Advertisement

- United States

- /

- Hospitality

- /

- NYSE:MCD

McDonald's (MCD): Assessing Valuation as New Menu Collaborations Spark Holiday Buzz

Simply Wall St

Reviewed by Simply Wall St

McDonald's (MCD) is rolling out a slew of limited-time offerings, including The Grinch Meal and a Disneyland Resort anniversary collaboration, just ahead of the holiday rush. These promotions aim to drive fresh consumer interest and boost foot traffic.

See our latest analysis for McDonald's.

Against the backdrop of fresh offerings and energetic holiday marketing, McDonald's share price has shown steady progress, up 3.1% over the past month and delivering a total shareholder return of 7.8% for the year. Although the company has seen a few operational bumps and ongoing local activism, momentum has generally held as McDonald’s relies on brand power, expansion, and promotions to bolster investor sentiment in an evolving consumer landscape.

If a global icon’s strategic moves inspire you to think beyond the golden arches, now is a great time to broaden your perspective and discover fast growing stocks with high insider ownership

With new collaborations, steady returns, and ongoing brand expansion, investors may wonder whether McDonald’s stock still has room to run or if all this optimism is already reflected in the current price. Is this a buying opportunity, or are future gains already priced in?

Most Popular Narrative: 5.9% Undervalued

The most closely followed narrative puts McDonald's fair value at $331.53, a modest premium to the last close price of $311.82. The current share price sits just below the narrative’s outlook, raising questions about whether market consensus is underestimating some of the company’s levers for future growth.

The accelerated rollout of technology initiatives (AI-powered order-taking, kitchen automation, edge computing, and IoT-enabled operations) is poised to materially improve operational efficiencies, reduce labor and equipment downtime costs, and ultimately enhance operating margins and EPS as tech investments mature after 2026.

Want to know the bold assumptions shaping this fair value? The narrative leans heavily on game-changing tech investments and margin expansion that could reset McDonald’s earnings profile. Wonder which key financial drivers set this price apart? Dig into the full story to see what’s making analysts optimistic about the next chapter.

Result: Fair Value of $331.53 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent declines in low-income traffic or sustained cost inflation could hinder McDonald's ability to deliver on these optimistic growth projections.

Find out about the key risks to this McDonald's narrative.

Another View

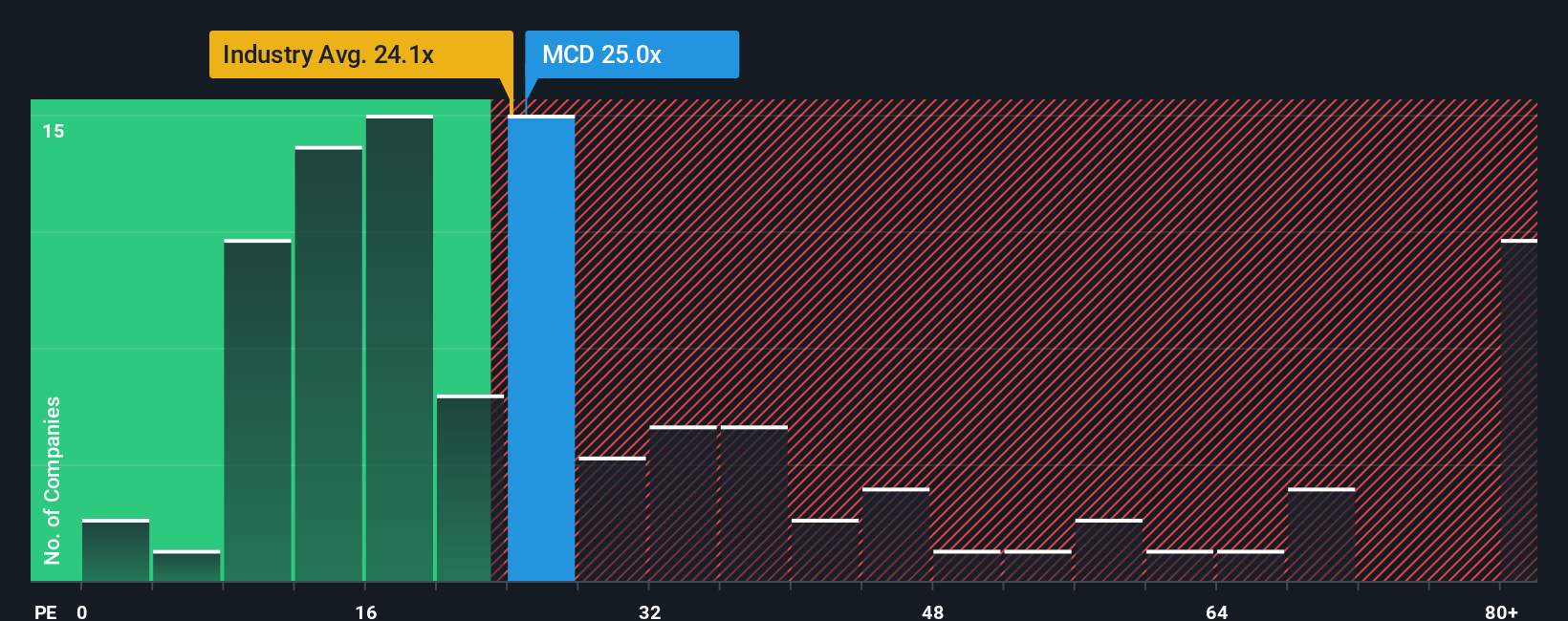

Looking from another angle, McDonald's is trading at a price-to-earnings ratio of 26.4x. That is above the industry average of 21.4x, but below what our fair ratio suggests the market could support at 29.5x. While peers average a much steeper 52.9x, this middle ground highlights both potential and risk. Will investors bet on further upside, or does the current premium signal caution?

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out McDonald's for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own McDonald's Narrative

If you see the numbers differently or want to explore your own insights, you can piece together a personalized McDonald's story in just a few minutes. Do it your way

A great starting point for your McDonald's research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for just one opportunity. Broaden your strategy and uncover untapped potential by checking out our pre-screened selections below. You might just find your next winning move.

- Capture high yields and stable growth by reviewing these 15 dividend stocks with yields > 3% with payouts above 3% and proven financial resilience.

- Get ahead of transformative trends with these 25 AI penny stocks featuring companies at the forefront of artificial intelligence innovation.

- Unlock overlooked value. See these 920 undervalued stocks based on cash flows based on robust cash flow, ready for a potential market re-rating.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MCD

McDonald's

Owns, operates, and franchises restaurants under the McDonald’s brand in the United States and internationally.

Established dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative