Advertisement

- United States

- /

- Hospitality

- /

- NYSE:NCLH

Will Simultaneous Cruise Stock Selloff Shift Norwegian’s (NCLH) Record Revenue Investment Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Norwegian Cruise Line Holdings, along with other major cruise operators, saw its shares decline during a broad industry selloff spurred by unclear market concerns.

- This simultaneous movement across multiple cruise stocks reflects underlying uncertainties or sector-wide factors influencing investor sentiment toward cruise line operators.

- With Norwegian reporting record-high quarterly revenues fuelled by strong demand, we'll explore how these mixed signals shape the company's investment narrative moving forward.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Norwegian Cruise Line Holdings Investment Narrative Recap

To own shares in Norwegian Cruise Line Holdings, an investor needs to believe that demand for cruise vacations will remain resilient and that the company's expansion into luxury and experiential travel can deliver ongoing revenue and margin growth. The recent, unexplained sector selloff does not appear to impact the most important short-term catalyst, robust consumer demand and record-high bookings, but it does highlight market sensitivity to industry-wide uncertainty, underscoring that Norwegian’s high debt levels remain a key risk for shareholders.

Most relevant to the recent news is Norwegian's Q3 announcement of all-time high quarterly revenue and a 19% increase in its full-year adjusted EPS guidance, underpinned by unprecedented booking activity and strong onboard spend. This supports the main narrative that occupancy and pricing power are critical drivers and helps offset some risk concerns tied to leverage and cost pressures, at least as long as demand remains healthy.

But on the other side of the story, investors should be mindful of Norwegian’s significant debt obligations and how...

Read the full narrative on Norwegian Cruise Line Holdings (it's free!)

Norwegian Cruise Line Holdings' outlook anticipates $12.6 billion in revenue and $1.7 billion in earnings by 2028. This scenario depends on 9.5% annual revenue growth and a $980.8 million increase in earnings from the current $719.2 million.

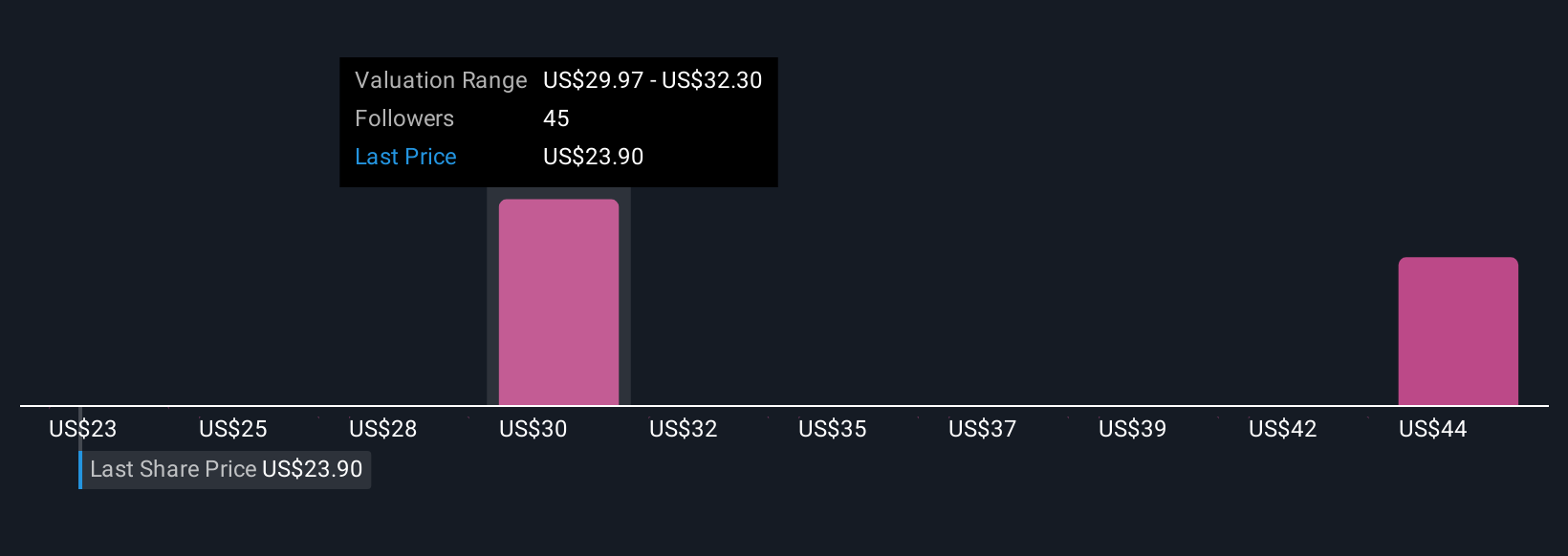

Uncover how Norwegian Cruise Line Holdings' forecasts yield a $28.20 fair value, a 54% upside to its current price.

Exploring Other Perspectives

Six individual fair value estimates from the Simply Wall St Community cluster between US$28.20 and US$45.10 per share, well above the current market price. While these viewpoints suggest confidence in the company’s future, remember that persistent high leverage remains an ongoing consideration for Norwegian’s earnings and flexibility, explore these diverse outlooks to gain a fuller picture.

Explore 6 other fair value estimates on Norwegian Cruise Line Holdings - why the stock might be worth over 2x more than the current price!

Build Your Own Norwegian Cruise Line Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Norwegian Cruise Line Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Norwegian Cruise Line Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Norwegian Cruise Line Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Norwegian Cruise Line Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NCLH

Norwegian Cruise Line Holdings

Operates as a cruise company in North America, Europe, the Asia-Pacific, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative