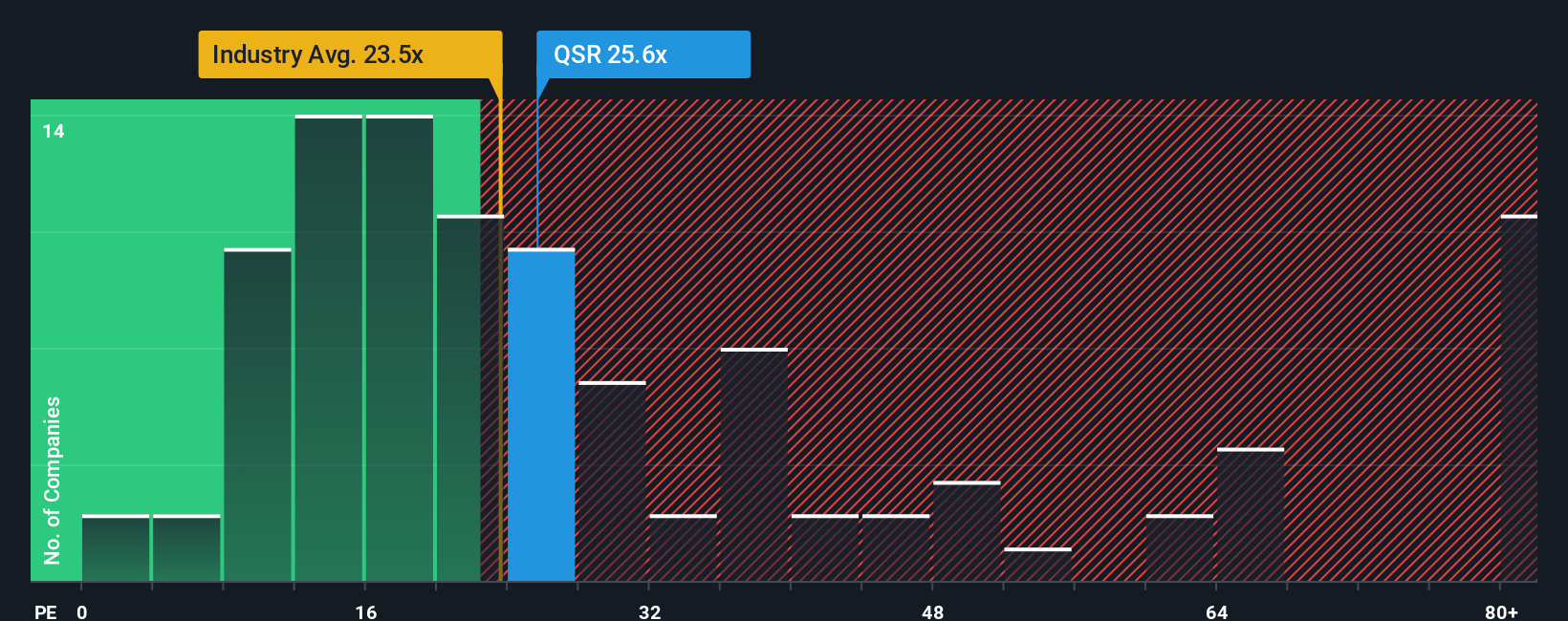

Restaurant Brands International currently trades at a PE ratio of 25.5x. This compares to an industry average PE of 21.4x and a peer group average of 24.3x. This suggests the company trades at a modest premium to its competitors and the hospitality sector as a whole.

Simply Wall St’s “Fair Ratio” adds another layer of insight; for Restaurant Brands International, this proprietary metric is 29.2x. Unlike broad industry or peer benchmarks, the Fair Ratio better incorporates the company’s actual earnings growth, profitability, risk profile, industry category, and market cap, offering a more tailored view of valuation.

With Restaurant Brands International’s actual PE ratio (25.5x) sitting below its Fair Ratio (29.2x), the stock appears undervalued on this metric. This assessment is further supported when adjusting for the company’s distinctive qualities.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Restaurant Brands International Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personalized story about a company, showing how you see its future playing out in numbers based on your views of sales growth, profit margins, risks, and opportunities. Narratives bridge the gap between headlines and hard data, transforming your insights or expectations for Restaurant Brands International into an actionable financial forecast and fair value estimate.

This user-friendly tool is available to everyone on Simply Wall St within the Community page, where millions of investors compare, share, and update their outlooks on companies like Restaurant Brands International. Narratives empower you to make buy or sell decisions by revealing how your calculated Fair Value stacks up against the current Price. The information stays up to date as news, earnings, or new market events arrive, so your story is updated automatically.

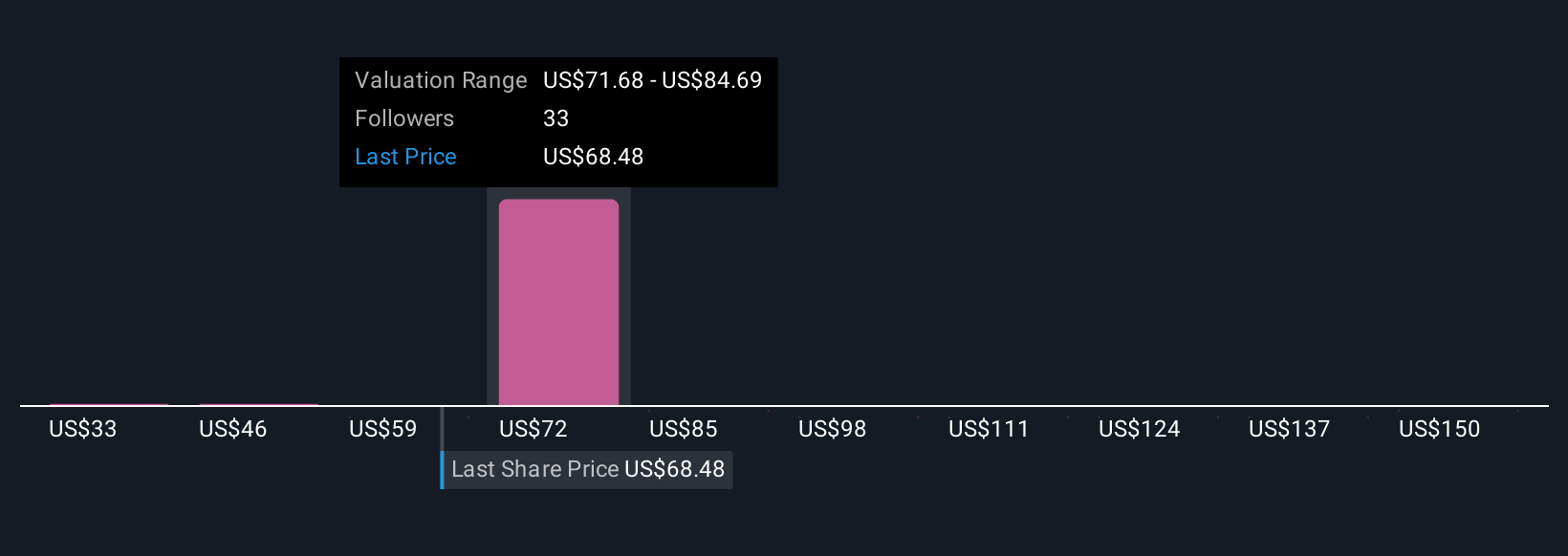

For instance, among current Narratives for Restaurant Brands International, some investors predict major upside from China expansion and see Fair Value above $93 per share, while others remain cautious about global competition and set Fair Value closer to $60. Each viewpoint is backed by unique assumptions, so you can quickly find the scenario that best matches your outlook.

Do you think there's more to the story for Restaurant Brands International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:QSR

Restaurant Brands International

Operates as a quick-service restaurant company in Canada, the United States, and internationally.

Established dividend payer with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative