Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:WYNN

Wynn Resorts (WYNN): Assessing Valuation After Analyst Upgrades and UAE Expansion Progress

Simply Wall St

Reviewed by Simply Wall St

Wynn Resorts (WYNN) is making headlines after a wave of analyst upgrades highlighted growing optimism around its expansion into the UAE. The company’s investor event and progress update on Wynn Al Marjan Island are drawing particular attention.

See our latest analysis for Wynn Resorts.

Momentum around Wynn Resorts is picking up, with upbeat investor sentiment following construction milestones, luxury renovations in Las Vegas, and a recent analyst upgrade after more details surfaced on the high-stakes UAE project. The company’s 53.6% year-to-date share price return and robust 1-year total shareholder return of 37.7% reflect both short-term excitement and longer-term confidence in Wynn’s growth pipeline.

If big moves in the resort sector have you looking for new opportunities, now is a perfect time to discover fast growing stocks with high insider ownership

With shares sitting just below recent analyst price targets and anticipation building around the UAE project, the key question is whether Wynn Resorts is still trading at a discount or if the market has already factored in its next growth phase.

Most Popular Narrative: 6.7% Undervalued

Wynn Resorts closed at $128.68, putting it below the widely followed narrative’s fair value estimate of $137.91. This sets the stage for an ongoing debate: is the market underpricing Wynn’s ambitious future?

The imminent launch of Wynn Al Marjan Island, with first-mover advantage and limited near-term competition in a potentially multi-billion-dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step change in both consolidated revenue and EBITDAR.

Want to unlock the math behind this bold target? Here’s a hint: the valuation rests on transformative earnings growth and improving profit margins, built on Wynn’s international leverage. Intrigued by the narrative’s key forecasts that back this premium? Dive deeper to see what’s fueling the optimism and whether the assumptions will truly hold up.

Result: Fair Value of $137.91 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent reliance on Macau and rising costs could still shake Wynn’s growth story if regulatory or economic headwinds intensify unexpectedly.

Find out about the key risks to this Wynn Resorts narrative.

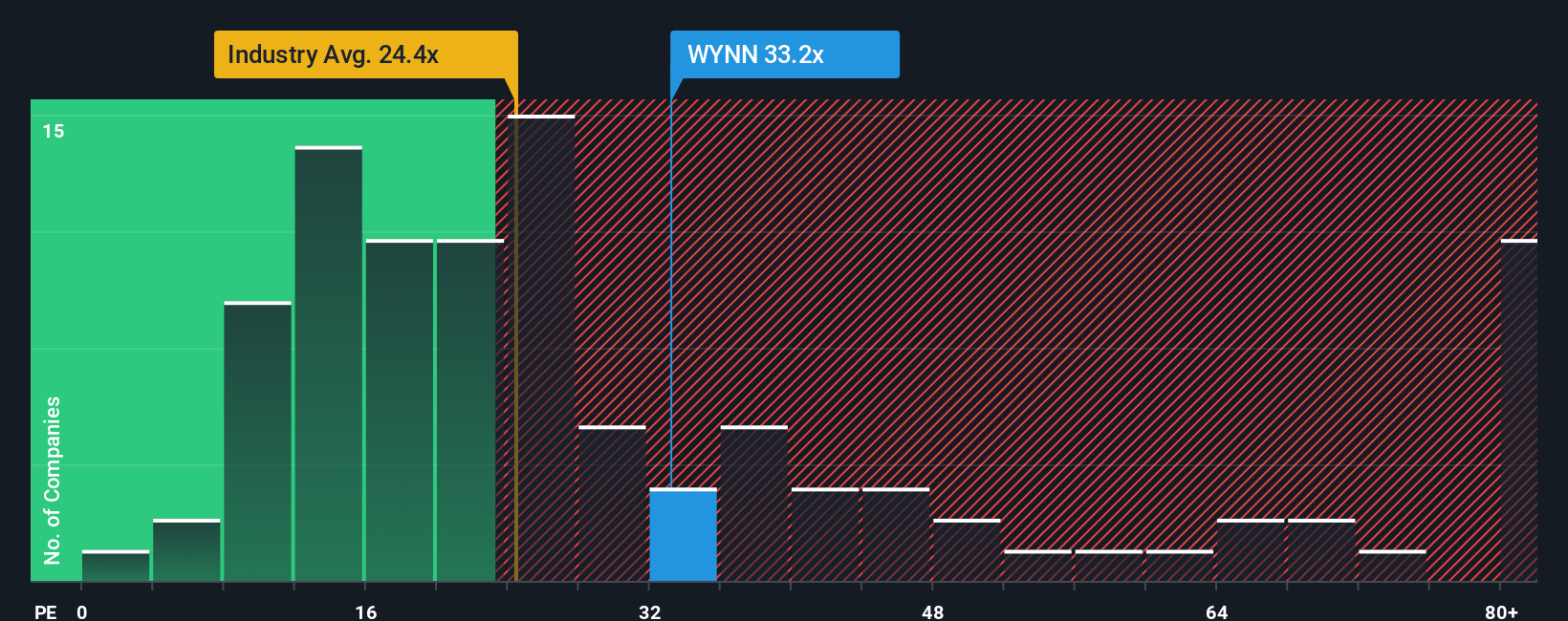

Another Angle: PE Ratio Sends Mixed Signals

Looking at Wynn Resorts through the lens of the price-to-earnings ratio, the picture is a bit different. The stock trades at 26.3 times earnings, which is attractive compared to the average peer at 61x. However, it is higher than the US Hospitality sector average of 21.4x and above its fair ratio of 23.7x. This gap highlights some valuation risk if the market shifts toward more conservative multiples. So, is the PE premium justified, or is caution warranted?

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Wynn Resorts for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Wynn Resorts Narrative

If you want to challenge the consensus view or dig into the numbers on your own terms, you can produce a fresh take in just a few minutes. Do it your way

A great starting point for your Wynn Resorts research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let your next winning idea slip past you. Use the Simply Wall Street Screener to unlock new opportunities tailored to what smart investors are watching right now.

- Boost your search for high potential growth by checking out these 25 AI penny stocks making waves in artificial intelligence and automation.

- Tap into the world of digital innovation and seize timely opportunities among these 81 cryptocurrency and blockchain stocks revolutionizing global finance.

- Secure stronger long-term income potential by browsing these 15 dividend stocks with yields > 3% that offer reliable yields amid volatility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wynn Resorts might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WYNN

Low risk with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative